Do Svidaniya

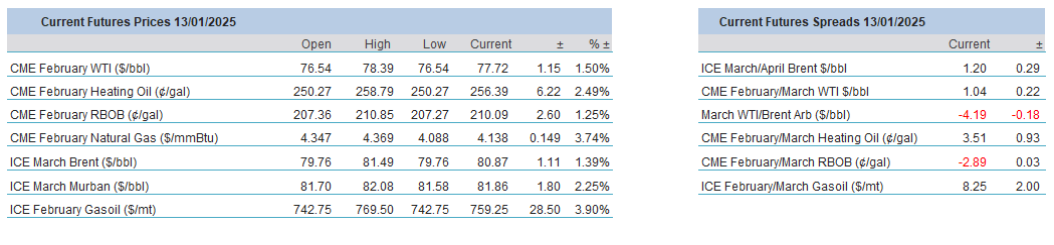

The oil market is like London buses: you wait ages for one then several come along quickly. Oil was gathering strength to break out of its 4Q 2024 range in the latter part of December and the move finally arrived as January kicked off. Better yet, due to a wealth of supportive developments, it stayed above the inflection points. These factors are the cold weather in the US and Europe, the halt of Russian piped gas to the old Continent via Ukraine, low Cushing stocks and the consequent fall in US crude oil exports, declining OPEC+ production in December and falling Chinese imports of sanctioned oil.

One might consider the resultant buoyancy as temporary but when the nuclear option is added to the equation, re-evaluating the situation is necessary. The outgoing US administration presented its farewell gift to Vladimir Putin and Donald Trump. Joe Biden imposed the most severe sanction package on Russia’s oil industry, which aims to deprive the US adversary of crucial oil revenues. Producers Gazpromneft and Surgutneftegas will be affected and so will more than 180 vessels, that ship Russian, as well as Iranian crude oil to willing buyers, particularly to China and India. These countries will now have to look for alternatives and the potential consequence of such a swap was brutally on display on Friday and this morning with Brent rallying briefly above $80/bbl and its backwardation widening. The latest package is certainly a blow to Vladimir Putin but a magnanimous present to Donald Trump as it provides invaluable leverage to the incoming president in his negotiations for peace with Russia.

The medium-term impact of the new measures is unclear. It must be pointed out that there is a wind-down period until March 12 for parties involved and in case a mutually acceptable deal is achieved by then, Russian oil supply might not suffer as much as the current rally implies. Secondly, any tangible shortage could be covered by OPEC’s spare capacity. Thirdly, there is the small matter of dealing with an increasingly pessimistic investor’s sentiment on revived inflationary pressure as echoed in last week’s bond and stock market sell-off and the galloping dollar after the release of strong US job data. Further and protracted increase in oil prices will only exacerbate this pressure and the well-known conditional US political reflex will probably put a cap on the price rise. Unless Russian export volumes suffer discernibly, we suspect the effects of the new sanctions will be short-lived, not so much pricewise but timewise. The first sign of the change in mood will be the narrowing of the backwardation.

Expect Another Turbulent Year

Wars and tensions between powerful nations have always played a decisive role in shaping politics, the economy and the prices of equities, bonds and commodities. The relevance of geopolitics has considerably risen since Russia’s invasion of Ukraine. Throw in the Near East crisis with the tacit involvement of Iran, China’s global ambitions, the advance of the far right in Western politics and the re-election of Donald Trump as the president of the US and the prospect of a utopian world is quickly degraded to the level of wishful thinking. Just like in 2024, the influential consultancy, Eurasia Group, published a paper that lists what they deem the top 10 risks of 2025 on the global stage. It is an essential read for everyone who wants to be prepared for all eventualities in the new year. Below we attempt to sum up the group’s findings.

No. 10 Mexican standoff – The new Mexican President, Claudia Sheinbaum, will face significant challenges in managing her country’s relationship with its biggest trading partner, the US. Mexico will want to avoid tariffs imposed on it by the Trump administration by constraining immigration, and fentanyl trade and make concessions on limiting Chinese investments. Her success in doing so is dubious.

No. 9 Ungoverned spaces – As the US is likely to abdicate its role as the global policeman a vacuum will be created. Global governance will suffer and the multilateral cooperation decline. Non-state actors and rouge states will be emboldened. Conflict zones, not just in different continents but in outer space, the seabed and airspace will expand.

No. 8 AI unbound – Artificial intelligence will be another contentious issue this year and beyond. With all its potential to enhance productivity deregulations and fading international cooperation in the area will increase the risks and collateral damage from the sector. Governments are reluctant to introduce strict regulations because of concerns about losing out on the economic benefits of AI.

No. 7 Beggar thy world – The consensus of healthy global growth might be misplaced. China and the US, the world’s two biggest economies, are ‘set to export disruption’. The Chinese President is focusing on exports as opposed to stimulating domestic spending. Donald Trump’s tariff threats will lead to retaliatory measures inevitably having a negative impact on global growth. Government debt servicing costs will remain high globally.

No. 6 Iran on the ropes – The Middle East as the gunpowder barrel of the world will remain a tangible risk, simply because Iran has not been this weak for a long time. Hamas and Hezbollah suffered unbearable losses as a result of the Israeli attacks post-October 7. The Jewish state might see the current state of Iran as an unmissable opportunity to force a regime change with all the political consequences in one of the world’s largest oil-producing regions.

No. 5 Russia still rogue – With Iran considerably weakened Russia is the world’s largest rogue nation by a country mile. A US-brokered ceasefire with Ukraine appears likely; however, Putin will do everything to keep undermining the global world order. He will be particularly hostile towards European nations with an anti-Russian stance. His military cooperation with Iran and North Korea will continue.

No. 4 Trumponomics – President Trump inherits a solid economy, in which inflation is reined in, and unemployment is low. He will try and remedy the country’s trade deficit with tariffs. China will be hit the hardest and retaliation is impending. American consumers and businesses will bear the brunt of tariffs. Inflation will rise, and the dollar will remain strong further hindering US exports.

No. 3 US-China breakdown – as mentioned above, the relationship between the two nations will sour considerably. Trump’s appointing of China hawks in his administration did not go unnoticed in China and confirms the view that the US will try and unseat the current regime. Technology policy will be a particularly sensitive area in the escalating tension between the two juggernauts.

No. 2 Rule of Don – the rule of law is replaced by the rule of man. Donald Trump’s mandate is much stronger than after the 2016 elections and he has all three branches of the government under his control. He is surrounded by loyalists and implementing his political and economic policies will be smoother than 8 years ago. He will use this power to achieve his objectives. Democracy, however, will not be under imminent threat.

No. 1 The G-Zero wins – The Eurasia Group defines the G-Zero world where no one power or coalition of powers is willing to set a global agenda and maintain international order. In their words, the global leadership deficit is growing critically dangerous. International institutions, from the UN to the IMF, World Bank and WTO, do not reflect the underlying balance of power. Rising tension and confrontation between different actors are the logical ramifications of this deficit.

Overnight Pricing

13 Jan 2025