China in focus, again

Technical analysts will be happy with a performance from oil yesterday that involved a bounce from a key technical indicator in the 13-day moving average. However, when the oil market appears to be comfortable in rally of late, it is often the case that China is the number one fire douser throwing a wet blanket over those dreaming for heady 90-handle crude and beyond.

Today China’s barrier to progression for all markets are quite substantial misses on economic markers. The National Bureau of Statistics (NBS) released data showing Fixed Asset Investment year-to-date came in at 3.4% versus last year, below the call of 3.8%; Industrial Production was 3.7% year-on-year (July), below the call of 4.4% and possibly the worst of all, because of its significance to the consumption habits of the population, Retail Sales year-on-year (July) came in at 2.5%, a full 2% lower than the 4.5% forecast. Even with the surprise cut by the People’s Bank of China in the MLF rate from 2.65% to 2.50% it is not enough for much of the investment suite to open defensively.

Indeed, China’s economic position is defensive judging by some of the poor financial press it has received of late. Whether or not US President Joe Biden’s signing of bill to restrict investment in China technologies was an accelerative is debatable, but according to Reuters, US funds have been abandoning China positions at some rate. In quarterly filings institutional investors are reporting a culling of China exposure across a range of industries. The recent short-comings of the property sector is hot on the lips of detractors to investment and Nomura in a note observes that China accounts for 50% of global new home sales and any slump in the housing market should not be underestimated.

On a brighter note (for oil anyway), and staying with NBS China data, China’s oil refinery runs were up 17.4% in July year-on-year, the equivalent of 14.87 million barrels per day (Reuters) and is rated as third highest on record. Even though China’s overall domestic demand is undoubtedly shrinking, its appetite for the massive refining sector would appear undiminished as it seeks to maintain full advantage of continued favourable margin rates.

GMT +1 |

Country |

Today’s Data |

Forecast |

10.00 |

EU |

ZEW Economic Sentiment Index |

Prev -12.2 |

10.00 |

DE |

ZEW Economic Sentiment Index |

-14.7 |

13.30 |

CA |

CPI (July) YoY |

2.8% |

13.30 |

US |

Retail Sales |

0.4% |

Asia and China, it is never straight-forward

The People’s Bank of China reported only $47.80 billion in new loans for July which is 90% lower than that of June’s and such a decrease that the last time these levels were seen was back in 2009. It appears that the recent reduction in the main market lending rates have failed to stimulate the population in taking on personal risk. Much of this risk is clearly defined as property exposure and hot on the heels of the plight of beleaguered Evergrande comes the real estate group, Country Garden.

China’s sixth largest developer has had a succession of bond suspensions and has also fallen foul of missing an interest repayment which can only add to investor reluctance. Not only that, but China’s Manufacturing PMI also has been in contraction for 4-straight months having only been above the expansion 50 number 3 times this year. Factory gate prices (PPI) have been in negative territory all year, leading to a CPI reading of -0.3% in July and therefore deflation. China’s claim, in boxing parlance, of being the ‘great oil hope’ is in fact, just hope. Gone are the days when there were queues of talking heads expounding on a China revival. This was replaced by a rolling ‘eventual revival’ and now to silence.

China is not coming to the rescue of bulls anytime soon. Its domestic situation makes for grim reading and the state of youth unemployment suggests that the economic funk will be hard to negotiate away from in a timely fashion. Markets are also becoming bored of the tepid stimulus shown so far from officials who think if they keep talking big and delivering small repeatedly, investors will believe them. China’s Asian influence pervades the progress of its neighbours be it for ill or good and sometimes both at the same time.

