Crudes Give Back Half of the Year’s Gains

What a difference a week makes. WTI and Brent, even more so, were riding a sentiment that continued to ignore the possibility of a Gaza ceasefire, poor Distillate performances and shifting sands from the macro suite while boasting lofty backwardation in M1/M2 spreads. This morning greets a much different looking market that has lost 50% of the value gained this year. The low to high midpoint of 03/01/2024 to 12/04/2024 is 78.47 for WTI and 83.48 for Brent in the continuation of first month contracts. Any vestige of a conflict spread emanating from the Gaza horror has disappeared, much like the recent firework display that Iran and Israel provided the world with recently. Oil prices are now even immune to the ‘stick and carrot’ attitude by Israel over Rafah in which it makes no bones in stating that without serious resolution at the multi-nation brokered talks in Egypt, it will allow the IDF to roll its full forces into the beleaguered southern city of Gaza. Taking away the current geopolitical trigger leaves the market staring into a world of sticky inflation in the US that is countered by interest rates that not only keep the US Dollar elevated but make any sort of commodity trading more expensive.

Aside from this change of attitude in the market’s gaze to current affairs elsewhere, the question of oil inventory comes in to nag at the notion of any tightness in the market. Without going over the Distillate issues again and the failing Gasoline margin, crude stocks and future demand are in the spotlight today and they do not make the best of reading for bulls. A Reuters poll yesterday and other market commentators were expecting a draw in crude inventory of some 1.2mb. Obviously, the EIA/DOE data is awaited, but the API report shows the US crude stocks actually built by 0.5mb, which if confirmed later will make for a 6 in 7 week increase. Slightly removed, but easy to align is the Short-Term Energy Outlook (STEO) that was published yesterday by the EIA. It lowered slightly its WTI forecast in 2024 for both WTI and Brent and expects prices to fall further in 2025 as production grows faster than demand. It upped 2024 US crude production by 100kbpd to 13.21mbpd and forecasts further growth in 2025 to 13.44mbpd. On the global front, liquid fuel consumption is raised by 120kbpd to 102.46mbpd for 2024, reaching a record of 103.67mbpd in 2025. However, the EIA warns that this growth is much lower than 2023 and notes higher production from Guyana, Brazil, Norway and Canada. It also pays heed to OPEC+ production being key to global fuels production slowing down, but at a forecasted 36.4mbpd in 2024 and 37.2mbpd in 2025 the group’s output is at the lower end of potential and the report speculates on whether such constraint will be able to continue through 2024, thereby weighing on prices.

08.30 | SW | Riksbank Rate Decision | 3.75% (-0.25%) |

Circumstance makes for a Russian bear

For all the recent praise heaped upon OPEC and OPEC+ in regard to its, and their patience in seeing voluntary cuts bear fruit in crude oil price increases, none of the accolades or indeed thanks need be targeted at Russia. At the back end of March, Alexander Novak, the Russian Deputy Prime Minister, alluded to Russia cutting production to ease exports for the second quarter of 2024 by 350kbpd and 121kbpd respectively. This then would make up for a large part of the 500kbpd cut promised one year ago and by doing so reduce output to 9mbpd by June of this year.

All fine and dandy then but such moves smack of cynicism and opportunism as outside influences force Russia into something of a corner which are then relabelled as promised production cut adherence. Applying sanctions directly at port are incredibly difficult when considering the so-called ‘dark fleet’ and ship transfers that are shifting Russian oil around the globe. However, and it is not surprising, interfering with capital flows from the proceeds of oil sales is proving to be much more of a telling way to take bites out of the Russian economy. The major oil landings of China, India, Turkey to name but a few have recently gone through a bout of conscience, or should we say compliance, in what is required to stay on the right side of sanction rules. Reuters have lately been contacted by several banking and trading sources informing that cautious financers are asking clients to confirm that oil deals do not break secondary sanctions where US Special Designated Nationals (SDNs) are confirmed in not benefitting from payments.

