The Camera is Rolling

The pre-election political environment in the US has all the ingredients of a Hollywood blockbuster. The tension is palpable, relationships are toxic, and it features the Good and the Bad, and perhaps even the Ugly. It is full of intricacy, not to mention the numerous assassination attempts and part of the storyline is centred around money. The casting has started, and it seems obvious that if the few weeks running up to the 2024 US elections is, in fact, turned into a movie Donald Trump will be played, well, by Donald Trump.

Other salient characters, who might eventually play a significant role in deciding how the finale of the election charade pans out are the Fed’s chair and his acolytes. An interest rate cut of 0.5% tomorrow, the chances of which are currently 67%, according to the CME FedWatch tool, could provide a much-needed economic boost that may tilt the pendulum amongst undecided voters in swing states towards the Democratic nominee. Cheaper money will also permeate the oil market and continuous dollar weakness will underpin the current optimism. Tomorrow’s event could weigh heavily on whether Donald Trump will be elevated to a ‘Chuck Norris’ type of fame and will be viewed as invincible or degraded to the status of the ultimate villain both amongst Republicans and Democrats.

For the coming day or two the Fed move will be the dominant driving force, that much was clear yesterday. Oil rallied hard and the dollar remained under attack notwithstanding rising Libyan crude oil exports after nearly two weeks of disruptions and the gradual normalization of production in the USGC in the wake of Francine. Oil fundamentals will indisputably take over the role of price-setting, for the immediate future, however, the cost of money in the world’s biggest economy will remain in focus as the investment fraternity, US political parties and the electorate hold their breath.

Macro View against Structure

The latest leg lower came to an abrupt halt last week but whether this change in the trend and sentiment is temporary or it signals a medium-term bottom is not entirely clear. We outlined in yesterday’s note that there are as many bullish as bearish factors to consider and a few days earlier we implicitly implied that the trend reversal cannot be far away.

Until the middle of last week, the oil market appeared truly awful as epitomized in the latest Commitment of Traders report from ICE, which shows money managers deserting Brent. For the first time since data was published 13 years ago, they have built up net short positions. The factors behind this fallout are well publicized and known. China is unable to get its economy going, partly because its communist leadership prioritizes national security and ideological considerations over the wealth and well-being of its citizens. In the US, for some obscure reasons, the talk of recession has been getting louder of late. Both OPEC and the IEA have cooled on demand prospects, non-DoC oil supply is anticipated to remain robust and not even God knows how long a handful of OPEC+ producers will be willing to constrain their individual production levels for the sake of the greater good of the alliance.

Probably there were several components in the mix, which helped brighten investors’ mood, at least for now. Inflation is being controlled in major economies, after the ECB rate cut last week, the Fed is expected to follow suit and might even go for 0.5%, the dollar remains under pressure, and Near Eastern and Ukrainian turbulences must play their roles, too. The decision of major OPEC+ producers to delay the planned unwinding of their voluntary cuts is also seen as a supportive factor.

When one calls for the bottom, she must assume that OPEC+ will not return barrels to the market. It would change the mood, the narrative and the oil balance. Whether such a move is feasible will be the topic of Thursday’s report. Until then, it must be observed that the most striking element of the recent price drop was the relative stubbornness of inter-month spreads to follow the move of outright prices south. This resilience flies in the face of the continuous weakening of crack spreads, yet inter-month spreads showed a recalcitrant attitude towards outright prices. Comparing and quantifying the relationship between flat price movements and spreads is anything but a practical science. As a rule of thumb, one might conclude that their directions of travel are aligned.

It is undeniably the case in the latest downturn, too but what is discernible is that the speed of the fall has started to differ. The oil market peaked in April and during these five months, the correlation between outright prices and the arbitrarily chosen M1/M7 price differentials has been subdued. They were the highest in RBOB and Brent at 94% and 88% respectively, but not acknowledged by WTI at 75% with Gasoil and Heating Oil at 48% and 27%. During the latest leg down, which started on August 21, the Heating Oil structure has actually strengthened somewhat against the fall in the outright price.

The seasonality of the product contracts makes it challenging to draw a firm conclusion on future price direction, nonetheless, the extent of M1/M7 contango on Heat and Gasoil does not imply an awfully oversupplied market. Current US distillate stocks are 9 million bbls under the 5-year average although the surplus to the seasonal norm is around 300,000 tons or 12% in the ARA hub, a slightly concerning sign. US gasoline inventories are on par with the 5-year average as the front spread is firmly backwardated.

A stronger signal comes from the crude oil contracts. Depleted US crude oil and Cushing stocks, which is a firm indication of the growing role the US benchmark plays in international oil trade, help its backwardation persist. Brent also commands premiums over successive contracts down to September 2025 and its physical version is around 90 cents/bbl higher than its forward peer for next week. It seems that macroeconomic considerations are not entirely backed up by the fundamental snapshot as mirrored in time spreads. By no means are we insinuating an irreversible rally back to the year’s high, but unless inter-month spreads start weakening considerably, possibly triggered by a change of heart from the OPEC+ group or by a bearish interest rate rabbit out of the Fed’s hat, a protracted break under recent lows is implausible.

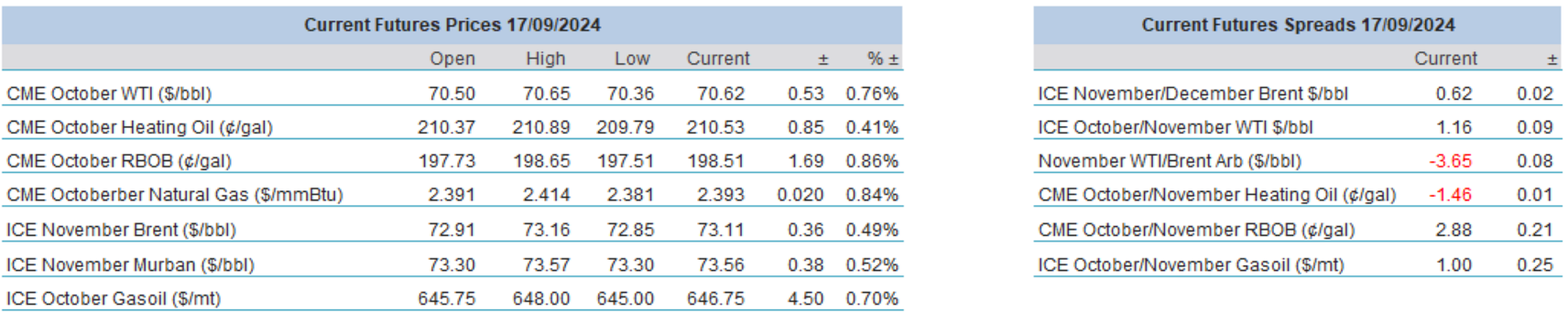

Overnight Pricing

17 Sep 2024