The trouble with having too great of a macro-economic inspired bear attitude at present is that OPEC+, under the watchful and willing swing producer Saudi, have achieved excellent results in tightening up the Asia area oil market. Local, preferred grades are becoming expensive forcing buyers to consider looking elsewhere. Interestingly and adding to the conundrum is that some of the substitute favourites are themselves embattled. Angolan crude’s recent production issues mean this source of replacement is somewhat limited. Urals used to enjoy favourable status too, but it is almost banished from consideration due to sanctions and the breached price cap. The only countries to where the Russian ex-marker does not experience political or legal hinderance in delivery are India and China but even they are reportedly becoming more sensitive to a global frown. Therefore, CPC has logically taken the Urals spot, but it too is not without woe. Bouts of unreliability due to pipeline squabbles between Iraq/Turkey/KRG, poor weather conditions and now the strategic threat from a possible escalation of hostilities in the Black Sea (this refers to a Russian warship firing warning shots at a cargo ship on Sunday) leaves no confidence in security of supply. US Midland is arriving in Asia, as it seems to do all over the world, but not in any incrementally higher volumes compared with recent history and North Sea barrels appear to be closed off due to arbitrage economics.

Even though physical arbs may not be a reality, some of the reported crude tightness seen in Asia gives the notion that crudes are about to sail East creating an implied underlying bid. But China stands in puzzlement to the market. The downturn in last month’s crude imports belies the enormous size of stored inventory which some analysts have at over 1.1 billion barrels. Does this ocean of feedstock sit to serve the refinery industry seemingly having been issued a carte blanche to reap the benefits of global stellar margins? Or if as mused on latterly, does the easy attitude in quota signify stimulus to get any sort of industry moving? It is likely to be both. China’s oil industry and governmental oversight are savvy operators, the size of the domestic crude stock is enough to service a thirsty refinery sector, more than enough to service a stalled economy and large enough to weather any more additions to this rally without having to resort to panic spot buying.

The one thing China has got right is its crude position. It is long and right (due to gorging on discounted Russian barrels); it will continue to buy at a reduced rate thus ‘averaging in’ the price of its current length. The world might expect lower inflows of crude into China but inflows there will be. Will it be enough to help keep Asia crude-tight? Only the resultant effect of turnaround will tell, but the mixed macro-economic messages emanating from South-East Asia’s powerhouse will continue to have mixed effects on oil price thinking.

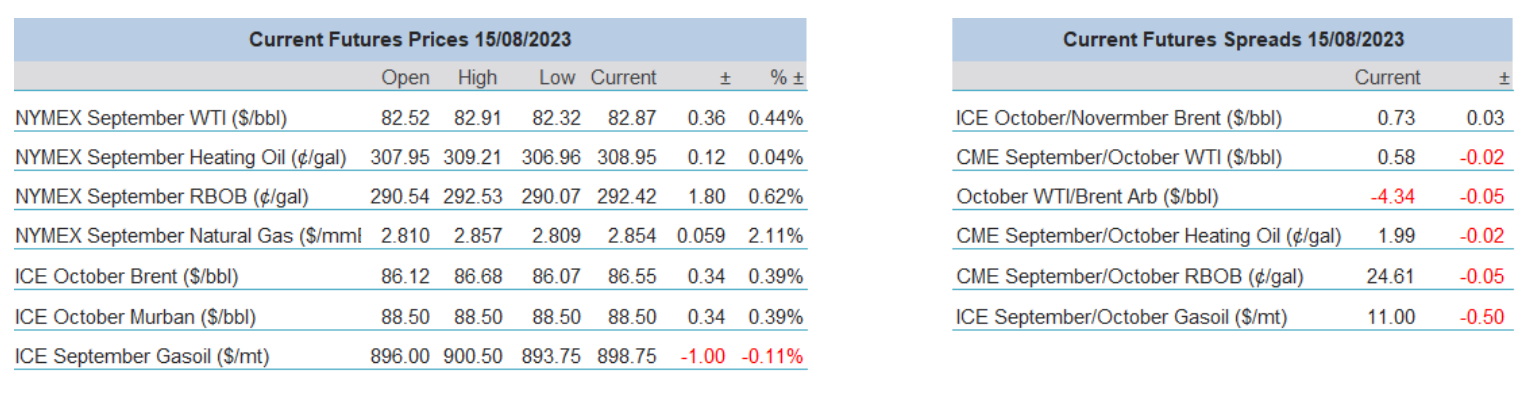

Overnight pricing

15 Aug 2023