Don’t Get Your Hopes Up High

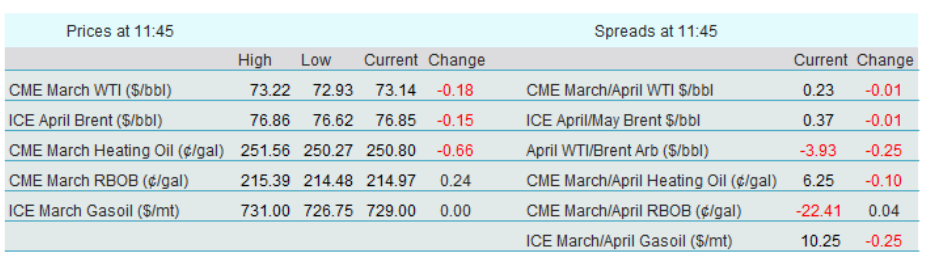

Stubbornly cold temperatures in the US pushed the price of the CME Heating Oil contract up $2.70/bbl equivalent. This, in turn, helped the whole energy complex advance with WTI finishing the day $1/bbl higher. Concerns about declining Russian output and the Israeli threat to end the Gaza ceasefire, if Hamas does not return hostages by Saturday, added fuel to the bullish fire. There are, however, a few red flags emerging on the horizon, which cannot and must not be ignored. The backwardation in the two major crude oil futures contracts is narrowing. The front spread settled at 24 cents/bbl on WTI, the tiniest premium the first-month contract has commanded over the second month since early December. The massive 9 million bbls build in US crude oil stocks as reported by the API leads to some profit-taking this morning. (Distillate and gasoline inventories drew 590,000 bbl and 2.51 million bbls respectively.)

The updated EIA report on global supply and demand paints a bleak picture. Consumption estimates have been left broadly unchanged but predicted output from non-OPEC+ nations has been revised upwards. There is an increasingly less reliance on OPEC+ oil. What it means for 2025 is that after a stock depletion of 530,000 bpd in1Q, global oil inventories will increase at the average rate of 740,000 bpd in the 2Q-4Q period sending OECD stockpiles to 2.805 billion bbls by the end of the year, an annual build of 29 million bbls. The average Brent price will gradually decline throughout the year and reach $72/bbl in December.

Of course, investors are still desperately trying to evaluate the impact of the US sanctions on metal imports. Some clarification came from the Fed. Jay Powell testified before Congress, reiterated his view about the robustness of the US economy, and concluded that no further rate cuts are warranted in the near future. Notwithstanding his optimism, Wall Street was mixed, and the dollar edged a tad lower. This retreat, as discussed below, is plausibly a temporary phenomenon, and no immediate oil price support is forthcoming from the greenback.

The Resilience of the Dollar

Oil is choppy, equities are reacting to fresh developments on planned and actual tariffs as the impact of potential trade wars between the US and other economies is assessed on a continuous basis. Yet, what appears reliably constant in this unpredictable trading and investment environment is the robustness of the dollar. Its index against six major currencies, albeit somewhat below the 2-year peak of 110.01, registered in January, is still strong by historical standards. Its ascent from under 100 in September last year is nothing short of impressive and apart from the spike to 114 in the second half of 2022, it is more expensive than ever since 2002.

There are three major factors the dollar’s current popularity can be pinned down to. To begin with, the strength of the US economy is a shining beacon compared to others, including the UK, the EU and China. Its equity markets have been confidently outperforming other regions of the world. Its central bank, which the US President, so far, does not have any influence on, has not been forced to lower the cost of borrowing at the same speed as its peers. Since May 2024 the Fed effective rates have been cut from 5.5% to 4.5%. During this period the ECB has cut the cost of borrowing from 4% to 2.75%. Whilst it is only a 0.25% difference, the current interest rate gap is the widest for nearly two years as economic prospects diverge. In layman’s terms, the primary objective of the Federal Reserve is to ensure stable consumer prices whilst the ECB, the Bank of England and several other central banks prioritize stimulating ailing economies by decreasing the price of money. This chasm will plausibly widen providing further support for the dollar.

Secondly, in times of external turbulence, the dollar is deemed, together with US bonds, one of the safest assets there is. Its role as the world’s main reserve currency will appreciate. Thirdly, as the US economy is performing comparatively better than other countries, the attraction of foreign capital rises. Investment from around the world in the US increases, which entails higher demand for the dollar. Judging by the economic salvo of the US administration, foreign investment will be further ‘encouraged’ in the foreseeable future, providing an extra layer of support for the greenback.

It is almost axiomatic, that a strong dollar creates an incentive for oil producers outside the US to step on the accelerator because their income will increase in local currencies. The very same but reverse logic applies to consumption. Its impact, therefore, is negative on the oil balance. It also creates economic headwinds, particularly for developing countries, as financing dollar-denominated debts becomes more cumbersome.

So, what would need to happen for the dollar to fall off the cliff, or at least to weaken? It would need to experience collapsing demand, which might be caused by political upheaval, and economic turbulence, precipitated by higher import prices and an anxious rise in domestic consumer prices. Inflation expectations are faithfully mirrored in bond yields, so a sell-off in the bond market and a jump in yields would be an early sign of potentially deteriorating economic conditions.

A weaker dollar, for reasons outlined above, would be supportive of oil demand and act as a brake on production, at least hypothetically. Hedging against inflationary pressure would create financial demand for oil. The impact of the loss of faith in the resilience of the US economy, however, would most probably outweigh the positive effects of a weakening dollar. The view from this chair is that a feeble dollar would only be oil-supportive if it were the product of brighter economic prospects outside the US and not gloomier perspectives in it. We are living in times when neither a strong nor a weak dollar could meaningfully boost physical or financial demand for oil.

Overnight Pricing

12 Feb 2025