Ceasefire Increases Oil Movement Stasis

The war in the Middle East has taken another turn, and arguably for the worse. Instead of trading missiles, drones and bombs, the new metric is how many ships can each side interfere with. After the US imposed its own blockade, it has now taken it internationally by intercepting 3 oil tankers in Asian waters, far from the Persian Gulf. Returning the favour, Iran has captured 2 container ships and IRGC gunboats have fired upon other vessels in and around Hormuz according to the United Kingdom Maritime Trade Operations. This is a new phase in the war and as always, an unexpected turn of events. There may be a ceasefire in military terms, but the barriers to international oil communications have just received even more crippling additions and even if another piece of military hardware is never unleashed, while this freezing of Gulf states’ energy assets continues, the chances of Brent heading back toward $120/barrel increases every day.

War always has consequence

Just because there is not a mushroom-shaped cloud over the Iranian horizon, it does not mean there is not fallout. We noted yesterday on a warning from the World Bank and the International Monetary Fund that any shortages in oil supplies would be exacerbated by excessive stockpiling and hoarding. O, for such an opportunity. It will be interesting to see in the future whether India takes up the calling of having massive strategic petroleum reserves because it is bearing undue burden in this current crisis. At present, as seen in the ’Economic Times’ and ‘Indian Express’, the ISPRL is a special purpose vehicle floated as a wholly owned subsidiary of the Oil Industry Development Board for building and managing the strategic crude storage. Currently, it has three underground caverns at Visakhapatnam (1.33 million tonnes), Mangaluru (1.5 million tonnes), and Padur (2.5 million tonnes). At capacity, India’s SPR may only cover about 9 days of crude oil consumption although when added to refined fuels that number increase to 74 days held mainly by refiners. Currently, the estimate across Indian media is that there are only 5 days of supply held and even if private oil product reserves are steady, the total is woefully short of the IEA’s recommendation that countries hold 90 days of stock equivalent of their net imports, although at present India is exempt as it is only an associate member.

The shortfall in crude holdings is reasoned by the state of current inflows. Using Reuters data, India’s crude oil imports fell 13 percent when compared with those of February. It also showed that at 26.3 percent, the share of Middle Eastern oil is at the lowest level since records began. The global outlook for trade growth at the start of the year saw projections matching those of 2025 at 4.7 percent, but with the constant uncertainty and disruptions from the Middle East, the United Nations Trade and Development last month published a view on how this has very much been whittled down in growth of between 1.5 and 2.5 percent. India, already somewhat hamstrung by tariffs and sanctions from the US, saw March exports fall to $38.9 billion last month, from $42.1 billion a year earlier, some 7 percent according to data released recently by its commerce ministry. At the beginning of proceedings in January, the financial year 2026-2027 saw forecasts of GDP expanding to 7 percent, this has now been dramatically trimmed by at least 1 percent and possibly more if the current hiatus in Hormuz continues. The biggest country in the sub-continent receives 60 percent of LNG, 90 precent of LPG and 25 percent of fertilisers from the Persian Gulf area as well as significant repatriated wealth from the millions of Indian workers who reside in the various countries hit by war.

In a full cycle of negative oil influence, the Indian Rupee has been in all but freefall, although movement lower has been arrested as the USD weakens with the risk rotation being seen in the United States. Still, the USD/INR has tumbled a full ten points from 85.0 to 95.0 year-on-year with half of that coming since February of this year. Additionally, and although with half of losses recovered due to the global influence of other stock markets, the BSW SENSEX Index is down 5 percent over the last 3 months, being 12 percent down at the start of April. The Reserve Bank of India is at present likely powerless to change the fortunes of India’s economy because a reliance on imported crude and a falling domestic currency does not give a signal that the economy would not immediately over-inflate if a rate cut was introduced to inspire growth.

