‘To Cease Upon the Midnight with No Pain’

Apart from the obligatory upbeat rhetoric from the US administration, the gunpowder barrel, the Strait of Hormuz, that is, remains exposed to explosion. Whether the spark will be ignited by Iran or the US is impossible to predict. In fact, the gap between narrative and reality is now probably wider than that between physical and futures oil prices. The Pentagon is at pains to emphasise that the month-long ceasefire has not been broken, while continuing to exchange (i.e. not cease) fire with its adversary. Iranian cruise missiles were reportedly launched at US warships and commercial vessels; the US attacked Iranian small boats; and the UAE also suffered from the latest round of drone and missile attacks from the other side of the Persian Gulf (denied by Iran).

Yet oil prices dropped like a stone and equities rallied, allegedly because one or two vessels sailed through the Strait with the help of the US military within the confines of ‘Project Freedom’. Not even the most optimistic observer would label this move as the full and unconditional reopening of this pivotal chokepoint, particularly given Iran’s warning to the US Navy to stay out of the Strait while simultaneously extending its area of control around the waterway. Duly obliging and after just one day, the President, in another capricious move, suspended the project, citing ‘Great Progress’ toward a deal. Brent has shed another two dollars or so overnight, but it is hurtfully evident: the escape from suffering referred to in the headline, as so eloquently put by John Keats, remains elusive and, in our simplistic view and rudimentary English, this conflict ain’t done yet.

Continuously Tighter

Although estimates vary, there is a broad and indisputable agreement that a worryingly vast quantity of oil has been stuck behind the Strait of Hormuz since the end of February. It is anywhere between 9 and 14 mbpd; it probably changes by the day, but is growing relentlessly and will continue to do so unless the blockades—plural, because there are two—are fully lifted. Even under this ideal scenario, the normalisation of oil production and traffic will take months.

Against the backdrop of close to 1 billion bbls of crude oil and refined products stranded, it is curious to observe why oil prices are not significantly higher. Or, to rephrase it, why did Brent average lower in April than in March? After all, traditional consumers of Middle Eastern oil have been forced to look elsewhere over the past two and a half months to secure whatever supply is available.

One possible answer is perceived or actual demand destruction; however, this argument stands on shaky ground. As noted in yesterday’s report, signs of a severe cutback in the consumption of the black stuff have not exactly surfaced yet. Strong equities also hint at economies that are ticking along nicely, and although growth estimates have been downgraded, they remain impressively positive. Given the strong relationship between economic growth and oil demand, while consumption might retreat, it is unlikely to contract; the extent of the supply disruption will therefore play a much more salient role in shaping the oil balance than demand.

The second, and more plausible, explanation is that there has been a reassessment of risk. In the immediate aftermath of the conflict, the move higher was exaggerated. It usually is, because of the financialisation of markets. Rightly or wrongly, the geopolitical risk premium has been slashed, and a massive valuation gap has opened up between futures and physical prices. If the conflict proves prolonged, the geopolitical risk premium, which reflects anticipation of future supply disruption, will turn into a physical premium that buyers are willing, or forced, to pay in order to secure supply. The extent of the physical premium largely depends on stock levels. The inverse correlation between OECD stocks and prices might give us an idea of how large the supply deficit might be and, consequently, how high prices might go.

The latest projection from Goldman Sachs is not reassuring. The investment bank sees global oil inventories at an eight-year low, warning that the speed of depletion is becoming an acute concern. Its estimates show that worldwide oil stocks stand at 101 days of demand, which could decline to 98 days by the end of the month. The CEO of a US oil major expects physical shortages to materialise soon, as supply in commercial markets is being absorbed. On a side note, the API saw a collective drawdown of 18.8 million bbls in US stocks last night.

Monthly supply-demand reports provide invaluable guidance in assessing what can be expected in the foreseeable future. Taking EIA projections as a reference point, the trend is painfully obvious. In February, second-quarter global stocks were expected to build by 3.03 mbpd, third quarter by 2.68 mbpd, and fourth quarter by 3.18 mbpd. Two months later, the current quarter is expected to see a global stock draw of 5.09 mbpd, the third quarter a modest build of 290,000 bpd, and year-end an increase of 3.16 mbpd. It is therefore no surprise that OECD oil inventories are now estimated to be more than 300 million bbls lower in each remaining quarter of the year than projected three months ago.

Using the aforementioned inverse relationship, an updated oil price forecast can be derived. In February, the second- to fourth-quarter Brent price forecast stood at around $50/bbl: $47.76 for Q2, exactly $50 for Q3, and $54.57 for Q4. The anticipated depletion of global and OECD inventories pushes these estimates up to $96.88 in Q2 (the quarter-to-date average is $103.70) and $128.30 in Q3, before falling back to $82.63 in Q4. Notably, all three agencies painted a rather optimistic picture for Q3—i.e. some degree of normalisation and a narrowing of the deficit, or even slight stock builds. Since the Strait has not reopened, downward OPEC supply revisions are likely this month, leading to lower stock levels and upward amendments in price forecasts.

No doubt, prices are driven not by formulas but by headlines and sentiment; however, the latest and upcoming reports on the global oil balance strongly suggest limited downside potential for prices.

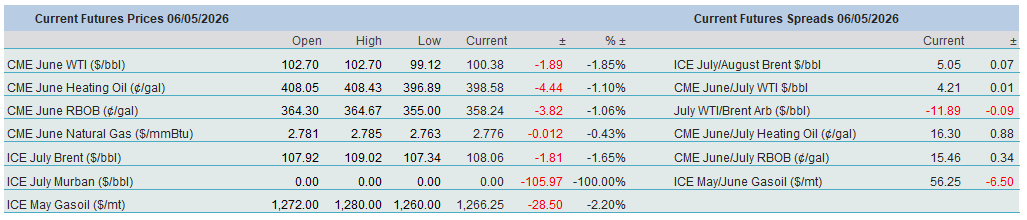

Overnight Pricing

06 May 2026