‘Best Offer’ Day is Here, Who Has the ‘Metal’ to Get Involved?

Markets once again experience a turn point day as the ‘best offer’ deadline for countries to propose their trade deals with US arrives. Five weeks ahead of the day when the reciprocal tariffs will be implemented, it appears Trump’s Administration is keen for countries to settle beforehand. Cynically speaking, it does beg as to whether the US is playing chicken, and one wonders if some hard-nosed dealing countries were to take it to the limit, there might not be just another extension available. However, what does serve the US well is the example of early settlement from the UK. With an agreement based around a 10% tariff and 25% on metals, the UK has been able to avoid the 50% extended tariff on Aluminium and Steel which also becomes live today. The day will likely be filled with a narrative from the White House on how countries are lining up to engage and opposing language from those which are about to find penalty.

Meanwhile, in a break from recent equity versus energy price movement, oil is still finding bullish interest as the wildfires in Canada are being measured as an antidote to the extra 411kbpd voted in by OPEC+ over the weekend. There continues a narrative of low inventory which has found an ally in the API Crude draw of 3.3mb against an expectation of a 1mb reduction. The build of 4.7mb in Gasoline will temper enthusiasm as it is the motor fuel which many expect to be the defining strength of the oil complex over the next few months, therefore, eyes will be on the EIA breakdown of inventory later and indeed the performance of refineries. Ceasefire talk in Ukraine is just that. A settlement seems so very far away, and with Iran making it known that a nuclear deal at present will be rejected, a change in the geopolitical scene that allows for more oil to be released from sanction is currently non-deliverable.

Manufacturing dozes in the shadow of stock market success

We cannot but doff our caps to the resilience of those that plant their money in the growth of US stock markets. Each bout of a tariff turnout, the accumulation of even more sovereign debt once the ‘big, beautiful bill’ is passed or even downgrading from the likes of Moody’s is greeted with opportunistic buying and presents a healthy state of investor mind. However, there really is divergence in the state of investment and the state of the world’s manufacturing sector. From the start of business in Asia to the close in the US on Monday the data presented tells of industrials that are not just idling but likely misfiring in the face of an uncertain future.

In Jibun Bank’s report, it spoke of manufacturing conditions in Japan improving slightly with business conditions deteriorating at a softer pace and the downturn in new orders eased notably on the month. But demand remained soft and while contraction was ultimately modest factory output once again fell. Across the Sea of Japan, and on the face of South Korea’s Manufacturing PMI reading, a slight betterment is witnessed between the reading of 47.5 in April to the 47.7 of last month. Yet, it is so very shy of expansion and continues to lay bare the problems of a country so imbued with a go-to culture. Within the S&P Global release not only is contraction a thing of four-straight months, but output has also fallen at its steepest for well over two years and new orders have been trimmed at a pace not seen since mid-2020.

Travelling nearly 9k kilometres west and several time zones the PMI eye scrutiny lands into the Old Continent and as is the case since Covid and the Ukraine invasion, manufacturing data has always been a source of trepidation if one were looking for signs of growth. HCOB Manufacturing PMI relies on a survey that encompasses 3,000 respondents in the private sector from, in order of economic size, Germany, France, Italy, Spain, the Netherlands, Austria, Ireland and Greece. Of all the centres of commerce, it is Europe that seems to be in throes of industrial renaissance. However, this rally of fortunes has started from a low base. The May Manufacturing PMI of 49.9 is a 33-month high as demand is seen as stabilizing, employment cuts diminished, and confidence rose to the highest seen since February 2022. The fortunes of Europe have been inextricably linked to energy costs and with a slump in fuel prices inflation has been encouraged lower prompting consumption, investment and rise in tourism. As good as this all sounds, it is not expansion, it is still contraction but in a milder form.

Importantly, and more relevant to the divergence between confidence in stock markets and confidence in industry came from the US itself and the Institute for Supply Management (ISM) Manufacturing PMI. At 48.5 in May, it fell well short of the 49.5 poll expectations and is two pips below that of April’s. The survey dwells on how new and old orders are falling as jobs, production, inventories, imports and exports are seeing contraction. Returning to Asia and marrying China to the plight of the United States, data stands in witness to how the other half of the real tariff war is faring in its own industrial path. Over the weekend the National Bureau of Statistics (NBS) Manufacturing PMI posted 49.5 and yesterday the private Caixin PMI 48.3. While the NBS reading hit the mark, the Caixin number is incredibly discouraging as activity in May shrank at the fastest pace since September 2022 and contracted for the first time since September last year. Foreign demand accelerated in decline as new export orders dropped to July 2023 levels.

The US and China are paired here for a reason. Their trading relationship will have the greatest influence of all. For there is not one part in the many and varied make up of manufacturing PMIs from Seoul to Berlin, from Madrid to Washington that did not find a mention in reports of how activity was being muted by the existence or at least the threat of tariffs and a global trade war. Even in the small improvements of Europe it still shares in the wider talk of provision for extensions both in time and measure on what punitive trade charges will be levied. The damage being done by Donald Trump’s pursuit of lopsided and wishful trade agreements has palpable negative data within manufacturing circles, and while stock markets can skip along while whistling to the tunes from A.I., there remain serious barriers to industrials and by association growth in oil demand.

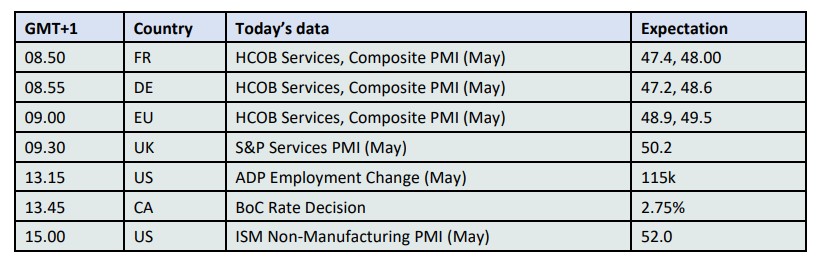

Overnight Pricing

04 Jun 2025