Cautionary Tale

It might be a forced parallel, but as the UK has gone through six Prime Ministers since leaving the European Union almost exactly ten years ago, the question arises: is reluctance or ego to cooperate, confrontational policies coupled with a bellicose narrative, and unsubstantiated optimism the most effective way to achieve one's goals, or does it more likely lead to unpredictability, mayhem, and havoc? Those who closely follow the ongoing nuclear talks between the US and Iran must surely ask themselves these questions.

Details are sketchy and often contradictory. Consider, for example, the role of the International Atomic Energy Agency in curbing Iran's nuclear ambitions. According to President Trump, Iran has agreed to nuclear inspections, a claim that was almost immediately rebuked by the other party. Go figure.

While the confusion—or perhaps the pursuit of negotiating leverage—may be idiosyncratic to the Middle East talks, oil appears to be transiting through the Strait in increasing volumes. This keeps oil bulls, if there are any left at present, in check. The build in US product inventories, as reported by the API last night, ensures no change in sentiment this morning. The dire state of the Russian energy sector, contemplating a ban on diesel exports while importing other fuels amid a barrage of Ukrainian drone strikes, is being overlooked.

Although a recovery in demand does not appear imminent (as evidenced by the disappearance of AI-driven support for equities yesterday), and supply is on the rise, the latter may not be able to grow quickly enough to turn the currently anticipated deficit into a surplus.

Slow Recovery of Oil Inventories, but Does Anyone Care?

The job of the analyst is to use available data, present it to their audience, and draw conclusions from it. Of course, in an interconnected, complex, and often chaotic environment, drawing firm conclusions is a cumbersome task, and one may find that interpretations of the data repeatedly prove inaccurate. When that happens, desperate attempts to rectify or amend prevailing assumptions begin.

The oil market is presently immersed in uncertainty, although the price action suggests otherwise. As noted in recent days, when it suffers a price decline of $50/bbl, or 40% (firmly within bear-market territory), in less than two months, it is difficult—and even foolish—to argue against who is in control. The extended ceasefire between the US and Iran, the lifting of the US naval blockade in the Strait of Hormuz, the removal of force majeure declarations in neighbouring Gulf states, and waivers allowing the Persian Gulf OPEC member to resume crude oil and product exports dominate market thinking and sentiment. In a nutshell, available oil supply is rising, and this is clearly reflected in price movements. Contradictory factors—such as protracted peace talks without firm commitments, occasional threats to reignite hostilities, or the damage the Russian oil sector is being forced to endure as a result of surgically precise Ukrainian drone attacks—have been relegated to the back of the market's collective memory and are unequivocally compartmentalised.

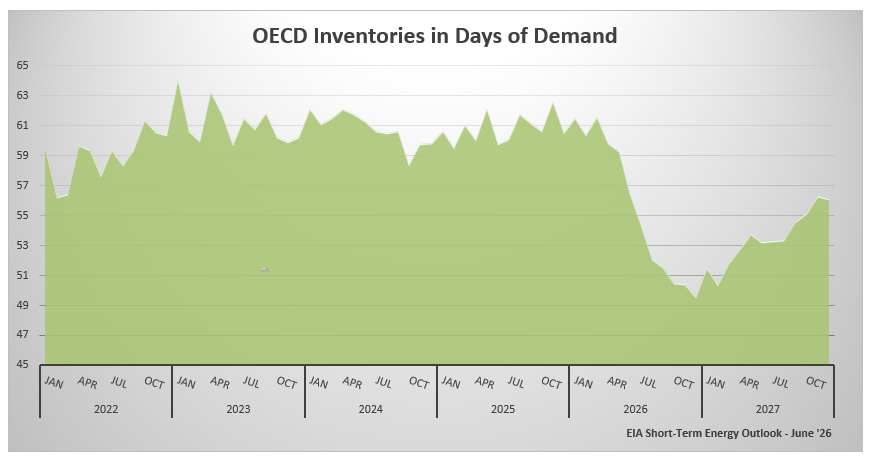

Admittedly, the current weakness can be characterised as surprising and unexpected. We recall the ubiquitous warnings from not so long ago, claiming that even if the conflict were to end tomorrow, oil inventories were so close to critical operational levels that prices would not fall in the immediate future. It is intriguing to observe that only the second half of this assertion has proved inaccurate. To corroborate this, it is useful to examine the latest Short-Term Energy Outlook published by the EIA two weeks ago and assess how OECD inventories—not in absolute terms, but in terms of the number of days they would cover demand—are projected to fluctuate in the coming months.

The stock depletion, it goes without saying, began in earnest after February. What is particularly intriguing is that it is not expected to bottom out until after December this year, when it dips below 50 days of forward cover, down from 61.5 days in March. Simply put, this figure is unprecedented. Let us not beat around the bush: it should be terribly supportive of prices. Another interesting aspect of the graph is that when the recovery gets underway in 2027, growth in OECD commercial stocks (expressed in days of forward cover) will not challenge pre-crisis levels, far from it. By the end of 2027, this figure is projected to reach only 56.1 days, compared with the 2022–2025 mean of 60.5 days, during which Brent averaged $82 per barrel. One caveat is that the updated figures were published before the extended ceasefire was announced; thus, a revision can reasonably be expected next month.

Is there a reliable conclusion to be drawn from all this? There are two contrasting possibilities. The first is that the current price weakness is merely a reaction to concurrent developments, with little regard for forecasts or projections, but it will self-correct. The second is that there is simply no fear of missing out on an impending price rally because seemingly bullish forecasts are misplaced and oil inventories will remain ample throughout the remainder of this year and next. Do we dare choose?

Overnight Pricing

24 Jun 2026