Conflict Premium Returns

The Middle East war premium comes marching back just in time to save Brent drifting into the ignominy of a $60/barrel handle. Two days of rallies eat at much of last week's 7% loss due to market perceptions of how the pieces of the war puzzle are falling into a timely picture in which Israel finally strikes directly at Iran. A compelling argument emerges that it is due to the US election on why Israel seems intent on keeping the pace of war in such a state. Logically, there is no guarantee of existing relationship under a new Washington administration, and while Donald Trump will be seen as a likely ally for Israel, the mercurial ex-President can hardly be relied upon for consistency. Kamala Harris is an unknown, and although appeasement is always on the lips of the Democratic candidate and that her husband might be the very first Jewish spouse in the White House, the Jewish Chronicle warned in July, "despite her support for Israel, Harris’s sympathy with the Palestinian cause and anti-Israel protesters is a marked shift from Democrats of President Biden’s generation." Yesterday's kicker for oil prices came from unsubstantiated sources that the Iranian Embassy in Beirut was involved in the drone attack on PM Netanyahu's house and that the Prime Minister would hold consultations with specific cabinet ministers, which markets perceived as a quasi-war council. With speculation in some media Israel has completed its preparations for a retaliatory attack into Iran, and overnight news from Tel Aviv confirming the second-in-line leader of Hezbollah, Hashem Safieddine, had been killed last month the current new flare up of conflict sentiment keeps oil markets buoyed. Whatever one's view may be of current fundamentals, of Chinese stimulus, of a higher API Crude build (1.6mb against a 0.3mb call) and the outcome of the US election, the imagined sight and sound of Israeli jets in Iranian airspace will continue to be a much greater influence.

All that Glistens is in Fact Gold

It is truly astonishing to see the rise and rise of the gold price over the course of the year. The precious metal has at times been associated with antiquation and that long-only investment monies might be served better elsewhere, particularly in the realms of crypto currencies and other modern modes of monetary management. However, not only has it reestablished usefulness in being a sanctuary for inflation, it has also been an alternative to the US Dollar which while being the world’s marker currency, is a hard sell for the likes of China and its cohorts who are looking for any excuse to further their cause of de-dollarisation. The historical treasure is very much a-la mode and the term ‘tangible asset’ warms the lips of the investor chattering classes.

Gold’s price has increased by 30% this year keeping pace with the DOW and S&P, double that of copper, smashing the performance of WTI and likely to beat the best previous rally seen in the metal since 1979 during the Iran/Iraq war. Judging by the commitment of traders’ reports, the appetite for gold has increased vastly this year. Net long only positions in Comex gold in February were a lowly 46k lots, as of last week length stood at 235k lots. Overbought? Well yes, the 14-day Relative Strength Index is around 75, above the 70 overbought signal, but it is nowhere near as overly stretched as it was in March and April when it scored 85 on the same scale. Rather than, head down right-angle buying seen during reactionary market times such as the missile exchange between Israel and Iran in April, buying has been consistent with longer-term strategic purchasing and smacks of institutional interest.

Central banks have been a mainstay of demand for gold and while there are varying reasons for nation-state money managers to increase their holdings, the net result is the world’s keepers of fiscal security are determined to keep gold as one of their main hedges against a world full of flux. Protraction of the Ukraine war, the potential for widespread conflict emanating from Israel’s aggressive reaction to the infamous October 2023 terrorism, and antagonism in Sino/US relations are but a few logical reasons for increased inventory. If anxiety is then a driver, none can be more pronounced than the close-run affair that is the US Presidential race. In June 2024 the World Gold Council (WGC) released its Central Bank Gold Reserves Survey and it offers future forbearance in attitude. Banks’ reserves are set then to continue to increase is it has done in recent history. The WGC reports in 2023, central banks added 1,037 tonnes of gold, the second highest annual purchase in history, following a record high of 1,082 tonnes in 2022. In the survey, the percentage of advanced economy respondents who believe that gold’s share of global reserves will rise has increased significantly from 38% in 2023 to 57% in 2024. When emerging market central banks are taken into account, being significantly more bullish on gold’s role, the overall Central Bank expectation is that 81% see gold, as a reserve asset increasing this year.

Donald Trump is all about uncertainty, and uncertainty is all about buying gold at present. Yet, elsewhere, the driver of inflation and its combatant, interest rates, are not finished harassing the world’s global financial system. Interest rates may drop and encourage gold buying again. However, and here is the rub, inflation may go up which makes gold attractive again. Gold interest is systemic, it has many-faceted interest points and as alluded to earlier much of it as an anti-dollar vote. China has increased reserves by nearly 350 tons since November 2022, which is why gold matches the USD move for move when there is a need for investors to take flight and find haven. Gold as a hedging medium, as a representative of heightened sentiment is as old as the hills, therefore, markets should not be surprised at its easy re-entry back into relevance. Its prominence as the pricing commodity for geopolitical and economic risk is set to continue and we can all ill afford to ignore it.

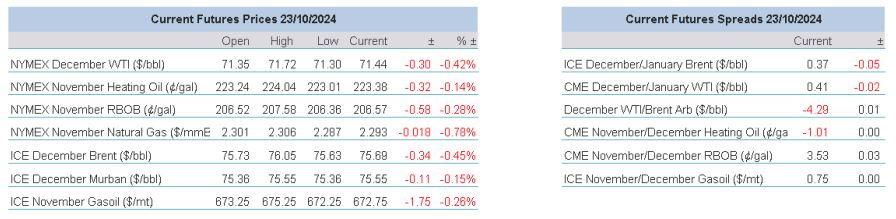

Overnight Pricing

23 Oct 2024