Buy the Rumour, Sell the Fact

The risk to oil prices coming from geopolitical instability is very much on full display again this morning as the developments in Iran, so very much part of the driving force behind the recent rally, have taken a much less anxious turn overnight. After promising “help is on its way”, giving an expectation of a US military intervention, the US President has turned the oil market’s mood by saying he has received assurances that killings of demonstrators in Iran had stopped. The softening of attitude by Donald Trump has seen a collaborative statement from Iranian Foreign Minister Abbas Araghchi. When asked in an interview with Fox News on plans to execute protestors, the Minister responded that Iran would do no such thing and that “hanging is out of the question.”

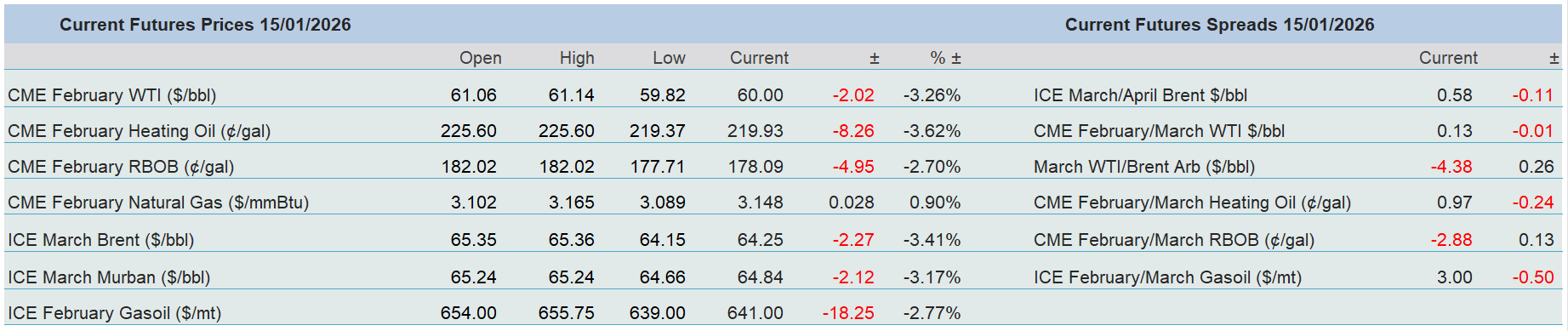

The ladder of risk premium has just lost, well at least temporarily, one of its rungs. Yesterday morning, the roundly bearish builds seen in the API private inventory report were ignored, and up and until the close so were the 3.4mb and 9mb stock increases respectively seen for Crude and Gasoline in the EIA Weekly Inventory Report. Oil prices are then this morning resetting to reflect the continued and sobering narrative of a market looking at a near-term future of oversupply. Even OPEC’s Monthly Oil Market Report seemed to be a study in conservative growth predictions. Having begun 2025 by expecting demand growth of 1.85mbpd, it has trimmed its final forecast for the year to 1.3mbpd and matches it with expectations for 2026 and 2027 at or around the same number. Our market is set to scamper forth on global flash points and probable winter disruptions, only to be keenly corrected by the forever stories of being more than adequately supplied, well at least by the basis feedstock. Short-termism in position taking will define our market’s movements for at least the first quarter.

China's surplus is a target on its back

It does not take too much of an imaginative leap to believe that there is trouble brewing once again between the US and China. Even if Mr Trump has not publicly recognised it yet, the latest trade data from the General Administration of Customs shows China sporting yet another record trade surplus which will likely have the currently agitated American president spitting feathers. For all the posturing in tariffs, deal-making surrounding rare earth materials and microchips by the US, the Chinese titular mastery of trade balances continues unfettered. Despite the unwillingness from the US to give China a trade advantage, it does not seem as if it has taken much of an effort to diversify to willing customers elsewhere.

The pattern of Beijing’s trade punch has hardly changed. It has not allowed the Renminbi or the Yuan to float but ‘manages’ them in a rate exchange; currency manipulation by any critic’s standard. With a daily midpoint ‘fix’ and next-day trading not allowed to move more than 2 percent from it, supressing its money and keeping currency pairs in a permanent state of tolerance not only allows advantage from an exporting point of view, but also the ability to take longer-term decisions without foreign exchange being a major consideration in export risk. The status quo is seen in how the state is fully invested in the globally competitive industries of cars, alternative energies and all things technology. Since breaking the shackles of old-style communism and an agricultural existence, China has always been of the attitude that if something is worth building, it is worth building big. Therefore, it does not matter if it is a metal smelter, oil refinery or car plant, all have huge capacity, which if not used domestically must be utilised internationally and at such volumes as to undercut most competition.

The Belt and Road Initiative (BRI) launched in 2013 by President Xi Jinping in which China sought to increase is trading footing in all continents has enabled and exposed China’s companies to new markets and opportunities. With large investments in transportation, energy and computing in many countries it not only has skin in the game for various nations’ economies but more importantly, leverage. Switching its trade focus from antagonists such as Europe and the US to the more friendly and dare one say softened up markets of Latin America, Africa and South East Asia is noted by Reuters quoting Wang Jun, a vice minister at China's customs administration who reveals, "with more diversified trading partners, China's ability to withstand risks has been significantly enhanced." Indeed, printed yesterday, the trade surplus for 2025 stands at a record $1.2 trillion and while exports to the US dropped by 20 percent, they increased to Southeast Asia by 13 percent, Latin America by 7.4 percent, Africa by 26 percent and even by 8.4 percent to an oppositional European Union.

With such custom and growth in exports, there is little wonder on Beijing’s unchanged attitude of building its economy based on exports rather than domestic demand. It affords a less forensic and hurried need to address the slumping housing market and the stubbornness shown by citizens to save rather than spend. China’s trade data comes at an apposite time in the US tariff wranglings. Yesterday, the US Supreme Court was expected to give a ruling on the legality of Donald Trump’s tariffs but has delayed its decision by one week.

Whatever decision comes from the highest judges in the land on whether President Donald Trump exceeded his authority in using the International Emergency Economic Powers Act of 1977 when introducing the sweeping and swingeing tariffs that have dogged international trade, China’s trading success will be as a red rag to the currently rampaging White House bull and no matter the stranglehold China seems to have on the US because of rare earths, we should prepare ourselves for another bout of US/Sino tension in tariffs, sanction and TACO versus a lighter form of CACO (China always chickens out) or deflection.

Beijing yesterday was quick to lay the blame of its burgeoning trade superiority squarely at the foot of Washington’s tariff and trade restriction policies. Returning to comments from Wang Jun, and as seen in the FT, export controls on high-tech products were preventing China from importing more and if there existed a freer world trade environment China has vast room for import growth. It is difficult to see how this will not descend into another repeated face-off between the world’s two greatest trading nations particularly as the current confrontational mood of the US President suggests he is hardly likely to let this one pass him by.

Overnight Pricing

15 Jan 2026