Bullish Tinged Uncertainty to Continue

After a tumultuous week in which oil prices, and indeed the wider investment suite, suffered almost minute-by-minute fluctuations as everything became exaggerated, the oil complex eventually pushed on in advances with the main contracts finishing week-on-week as follows; WTI +$4.90/barrel, Brent +$6.31/barrel, Heating Oil +31.09c/gal, RBOB +7.31c/gal and Gasoil +$59.25/mt. For much of the week, there seemed to be a quiet resignation that oil prices would drift after the Middle East inspired spike and march to the tune of the wider macroeconomic influence. As of October 10, money managers reduced net-long positions by 65,161 in Brent to the lowest bullish positioning for 20 weeks at 153,174 lots and long-only positions by 52,563 the lowest for 21 weeks at 208,515.

At times it felt as if the markets were in a Rocky movie as they were constantly floored only to bring themselves back before the count of 10 had finished. None more perplexing was the travail of the yield curves which had investors running for the hills of safe haven, only to return the next day. The US Dollar Index (DXY) ticked to 106.50, lost a whole point to 105.50 and roared back, setting already ground down teeth further on edge. The talking heads of the Federal Reserve assured the world that the high yield structure was doing much of the work in terms of financial tightening, but that stream of consciousness was quickly thwarted as the US posted slightly higher inflation data. Meanwhile, continuing worrisome trading numbers emerged from China as both exports and imports reduced by 6.2%, CPI registered a flat reading, a –2.5% reading in producer price index (PPI) and the warnings of deflation were fuelled yet again.

Oil prices suffered accordingly with Brent on Thursday evening closing only $1.50/barrel above where it languished the previous Friday before the horrific scenes seen in Israel and the ensuing risk rally. However, contemplating risk exposure to further incidents in Israel/Gaza and beyond and with a market unguarded by closed exchanges, a conservative walk to close shorts or indeed hold some hedging length turned into a full blown stampede and other bullish news factors that had been thus far ignored were partnered with this newfound bullish sentiment. The sudden decision on tightening up of sanctions on ship owners carrying Russian crude over the $60/barrel limit by the US started to niggle and so did the Russian/Saudi meeting concluded by President Putin stating that OPEC+ were achieving ‘stability’. Participants, looking for a reprieve in Saudi and Russian voluntary cuts, decided that Putin’s aside meant no such consideration would be forthcoming and all this ended in pent-up bullish leapfrogging.

This morning we enter the week a little subdued. Fortunately for the world the massed troops of Israel have yet to enter Gaza and the imagined flow-charts of expanding conflict are still just that. The US is going all out to contain the situation by both showing support for Israel by dispatching another carrier group to the area and by sending Secretary of State Blinken in a bid to keep all diplomatic solutions open. There are also murmurs on wires that President Joe Biden might even put in an appearance backing up his weekend calls for Israel to show restraint. The situation remains fluid and ugly for price prediction with little chance of a return to a relative normal market, whatever that might be post-COVID/Ukraine.

Venezuela Is Not the Answer

Since 2006, and according to the Congressional Research Service, the US Secretary of State in annual reviews has found that Venezuela has not adhered to, or cooperated with anti-terrorism efforts and this remains the case after the latest review in May 2023. Furthermore, Venezuela, has since 2005 failed to comply with obligations to international drug laws and this charge remains current, and in 2014 the South American country became subject to further accusations of anti-democratic actions, human rights violations and corruption by the United States.

All of these have brought both corporate, political and targeted individual sanctions which have been implemented and held up by the three administrations of Presidents Obama, Trump and Biden. How the US pressured President Nicolas Maduro in 2019 by sanctioning the state-owned oil company Petroleos de Venezuela, S.A. (PDVSA), is a matter of common discourse and so is the granting of a licence in November 2022 allowing Chevron to resume some oil production and trading where it had existing partnerships with PDVSA. Allowing such a license served two purposes in that Chevron were able recoup some of the debt owed to them, but also as a sweetener in bringing President Maduro to consider attending a conference where ‘free and fair’ elections were to be discussed with an international panel. The very intricate nature of the sanctions, so intertwined with the oil industry, and the hate/hate relationship between the two governments brings into question how the US, seeking to find extra oil for the world, will be able to justify sanction lifting in such a toxic relationship.

Indeed, further scrutiny reveals that in 2008, one of the reasons terrorism-related sanctions were expanded was due to US treasury evidence that Venezuelan companies and some individuals were giving aid to Hezbollah. Whether or not such financial contributions to an internationally labelled terrorist organisation (or at least its military wing) continue to this day is a matter for the imaginary dark world and the backrooms where all the secrets lie, but if the financial link is still legitimate the road to free flowing PDVSA oil is a bumpy one. Hezbollah, in its 1985 manifesto, called for the destruction of Israel, it has tight links to Hamas and is funded, as is Hamas, by Iran.

How the United States unravels this pickle of political patronage is a task worthy of a chess grandmaster. How it also squares away doing business with a possible terrorist funder with an electorate that is 65% in favour of support for Israel, according to a recent NPR-PBS poll, in bare-faced oil price expediency will also be intriguing. Negotiations are currently being brokered in Doha, Qatar between Venezuela and the United States but it does seem to be a drawn-out process. Even if all hurdles were miraculously cast aside, Venezuela crude exports in August were under 600,000 barrels per day, which is why the oil market considers the risk of an expanding Middle East conflagration involving possibly Iranian and Saudi oil infrastructure as a much more pertinent and powerful influence.

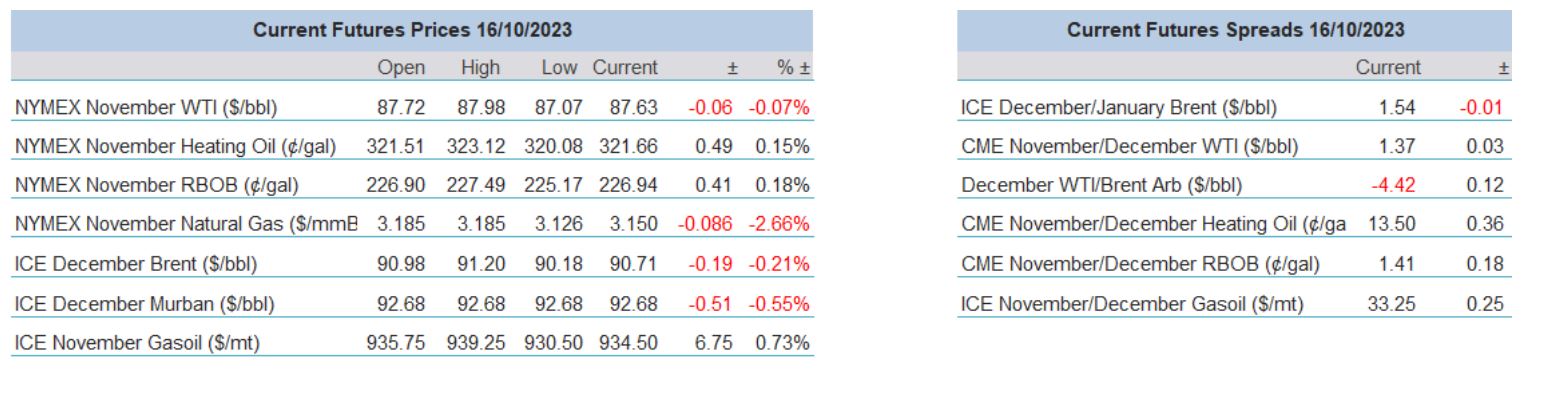

Overnight Pricing

16 Oct 2023