The cost of this war is not notional; it is not something for the future and requires no crystal ball. It is manifest and negatively thriving in the once hopeful economy of India. Even when judged by diminishing GDP, it is the world’s 5th largest and its vulnerabilities to energy imports are being played out in a livestream nightmare. No doubt alternative supplies will be captured, from the dark vessels of Russia to the too-light crudes of the United States, but the cost at present is detrimental to New Delhi’s emulation of Beijing’s policy of exporting its way into world recognition. China has energy security at present. This is achieved by very smart utilisation of its vast SPR capability and the ongoing transition in energy, particularly that of internal combustion engined cars to electric vehicles. These choices are not available to the largest population on the planet. Transition will be decades away and it first must create the wealth to even contemplate such a move. Therefore, there is little option other than to build new SPR. Reuters revealed this month that India plans to build two new SPRs; the first a 18.3 million barrels cavern at Padur in southern Karnataka state, and then a 29.3 million barrels SPR in eastern Odisha state with private partners allowed to trade all of the oil locally but the government having first right of claim. Sadly, the project will not be completed until the end of this decade meaning there is further pain and energy insecurity to be endured. Yet for oil watchers it is interesting to see such vast potential in oil consumption being readied for the future, and despite its current agonies, India looks set to take up China’s mantle of being the source of both oil demand growth and oil price protector by 2030.

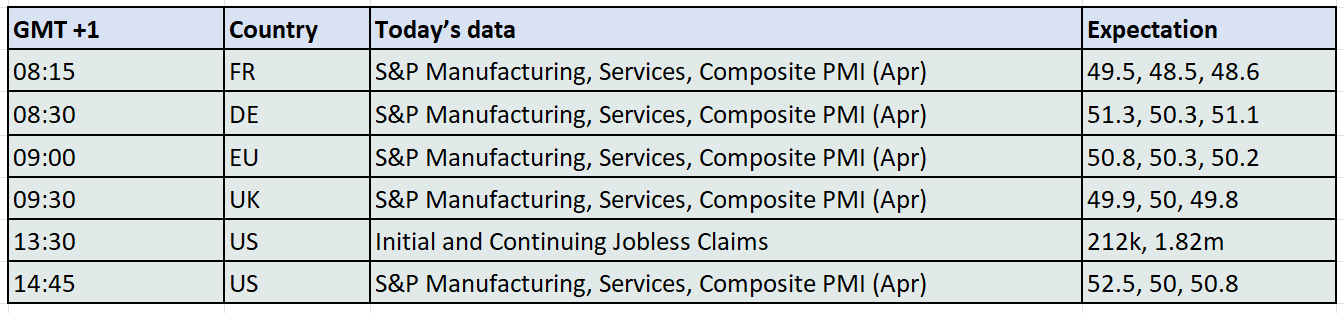

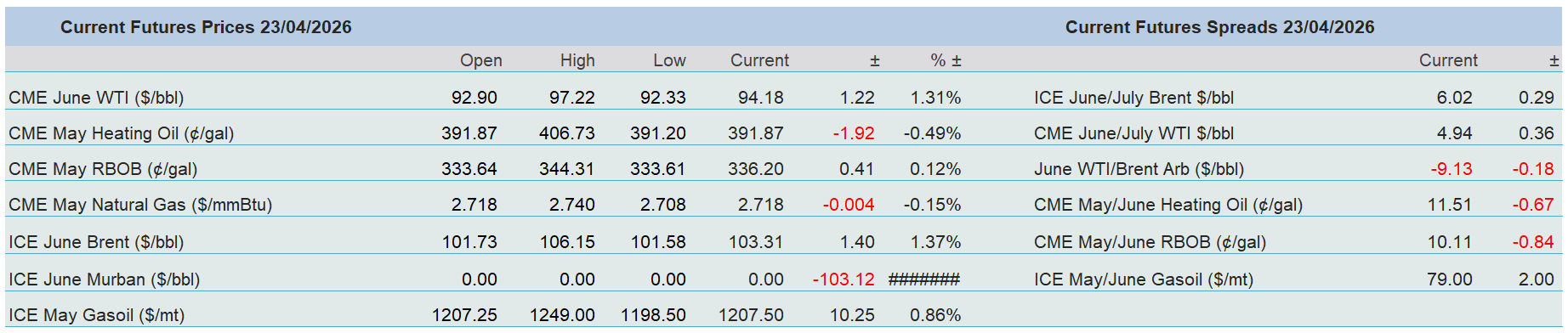

Overnight Pricing

23 Apr 2026