Breathing Space

• The US agreed to halt attacks on Iran for two weeks if Iran reopens the Strait of Hormuz.

• Building on this, Iran’s foreign ministry says the country’s military would allow safe passage through the Strait if the US halts its military operations.

• Meanwhile, Israel supports the suspension of attacks, provided it does not include Lebanon.

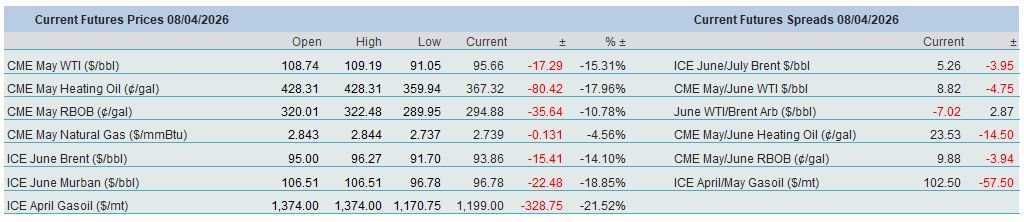

• WTI has fallen to $91.05 and Brent to $91.70/bbl following the announcement of the two-week truce. The Japanese stock market is up 5.2%, and the South Korean stock index 7.1% at the time of writing.

As a two-week ceasefire has been agreed, the market reaction has been textbook: equities are experiencing a relief rally, while oil, on the promise of traffic resuming through the Strait, is in freefall. In theory, the 10–13 mbpd of crude oil and product supply stranded behind the Strait should now be gradually released. Whether the pre-March status quo will be re-established depends entirely on whether the truce can be turned into a permanent peace during the negotiations in Pakistan.

Under discussion will be a 10-point Iranian proposal, which includes its control over the Strait of Hormuz, as well as the lifting of US sanctions on the country. President Trump, instead of wiping out the country’s entire civilisation, now envisages a “Golden Age of the Middle East,” where there will be “big money to be made.”

At this stage, there is no talk of Iran giving up its nuclear programme or removing its autocratic regime. It remains to be seen whether reopening the Strait of Hormuz, which was fully functional before March, will ultimately prove to be the primary objective.

Awfully Tight Q2 Followed by Painfully Slow Loosening

The chief determinant of every forecast of economic growth, inflation, recession, stagflation, and, of course, the oil balance is the constant reassessment of the Iranian war. Since its duration and outcome have been and possibly still are far from clear, the figures are understandably readjusted on a weekly or monthly basis. The latest example of this need to recalibrate is the Short-Term Energy Outlook by the EIA, released on the Tuesday following the first Thursday of each month. Those, including the EIA, who predict significant changes from previous reports do not possess a crystal ball; rather, they follow an indubitable logic: the longer the conflict lasts, the greater the damage to both oil supply and oil demand.

Following this reasoning, it comes as no surprise that both the major and minor elements of the latest findings differ considerably from the March, let alone the February, reports. To begin with, prices have been consistently revised upward. Pre-conflict (in mid-February), the EIA estimated Brent to average $58/bbl this year and $53/bbl in 2027. A month later, and two weeks after the US and Israel began their military actions against Iran, together with the retaliatory measures, it became increasingly evident that the abrupt disruption to oil supply through the Strait of Hormuz would have a tangible impact on the supply-demand balance. As a result, Brent prices were revised up by $21/bbl for this year and by $11/bbl for next year. The following month, characterised by a disturbing escalation in both rhetoric and action, resulted in a price estimate of $96/bbl for this year and $76/bbl for 2027 for the European crude oil benchmark. More importantly, and with the upcoming US midterm elections in November in mind, the EIA expects US retail gasoline prices to peak at $4.30/gallon in April. The annual average is seen at $3.70/gallon, compared with $2.91/gallon two months ago.

Of course, these forecasts are subject to significant revisions, either upward or downward, depending on the direction the war takes. What appears evident, at least for now, is that the current quarter, the April–June period, will be the tightest, as the scarcity of available oil, both crude and refined products, precipitates a scramble for whatever volumes are available. Demand destruction, triggered by elevated oil prices, is then expected to emerge toward the end of the year.

Global oil demand for the second quarter of 2026 has been reduced from 104.74 mbpd in February to 104.27 mbpd this month. At the same time, the world’s combined petroleum and other liquids production has declined from 107.76 mbpd two months ago to 99.18 mbpd in April. OPEC+ output has been revised down from 44.90 mbpd to 37.65 mbpd over this period, while OPEC output has been downgraded from 34.26 mbpd to 27.01 mbpd. In other words, the impact of the paralysed Strait of Hormuz is clear for all to see.

As the situation remains fluid, changes in global oil supply and demand further down the line are less relevant than the second-quarter oil balance. What is particularly intriguing is that, due to significant reductions in production estimates, the EIA now forecasts a supply deficit of 5.09 mbpd for the second quarter of 2026. This contrasts with a projected surplus of 3.03 mbpd in February, representing a swing of 8.12 mbpd. This predicted drawdown of 5.09 mbpd during the second quarter (468 million barrels in total) still exceeds the estimated stock build of 1.73 mbpd in the second half of 2026 (equivalent to 318 million barrels). Even if the Strait reopens imminently, as last night’s developments suggest, and oil flows recover as quickly as possible (unlikely), it will take several months for the current tightness to reverse. However, each passing day without a realistic prospect of permanently ending the hostilities will simply prolong the period of supply shock. Furthermore, the geopolitical risk premium is likely to remain significantly higher than before the conflict; consequently, a return to sub-$70 levels is highly improbable, at least over the next year or two.

Overnight Pricing

08 Apr 2026