A Delayed Reaction, But Bulls are Enjoying Themselves

After the FED opened the door for risk appetite overnight on Wednesday, it did take a little while for the ever-present bulls to step through. It also took for the cash market to open and a better reading in Jobless Claims to entice continued buying taking the US bourses to record highs. One can only surmise that digestion of the chunky rate cut had to first dismiss the notion that in some ways it was defensive amid the recent poor employment data which the claims eased. The slight reluctance has now turned into enthusiasm once again, bathed in the flush of a very decent day investors in equities return to their normal modus operandi and start to get excited by the next rate decision even before this one is but a day old. Despite a fairly solid warning from the FED Chair for markets not to expect such rate cuts to be normal, pricing for a 50-basis point reduction in November is now at 43% on the CME FedWatch tool.

Most bourses across the globe act in kind and even the Nikkei keeps a steady track. The fears of a BoJ rate hike this morning were at last quelled somewhat as Japan's central bank held the line. But, with the bank observing private consumption moderately increasing future rate hikes cannot be dismissed. Running counter to the overall mood is the fate of Chinese markets. The PBoC kept its 1-year and 5-year Loan Prime Rate (LPR) unchanged and while yet another idea was floated concerning easing rules on property ownership, any stimulus that markets are looking for still looks a very long way off.

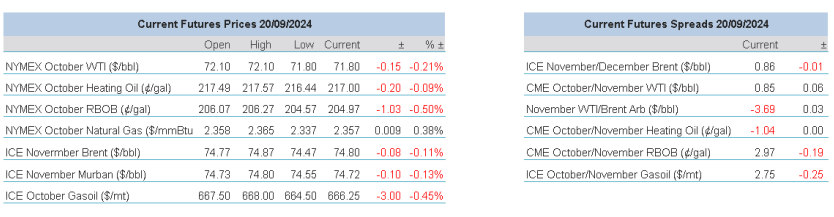

The investor tone and bruised US Dollar influence did not take much time in pushing oil prices on. The curious lack of attention shown to the low crude stocks in the US as evidenced in the 'bottoming' of Cushing levels, was suddenly recognised. However, there is a report shared by Bloomberg from IIR Energy predicting the lightest maintenance season for 3 years, which if correct will not see extra stress in the US oil system. Once again, the Middle East deserves oil attention. Following on from the technology attacks in Lebanon, Israel has been about another swathe of bombings north of its border. With such belligerence from Israel and political howls of protestation that go beyond the proxies of Iran, any vestige of ceasefire talks has all but disappeared. Oil market trading mediums have at last shown efficiency lately. Countering a status of being oversold with a rally of $5/barrel in Brent, enduring the pre-expiry backwardation of WTI and absorbing the spill over enthusiasm from the wider suite, instruments will now rally and fall with actual oil news, rather than positioning.

US Dollar will grow in influence for oil

The plight of interest rates is the go-to influence for all markets at present and oil is no different. Having benefited from years and years of benign borrowing costs, free money that is supplanted with 5% base-costing money is a mind and habit changer in how participants can engage in long-term strategies that involve commodity financing. Still, markets are adept and whatever changes there are in financing considerations, producers, end users, traders et al, do not take much to price in rate concessions or indeed, exclude strategies that become prohibitive. As commodity markets settle into new monetary climes, interest rates become passe and ignored until such time as changes become due. This is obviously not the case within Foreign Exchange markets, and definitely not for the US Dollar.

Immunity to interest rate interference is an impossibility for the mighty greenback. In likeness with commodities, currencies and their values are set by the amount of demand for them. This obviously puts the Dollar in a league of its own. Despite the protestations of many that seek an alternative, holdings of the US currency must be a strategic requirement for all governments. Commodities are priced in dollars, foreign exchange is set and settled against the dollar and international loans are granted and repaid in dollars. Therefore, there is little wonder that the US Dollar makes up nearly 60% of worldwide currency reserves. Its link to the US economy and how the FED manages internal affairs is given an acceleration in importance because of the amount held elsewhere and interest rate sensitivity is heightened.

Consequently, when foreign central banks move the pegs on their own ‘dot plots’, their exposure to the US Dollar has the potential to move it. Lest we need reminding, the recent carnage caused by the ‘carry trade’ in Japan is an example. Borrowing cheaply in Japan to invest into the United States combines many assets but in terms of Forex, it is being short JPY/USD. When the Bank of Japan increased interest rates exposure to the cross-currency position became untenable for some and such was the rally in the Yen versus the Dollar that overnight the US Dollar Index (DXY) lost a whole tick or 100 points travelling from 104.42 to 103.21. The two-year rise in global interest rates, with some exclusions, was a concerted affair. Be it New Zealand’s RBNZ, Australia’s RBA, Sweden’s Riksbank, the UK’s BoE, the ECB and the grandee of all, the US Federal Reserve all chimed with bringing inflation under control and all raised rates in unison.

The global quantitative tightening, however, has had mixed effects and while the US has held onto much of its economic prowess, due in part to being cushioned from the energy price ravages caused by the Ukraine invasion, Europe and elsewhere have suffered diminishing returns in growth and confidence. This then makes the passage back to monetary easing a staggered affair, one in which some centres of trade will experience greater relief earlier and some greater inertia and rates will likely diverge. In such a scenario, as is the case yesterday with the Bank of England’s decision to hold pat on rates as the FED cut, sterling proceeded a rally to 2-year highs. Correlation demands that the USD reprices and by doing so the knock on involves other risk assets including oil. As much as oil prices can become tolerant to interest rates, they, along with many other investment classes cannot enjoy the same disinterest to the US Dollar. Howsoever central banks plot paths of monetary policy, the variations will have continued influence on the world’s marker currency and because the likelihood that ‘easing’ will be an elongated affair, currency disparity and movements in the US Dollar will occur frequently and must be watched.

Overnight Pricing

20 Sep 2024