Conflict Premium is Back

After months of being on missile watch in the Middle East, the oil gaze turns to the airborne show of military new stuffs being exchanged by Ukraine and Russia. After successive days of permission and use of American and British hardware, Russia ups the ante by shooting a ballistic missile which is the first time such a weapon has been used in the 1000-day old war. President Putin was at pains to point out that the use of the newly developed missile was direct retaliation for the use of Western weapons and warned that the involvement of both the UK and the US risks expanding the war into a global conflict. Oil prices under such circumstances and rhetoric have little choice other than to rally. The influence of energy prices in strategic thinking must mean that the use of such firepower these newly introduced weapons wield will come with a degree of circumspection, after all, their full capability of destruction far outweighs the drones that have been the weapon of mid-range choice during the war. However, it does not matter what limits of use the UK and US give Ukraine, what the market fears is accidental destruction in any part of oil, gas and refining that not only causes long-term damage but accelerates a war spiral. Heating the whole situation is the arrival of some cold weather in Europe and how even the continent's much smaller reliance on Russian Gas remains a real problem for energy security. The market can take into account high US refinery runs, China's monthly decline in oil demand, a prevaricating OPEC and a rampant US Dollar. What it cannot plan for is the tragedy of war and the litany of appalling outcomes if it continues unchecked.

Gas inflates

On Wednesday the UK posted some worrying inflation data that ought to serve notice in Europe and elsewhere for the months ahead. The Office for National Statistics (ONS), registered the first rise in the rate of prices, measured by the consumer prices index (CPI), for three months. Even though there was an expectation of higher inflation the October month-on-month and year-on-year readings of 0.6% and 2.3% respectively, came in a tick higher than consensus which on the face of it does not look that bad. However, the September readings of flat for the monthly and 1.7% for the yearly shows just how much of a jump prices have experienced. The blame in such an increase is laid fully at the foot of increased energy bills, with energy costs and transport also linked. There is little doubt price pressure rose due to last month’s increase in the UK’s energy price cap (it will also rise in January), the maximum amount energy companies can charge for each unit of energy as set by the regulator. But whatever the reasons for gas price rises, they are inflationary, and it will directly impair the ability of the Bank of England to reduce its interest rates.

Therefore, and carrying on from yesterday’s report looking at the fate of gas prices, the significance of the recent retaking of the headlines by the Ukraine war may not just be another example of ephemeral media and our, the consuming readers’, attention flitting from the Middle East because of boredom. Any interruption to gas supplies no matter how small will have great consequence.

Definitive correlation science aside and looking at it from something of convenience to this argument, it is intriguing how European CPI does indeed run in tandem with Gas prices. After the negative inflation readings of the pandemic years, CPI increased dramatically from 0.9% in February 2021 to 5.1% exactly one year later, and at the end of February 2022 after the Ukraine invasion went on to the highs of October and November 2022 of 10.6%. Dutch TTF Gas prices over the whole of the period outline rallied from Eur20 MWh to Eur340 MWh. The intervening period of post-pandemic consumer buying and the realisation on how Russian Gas supplies were to be interrupted, did see a hiatus in movement higher, but without a significant fall in the interim an inflation influence had been established.

‘Assumption is the mother of failures’, so the saying goes but any elongation or elevation in the current warfare between Ukraine and Russia must increase the danger of whatever Gas still supplied to Europe being restricted. This may come from direct infrastructure damage or indeed, Gas yet again being weaponised by inflicting pain on European consumers still reliant on Gas in all its forms for power and heating. Returning to yesterday’s report and how it highlights the spat between Russia and Austria and on how Europe still has some reliance on Russian Gas, the guards put in place such as LNG term deals may not be enough to insulate end users from a hike in prices.

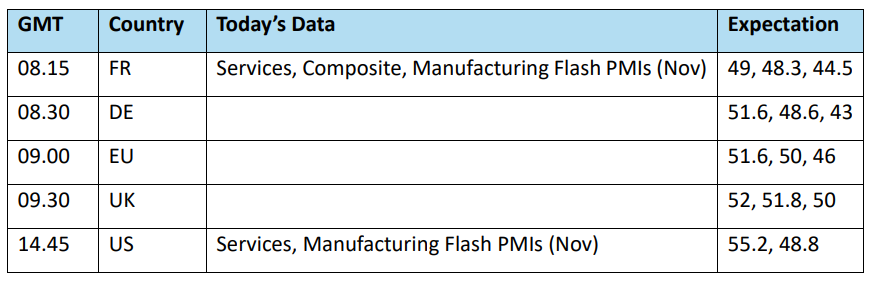

The current European CPI measure is 2.0% and well within the bounds for the ECB to contemplate another interest rate cut. Industrial activity across the continent is in a shocking state as seen in the recent Manufacturing PMIs of Germany, France and the bloc as a whole. With the advent of global trade wars as Donald Trump re-enters office, the European Central Bank must do all it can to pull some of the economies of Europe from the mire of stagflation before any tariffs take bite. However, it does not take a much of jog to memories in how Germany’s economy has been wrecked due to the cold turkey it felt after weaning itself from cheap Russian Gas.

If the Bank of England, and its plans to bolster the UK economy with interest rate cuts is stymied by a change in a price cap, one can only speculate on the impossible task the ECB will encounter if the cycle of higher Gas and inflation levels alluded to here actually sees fruition. Mr Tump brags on ending the Ukraine war in days? Maybe from an economic point of view, Europe might just hope he does.

Overnight Pricing

22 Nov 2024