Defunding the war machine of Russia has developed another layer this year. The drone attacks by Ukraine deep into Russia and targeting oil infrastructure, particularly refineries, has been very successful in causing production outages. Much to the consternation of the United States, worried that such attacks can only make oil prices increase, Ukraine estimate that it has shutdown something close to 12% of capacity, whereas Reuters calls that value conservative as its own reckoning has about 14% of processing shuttered. This equates, by Reuters calculation, to 900kbpd of capacity being offline and with reports that there is a lack of storage in Russia, the need for a production cut becomes apparent and is not just about OPEC+ compliance.

Energy Intelligence has that Russian crude exports in April were 4.73mbpd, matching the level of March and 120kbd below the base agreed with OPEC which was calculated from the May to June levels of 2023. However, for the first quarter as a whole, crude exports were only down 170kbpd versus May-June 2023 and products up 130kbpd making something of a mockery in terms of a pledge to cut both by 300kbpd and 200kbpd respectively. The secondary effect of drone attacks is the obvious build of crude, which, as suggested above has no domestic tanks to drop into meaning it must prepare for export.

Last month, in a Platts/OPEC survey, the nine OPEC nations subject to quotas produced 320kbpd over their targets in March, including excess output of 280kbpd in Iraq, 40kbpd in the UAE and 50kbpd in Gabon. The oil market has become immune to what Iraq says and what Iraq does, it is about to go through the same process with Russia. Funding the war machine is proving harder in the face of the constraints due to increased finance restrictions and how not enough products will make up the export mix. Therefore, the Russian transition on measuring production rather than supply is wounded, maybe fatally. However one measures it, Russia needs foreign exchange and the only way that can be achieved is by increasing the amount of crude getting to water. Such an undignified lack of compliance played out in public can only add to the emerging contention regarding discipline within the oil producers’ group. Will it cause a break in cuts or even a sulk by Saudi as in March 2020 when it threw open the oil spigots? No, the economic backdrop is much different, and nothing now can stop the US shale industry. Yet alliances can only be kept by parties keeping to their side of the bargain and at present Russia will not be able to, and the OPEC/OPEC+ success enjoyed so far might just begin to creak.

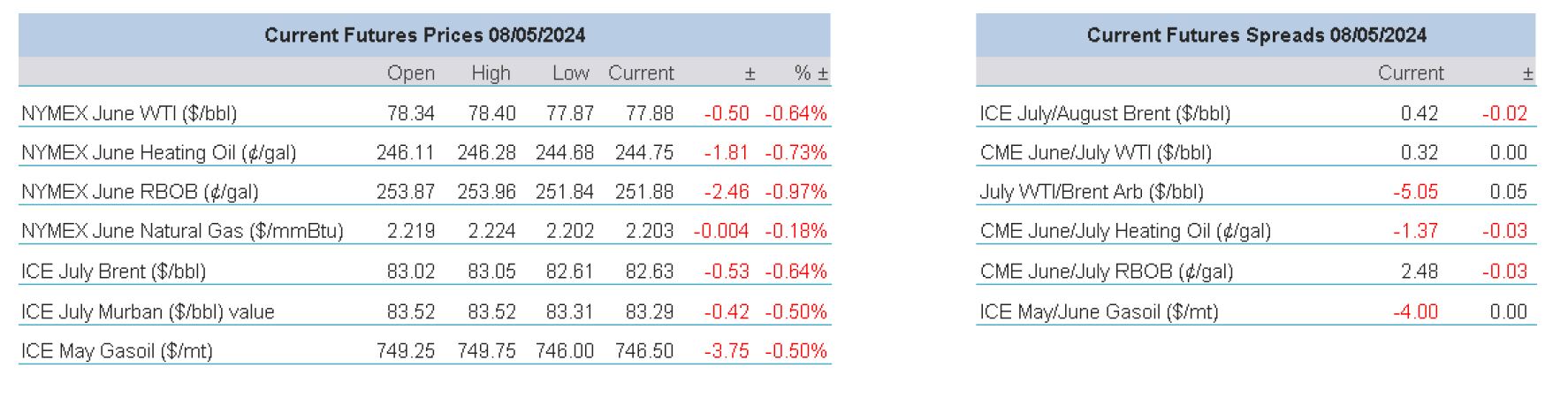

Overnight Pricing

© 2024 PVM Oil Associates Ltd

08 May 2024