Dancing to the Tune of the Dollar

The latest fashionable soundbite in financial circles is ‘immaculate disinflation’. Loosely defined, it means mitigated consumer prices without rising unemployment, which broadly equals impending rate cuts. And the conviction that it will remain the prevalent mantra has been growing of late. Fed policy makers insinuated on Wednesday that they would expect to lower borrowing costs three times this year. The series of cuts could start shortly but not before June as business activity proves resilient this month, jobless claims unexpectedly declined last week, and existing home sales surged last month. The Bank of England is more or less of the same view as its trans-Atlantic peer. Interest rates stayed pat, but the bank strongly hinted that cuts are more of a question of when and not if. The rabbit jumped out of the Swiss central bank’s hat, in the form of a surprise 25 basis points decrease in borrowing costs.

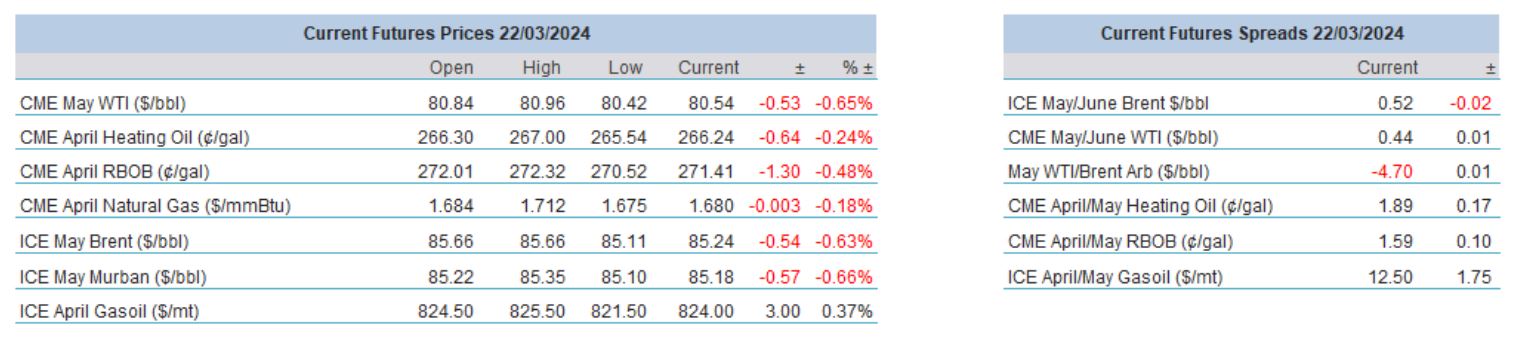

Economies stand on solid legs; rate cuts are happening or will take place and yet what we see is a rather unenthusiastic oil market. Prices drifted lower for the second successive day; this time driven by the dollar. The BoE and the SNB decisions and narratives sent their respective currencies into something of a tailspin and given that the Swiss Franc and the Pound are both the components of the dollar index the greenback strengthened over the day pressuring oil prices further also helped by attempts to revive Gaza truce talks. Protracted downside pressure, however, is dubious. Russian refinery throughput has been adversely affected by Ukrainian drone strikes and, according to latest estimates by Reuters, as much as 348,000 bpd capacity has been lost over the past two weeks alone. Energy Intelligence reckons that the damage amounts to 720,000 bpd, so far, or 12% of installed capacity. The Ukrainian retaliation should inevitably impact the country’s product exports in weeks and months to come.

IEA in the Crosshair of Republicans

Politics is all about compromises. This art is sometimes embodied in thinly veiled or occasionally open threats. When times are changing, lawmakers and decision makers must roll with the punches, they must be pliant enough to change their views and values as they pledge to remain the humble servants of the nation, whatever the circumstances. Over the course of the past 10-15 years the US interest in the world of energy has undergone seismic changes. Given the size of its economy, the country has remained the world’s most salient consumer of oil and other energy resources but with the emergence of the US shale industry it has also become the largest producer of crude oil.

Energy security is the sine que non for every reigning government. Whether it means adequate supply or relatively low pump prices is open to interpretation although the two go hand in hand most of the time. Governments would go a long way to ensure that that its people (the voters) would not be alienated by the rising cost of energy. The latest example was provided by the Biden administration when 200 million bbls of crude oil was released out of the Strategic Petroleum Reserve in order to tame galloping retail gasoline prices after Russia’s incursion into Ukraine although the country’s energy supply was not in jeopardy.

Joe Biden’s predecessor did not shy away from using his political influence to protect his country’s energy interest either. Barely weeks after openly boasting about how plummeting oil prices helped the US consumer in March 2020, Donald Trump played an undeniably pivotal role in persuading the OPEC+ alliance, or better say Russia and Saudi Arabia, to reduce output by 9.7 mbpd in the wake of an oil price plunge into negative territory as the price war between the two heavyweight was raging on. Two years earlier he had tweeted that the ‘OPEC+ monopoly must get prices down’. Then there are times, when the US Congress regularly floats the idea of introducing a legislation called the NOPEC bill, the No Oil Producing and Exporting Cartels Act, threatening to revoke the immunity OPEC+ members and their national oil companies enjoy, which prevents them from lawsuits over alleged price manipulation.

With the transition from fossil fuel to renewables irrevocably under way and with the US presidential elections less than 8 months away the stubborn insistence of OPEC+ to keep output at a depressed level has been, for now, confined to the back of policy makers’ minds as their focus has shifted from the oil producer group to the energy watchdog of major consumers in the OECD. A letter signed by two Republicans, John Barrasso, member of the US Senate Committee on Energy and Natural Resources and Cathy McMorris Rodgers, who is the Chair of the US House Committee on Energy and Commerce, has been sent to the executive director of the IEA, Fatih Birol. In that, as reported by S&P Global Commodity Insight, the lawmakers have accused the agency of being an “energy transition cheerleader” and emphasized that the IEA, by advocating peak oil demand and discouraging investment in oil, natural gas, and coal production, endangers energy security. The diverging views of the IEA and other forecasters, OPEC in particular, on peak oil demand has been well documented and although the former has unexpectedly revised its global consumption estimate upwards in its updated report this month, the gap remains at a yawning 1.27 mbpd for the whole of 2024.

The letter has also demanded that the IEA provides details of its financial support received from the US in the last 10 years as Republican attempts to cut federal funding to the IEA has been intensifying. Clashing interests make any predictions or forecasts about the speed and effectiveness of the green transition ambivalent at best. The latest Republican efforts to undermine the authority of the IEA, whether justified or not, aptly illustrates where the priorities of a potential second Trump administration will lie in the energy sector. It has been obvious that the reliance on fossil fuel and oil within that will be extended beyond 2030 but it appears that the conceivable and ominous changing of the guard in the White House will also aim to reverse most of Joe Biden’s green agenda.

Overnight Pricing

© 2024 PVM Oil Associates Ltd

22 Mar 2024