A Change in Syria, But More of the Same from China and Saudi

The amazing scenes in Syria catch most of the eye this morning, which we touch upon below, and oil prices have responded with the normal twitch higher, but in rather quiet fashion for all ponder on what a new look Syria does for the world order. Outside of this understandable reaction, prices might have fared a little worse given the continued backdrop of negative influences. Yesterday, Aramco reduced its official selling price (OSP) to Asia and Europe. The cut into Asia is no doubt aimed at trying to attract more customers after the publicised reduction in demand from China but is a significant 80c/barrel and now stands at the same low level seen toward the end of the pandemic.

This segways conveniently into more troubling data out of the globe's second-largest economy. CPI data this morning yet again reveals deflationary issues, the November month-on-month figure of -0.6% versus -0.4% call and year-on-year 0.2% versus 0.5% expectation shows a populace unwilling to overspend. While November's PPI year-on-year reading of -2.5% against a forecasted -2.8% is marginally better, the issues of over-capacity and lack of markets keeps factory gate prices as a continued poor barometer on how the Chinese economy fares. There might have been a more negative reaction if it were not for the upcoming Central Economic Work Conference in which much hope for direct stimulus is laid. Given that Fitch, the ratings company, this morning downgraded China's GDP forecast, the meeting must deliver or another bout China disappointment selling will prevail. Citing ongoing challenges in the real estate sector and an anticipated rise in tariffs on imports from the United States, the agency now projects that China's GDP will grow by 4.3% in 2025, down from an earlier estimate of 4.5%.

War, war, politics and war

It has always been an opinion of ours the most important event of 2024 was and is the US election. However, what has run close the extraordinary march to the White House of Donald Trump are the points of conflict that have either opened or been rekindled. It has taken nearly all year for oil prices to become used to the scorching of the earth of Israel’s enemies and it has been a lesson hard learned. It is only of late that imaginings that involve oil installations consumed by a many-countries domino fall of production if Iran’s capabilities were targeted have abated. Admittedly, and in an obvious sign of the modern phenomenon of ephemeral interest, the upping of the ante in the Ukraine/Russia war in which the use of US and UK long range missiles have been permissioned, grabbed the attention once again. Conflict premium shifted to the Eurasian battle, and it did not take long for doomsayers to draw a direct line from American and British ballistics versus Russian hypersonics to a full-blown nuclear theatre of exchange. Eventually, and with no regard for the ramifications to human life, markets, and ours in particular, as always work out that wars are bad for economies, bad for business and thus demand. Each aftermath of war or its perception is greeted with a massive bout of selling the fact after the rumour and so the cycle continues.

Why such a reminder of doom on a Monday morning? O, that we were blessed with an equivalent to Nvidia or the AI hope, or even the Bitcoin charge at $100,000, but we are not. Oil is hitched tightly to geopolitical challenges in so many more ways than parochial and elitist investments will ever be, and for the black stuff it is frankly all bad. Hot off the press of things to worry about is Syria. Ten days ago, Bashir al-Assad sat comfortably in his Damascene tower which was propped by an alliance with Russia, Iran and Hezbollah. His brutal put down of a civil war that started in 2011 would never have come about if it were not for the help and presence of the listed benefactors. The remaining rag tag of rebel groups that were penned in their geographical enclaves were likely planning for a New Year sat exactly where they were last year, not marching through Aleppo, Homs and Damascus as the Syrian army made like the proverbial ostrich and put its head in the sand hoping to be ignored.

The collapse of Assad’s Syria is 100% caused by what is happening in the conflicts as opened with above. Us mere mortals do wonder sometimes whether the leaders of the world are engaged a game of ‘Risk’, the strategic board game, as they push pieces of hardware across the borders of opposing countries. Was this part of the Netanyahu plan? Anyway, musings aside, the Israeli policy of attacking first and negotiating later has routed Hezbollah, the very same group that has provided boots on the ground so many times in aid of Assad. It has also caused a rethink in Iran. With proxies falling all the time and knowing that Israel could breach its air defences when and so it feels fit, Tehran has little choice other than to bolster its own military amenities, let alone a puppet that really has little reciprocal value other than spreading word, doctrine and not to fall under the influence of the Great Satan. Similarly, and despite the jaw-jutting bullishness of President Putin, Russian air power can hardly be spared from Ukrainian missions. There remains a pro-Assad area of Syria toward Lebanon and the Mediterranean Sea, but as with all dictators and cowards, and confirmed by Russia, Assad has flown the coop and what he has left is a dangerous vacuum.

Syria does not have the same influence on oil prices that a similar collapse in Libya saw. Its importance is of a geographical nature rather than that of any natural resources. The Syrian border touches Turkey, Iraq, Jordan, Israel and Lebanon, with Jordan the only country not in current conflict either internal or external. There are wide media reports that borders are being strengthened by some neighbours. Is it just that, or is it viewed as a land extension opportunity? Internally, Syria boasts many and varied rebel groups that are currently enjoying necessary mutuality, but will that carry on as victory nears? Among some of the small groups is ISIS and the world is well aware of its nature, indeed, it is reported that the US yesterday undertook bombing of Islamic State positions.

Hope springs eternal, but Syria could disappear into a black hole of malcontent where terrorism and despair can be shared very easily with groups in Lebanon, Iraq and beyond. New battle lines are about to be drawn, nationalist and religious extremism is about to rise and points of conflict increase. All are anathema to trade; all are dampeners of demand. Syria has no direct influence on the fortunes of oil, but the Middle East and the world do not need any more conflict anxiety nor for that fact do oil prices, which invariably end up much lower from whence the worry started.

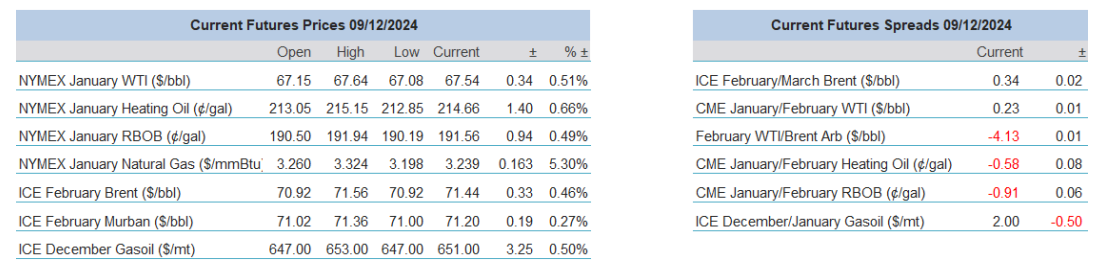

Overnight Pricing

09 Dec 2024