Believe it When You See it

Oil market participants do not need any more uncertainty, therefore the glitch in CME today which has all futures markets down, might throw up some strange trading levels when it eventually arises from its binary-spilling slumber. As it is, the Ukraine negotiations can give one a healthy dose of optimism or in our case, scepticism. Vladimir Putin has said that the current framework of peace could be something to build upon in the future, which is hardly a signal of a softer immediate intent. In fact, he went on to say that any naysaying from Kyiv would result in Russia fighting on. The chief of staff to Volodymyr Zelensky is quoted across media as saying, “as long as Zelensky is president, no-one should count on us giving up territory. He will not sign away territory,” which might just be the trigger for Moscow to not lay down arms. It then appears that any singing around a campfire will be delayed and with sanction relief notions for Russia being eroded, oil prices gain a morning pop. In usual quiet circumstances, and with little else to consider (we look at OPEC below), aligned influences are easily attached, which is the case for the Fed decision in December. The USD is flagging as the CME FedWatch tool prices a quarter-point reduction at 85 percent probability, but the convenience of a softer US Dollar bringing oil demand will be quickly blown away if, or ever, a firm outcome is seen from the Ukraine talks.

Not much choice for OPEC

It should come as no surprise that the leaking of intention from OPEC shows the cartel likely to once again put a hold on increasing production. While it is imperative that the group of allied oil producers maintains a policy of wresting market share back from the ever-incursive exports coming out of the Americas, it must avoid being part of a catalyst that breaks the back of oil market price resolve.

Some of the problems faced by OPEC may be insurmountable in terms of discipline. Indeed, the reversal in attitude from production prohibition to a policy of ‘if you can’t beat them, join them’ by turning their combined spigots on, is very much authored by the serial cheaters of Iraq, Russia and Kazakhstan. This has been a hard lesson learned and made all the more difficult by the likes of Venezuela, Iran and Libya having exemptions from quotas.

The South American country earns over 90 percent of its export revenues from the oil industry matched by Libya, while it is 57 percent for Iran. Venezuela and Iran are subject to oil sanctions and Libya cannot shake the hangover of a divided country guilty of literally shooting itself in the foot by never achieving oil revenue potential. It does not take much imaginative thinking, allowing for time, that any solving of these problems will see a utilisation of their massive spare capacity without being limited to quota. This is without doubt a stretch, but quota within OPEC will be a source of conflict going forward probably forcing the de facto leader, Saudi Arabia, metaphorically taking on the form of Lord Vishnu and with many arms, club and cajole the Kingdom’s errant partners into accord.

It is not only the prospect of unleashed, including quota-exempt oil that haunt the cartel’s future oil supply revenue. Geopolitical and geoeconomic conditions are stubborn in signposting short-term negative issues for demand. Millenia of religious and land conflicts in the Middle East suggest that the recent flare up surrounding Gaza will never be far away in repetition, but the risk premium in oil prices felt as Israel exacted revenge across the countries harbouring indigenous and proxy enemies has all but evaporated. Likewise, if a miraculous coming together by Ukraine and Russia armed with war-ending words and not weapons is achieved, the almost guaranteed increase of Russian exports, no matter what quota, will have the ability to crush the Brent flat price into quite a low $50-something per barrel.

The genie is out of the bottle for OPEC. There is no going back to supply-side price control. The group’s members and affiliates cannot risk losing market share and indeed whatever influence it has left. There is merit in the argument on how OPEC is no longer a price-setting mutual, but a political bloc endeavouring to influence the globe’s energy attitude. Individuality is a byword for the modern era with all producer nations exampling this as they are driven by the same parochial pressures and self-serving arguments that each have unique problems. Membership then is political, strategic and convenient by weight of numbers.

Reuters sources have been reliable in this period of policy transition and claim ministers on Sunday are expected to discuss a mechanism to assess countries' maximum production capacity, to be used as reference for 2027 output baselines. Discussions on baselines enables future economic forecasting, but also means discussions on future quota, and which of any country would want a smaller one? Aiding the OPEC decision on Sunday is its inability to yet reach the group’s combined production quota total. It would be, and will in the future be, a very different meeting if limits were being pushed, but as it stands the most sensible thing for OPEC to do over this weekend is stay its hand and stay quiet, lest it becomes the lever which tips oil prices over the edge.

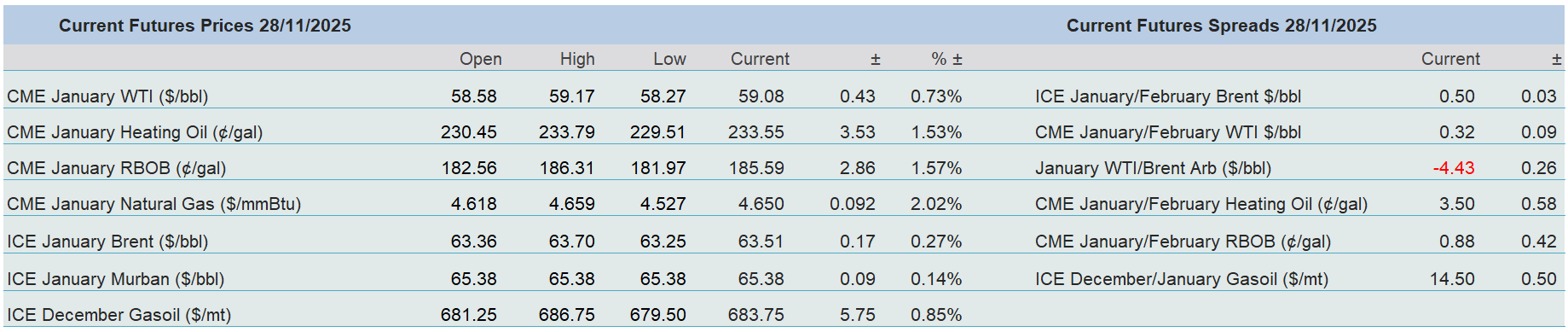

Overnight Pricing

28 Nov 2025