Confusion Rules

There are likely three main reasons why oil prices rallied yesterday, notwithstanding the 10-day ceasefire between Israel and Lebanon announced in the afternoon.

First, while it is undeniably a welcome move, it is temporary, and Hezbollah, which both Israel and the Lebanese government want to disarm, was lukewarm and ambivalent in its comments on the agreement.

Second, the ultimate Israeli goal of removing the oppressive and hardline Iranian regime is still far from being accomplished.

Third, the temporary ceasefire will not automatically lead to a resumption of oil flows through the Strait of Hormuz, at least not immediately. Adding to this, the US–Iran ceasefire is unlikely to be extended, and the US blockade of the Strait remains intact.

Halcyon times of comprehensive and lasting peace in the region remain as elusive as ever. Yet the silver lining is that major developments often take place over the weekend, and the US President’s hint that he may travel to Islamabad if a deal is reached and signed could be a precursor to an eventual agreement. Oil prices produced another reversal overnight as Mr Trump claims that Iran agreed not to obtain a nuclear weapon. A deal is apparently very close. Recent history suggests that words are cheap and are not always backed by action. And even if an agreement is struck, whether it would endure is anything but certain.

Differing Realities

An increasing number of media outlets and news agencies are of the view that oil futures markets are now detached from reality. This assumption is based on the data summarised in the table below, which shows the changes in both physical oil and futures between February 27, the day before the US/Israeli war against Iran began and April 15.

The difference is conspicuous. Front-month Brent futures gained $22.44, the front-month Dubai derivative contract rose by $29.86, but physical oil, such as dated Brent, the world’s benchmark, rallied by $45.60. More strikingly, Forties, a member of the Brent basket, surged by $49.51. The Iranian conflict has greatly enriched Russia, as it is reaping the double benefit of higher oil prices as well as a US sanctions waiver (which might not be renewed). Physical Urals shot nearly $50 higher in the past one and a half months. The front-week Brent CFD strengthened by as much as the front-month Brent futures during the period.

Reality, however, is a tricky concept, at best subjective and biased. It is impossible to determine whether the comparatively tepid performance of futures and other derivatives faithfully reflects the truth, or whether the opposite is the case. A fair conclusion may be that cash oil reflects the reality beyond the Strait of Hormuz, at wellheads, in the tanker market and at refineries, while futures and derivative markets display hopes, expectations, and perceptions of where physical markets might be heading.

The dilemma is how to assess accurately whether futures will realign with the physical market or vice versa. If the inverse correlation between oil inventories and prices holds in the foreseeable future, then futures will need to move higher and not physical prices lower. For this assertion to prove correct, the majority of market participants must agree with it. It is the market that is infallible, not the individual. And updated monthly reports on the global oil balance foresee an exceptionally tight market, particularly in Q2.

Whether the projected supply deficit actually materialises is, again, open to debate. Recent data, nonetheless, points in that direction. If the latest US Weekly Petroleum Status Report produced by the EIA is a harbinger of things to come, then the oil market ought to face very limited downside potential. With almost 600 million barrels of oil stuck beyond the world’s most pivotal transit chokepoint in the Persian Gulf, and growing by the day, and with energy infrastructure badly damaged in the region, competition for available barrels is becoming increasingly intense. Consumers, whether of crude oil or refined products, are forced to look further afield in their attempts to secure whatever supply is available. This week’s EIA statistics provide compelling evidence of that.

US commercial oil inventories declined by 9 million barrels week-on-week, driven primarily by a simultaneous plunge in distillate and gasoline stocks. One might assume these drawdowns were due to strong domestic demand. This is not the case. Although products supplied, a proxy for US demand, remained above 20 mbpd, it has not surpassed the recent peak of 21.64 mbpd recorded in mid-March.

The obvious driver, therefore, is demand from outside the US, which is reflected in gross and net export/import figures. Right on cue, combined weekly US crude oil and product exports, on a gross basis, reached 12.74 mbpd, the highest on record. This comprised 5.22 mbpd of crude oil and 7.52 mbpd of product shipments overseas. On a net basis, crude oil imports fell to just 66,000 bpd last week, a record low, and, for the first time, the US may soon become a net crude exporter. The difference between product exports and imports was 6.09 mbpd, resulting in net weekly US oil exports of over 6 mbpd, an all-time high. Even more striking, this figure is nearly twice the average of the preceding four weeks, suggesting an acute shortage in regions such as the Far East and Europe, which have been heavily exposed to the impact of the Strait’s closure.

This week’s US stock report lays bare the conundrum facing oil consumers and importers. One might argue that the current status quo is unsustainable; after all, the cure for high oil prices is high oil prices. Yet lest we overlook the possibility that an untamed and capricious US President, with a healthy dose of vanity, inclined to gauge foreign and domestic policy through the lens of equity and oil market performance, may feel emboldened to up both the rhetorical and military ante against Iran, with equities at record highs and oil still below $100, in lieu of pursuing de-escalation. What may sound like conjecture could yet prove to be an objective reality.

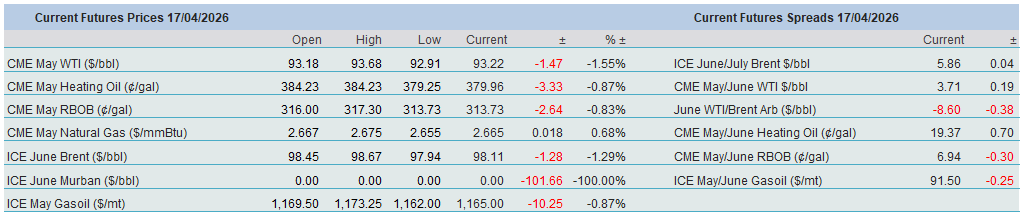

Overnight Pricing

17 Apr 2026