Eerily Familiar

There have now been three game-changing wars within the last four years. The instruction for individuals in Gulf states to ‘shelter at home’, and with no commercial flights carving their vapour trails across the skies of the European, African and Asian juncture, there is also an echo of the Covid years. The worry and dismay humankind feels at such threat is robotically equalled in the sentiment of investment markets, and it matters not how much moola is slopping around in institutions, funds and those made rich from the extraordinary run in stock markets, war brings a whiff of nihilism. After Wall Street forged something of a recovery yesterday, no doubt inspired by a latent ‘buy dip’ attitude, Eastern bourses and the stock market index futures in Europe and US are once again experiencing an unhealthy tide of a sea of red. The Hang Seng is down 1.5 percent, Euro and US bourses down 1 percent with the Nikkei still under siege and shirking 2.5 percent. The Japanese index is showcasing the sum of all economic fears as it contemplates a future where it might just have to seek higher priced alternative energy supplies other than those from the Middle East. Bottleneck inflation that inspires higher interest rates sounds all too familiar and there probably is not a greater potential of economic constriction than that of the Strait of Hormuz. The flight to the US Dollar and Gold is a predictable outcome, but what is not, and what markets hate, is how long this latest episode of world self-harm will continue.

Time, the greatest gift of all

When assessing the future for oil prices, it is more than easy to hide behind the complexities and fluidity of the ongoing crisis in the Middle East. The idea is to presume nothing but prepare for everything. How one does that might create a flow chart that only artificial intelligence bots could plot. Yet the biggest judgement, as it has always been, is timing. It is to the longevity of attacks on Iran from the US and Israel and the retaliation of the Islamic State on neighbours that will determine the track of where oil prices will travel to. Yet, even if there are a sudden breakout of diplomacy and a cease to arms, the anxiety of unfinished business will reside. After the ‘Midnight Hammer’ attacks by the US on Iranian nuclear sites last June, many, including us, thought on how this could be a mapping operation and a calling card from the USAAF saying it would be back some time soon. But not to this extent. No-one could have predicted the level of diplomatic frustration and how the most anti-war US President became the most war-like in recent history, leading to where we are today. But if by some strange turn of events a truce is found and talks resumed, oil prices will not be lulled into complacency again.

At the risk of being on the wrong side of Donald Trump’s five-minute attitude to geopolitics, it is difficult to see how his active call for regime change in Iran can be walked back, and with whom now will the US negotiate after the regicide of Ayatollah Ali Khamenei. The language is inflammatory from the US and Israel, and pugnacious from Tehran, as reported in Middle East Today, Iran’s top national security official, Ali Larijani, said in an ‘X’ post yesterday that his country would not negotiate and added the Mr Trump had “delusional ambitions.” Iran has no intention of folding quietly. Whatever conflict-spread the world envisaged at the start of 2025 due to Gaza has happened in February 2026 in an instant. Including the US, Israel and Iran; 12 countries have experienced direct military involvement. Lebanon is paying the price for sending missiles into Israel as revenge for the death of the Ayatollah. Paramilitaries in Iraq have been subject to US attack. Kuwait has seen the deaths of US military personnel, with additionally UAE, Bahrain, Oman, Qatar and Jordan all feeling the hand of Iranian retaliatory attacks for being allied with the United States, with British bases in Cyprus being subject to the attention of drones.

Without a leader, one wonders if these attacks have been something of misstep. Instead of concentrating on US bases, the civilian attacks along with the targeting of oil and gas assets are being considered reckless by those on the receiving end of Iran’s ire. The Gulf Cooperation Council (GCC) of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and UAE had for months offered sympathetic overtures to Iran, would not let US attacks be launched from their soil and were beginning to deem Israel as the regional threat to safety. As reported in the Guardian, the UAE has withdrawn its ambassador from Tehran in protest and claims Iran has launched more attacks on its territory than on Israel. If the tactic is to soften up its neighbours and force them into petitioning the US to return to negotiation, then at present it has backfired.

There are more questions than answers on how alliances, when under such strain, will develop or indeed, survive. The likelihood is that most will choose not to alienate the United States, but how they dance a diplomatic two-step with Iran so as not to see missiles rain down on their oil assets or even worse, civilians, can be only revealed in time. Meanwhile, oil communications are broken. They have never really recovered from Covid or Ukraine and if the sensitivity seen in how ships were reluctant to traverse the Red Sea during the Gaza conflict because of Houthi attacks, the closing of Hormuz is so much more delicate. The US can brag all it wants and will probably achieve a neutralising of the Iranian navy and the IRGC boast of closing the vital Strait of Hormuz artery. But if a few haphazard missiles and drones forced diversions from Suez, that threat will be seen doubly, trebly or more in Hormuz and by many more proxies. There is no optionality in the Strait of Hormuz, Red Sea vessels had the luxury of diverting around the African Cape.

We read of high-flying freight rates last week, something we will no doubt touch upon in the coming days, but shipping just became even more expensive because insurance companies will start to abandon their risk on vessels that secure their income by plying oil in an out of the Arabian seas. We can dwell on localised glut, localised shortages, collapsing or rallying arbitrage and refinery margin disparity depending on geography, because oil communication is bust. Then there are currency moves and inflation with the oil price suddenly going to the top of the list of wider market considerations. But we will finish as we started and hide behind how all the effects we have touched on here, and countless more not named, brought about by war in Iran can only oblige us in fruition by how long this state of war exists.

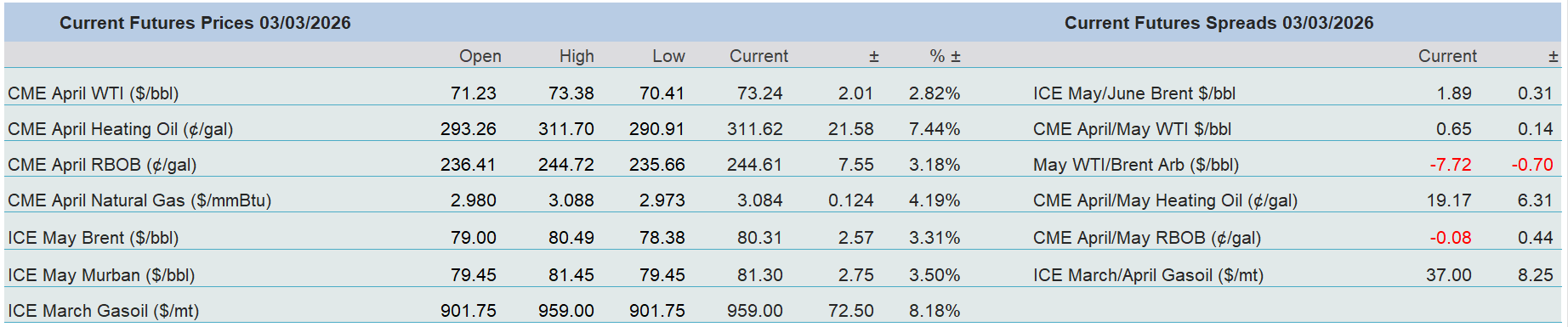

Overnight Pricing

03 Mar 2026