Equivocal Bull Revival

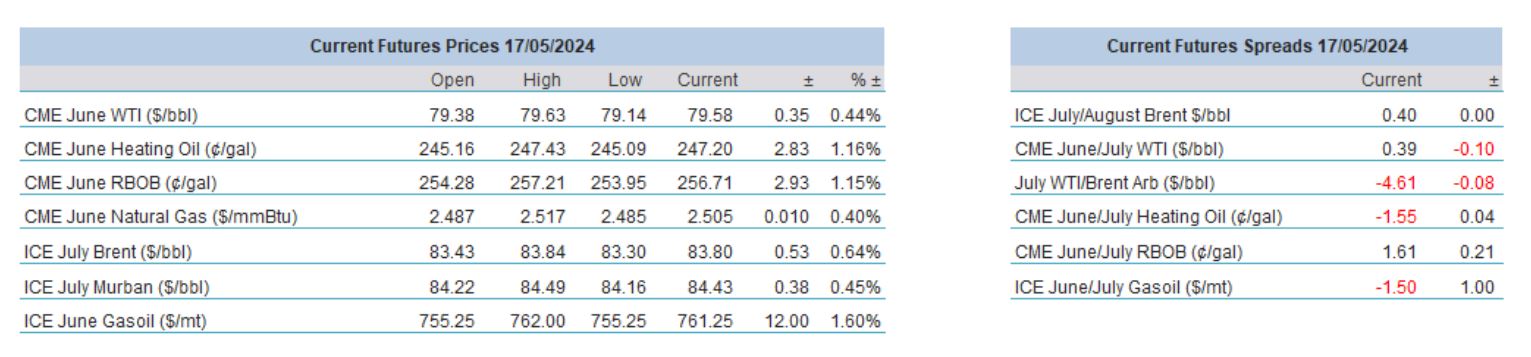

Brent reached its annual peak of $92.18 on April 12. Yesterday it settled at $83.27/bbl having been as low as $81.05/bb on Wednesday. The burning, albeit rhetorical, question is whether the summit will be re-visited first or another $10/bbl will be shed as optimism has seemingly gone AWOL. Equity markets do their best to support oil. The MSCI World Index returned 7% since April 12. The Nasdaq Composite Index registered 8 daily gains in the last 10 sessions. Bond yields rose yesterday but have fallen considerably in May. The dollar has been weakening. US April CPI data encouraged investors on Wednesday. Initial jobless claims were down 10,000 last week, a sign of job market consolidation. US manufacturing output unexpectedly plunged in April underpinned by high rates. Hopes of rate cuts in the foreseeable future are on the rise again.

Israel’s assault on Gaza continues unabated and peace talks have broken down. Russian seaborne product exports dived 15% in April, Reuters calculates. OPEC envisages a massive supply deficit for the remainder of 2024. Yet, the oil complex fails to convincingly recover from the recent slump despite the advances of the past two days and this morning’s strength aided by rising Chinese industrial output and renewed attacks on Russian oil infrastructures. The lack of explicit enthusiasm is probably the function of tepid product demand depressing refining margins. Additionally, the great unknown is the next move the OPEC+ producer group is contemplating. The forthcoming summer driving season might revive the fragile gasoline market on the northern hemisphere and in case OPEC, as a display of solidarity, leaves production ceilings unchanged at the beginning of June, prices might start the hazardous climb towards the 2024 peak. Lots of ‘mights’ and ‘ifs’ but those who are bold enough to hold their breath until $90/bbl comes into sight again might just struggle through the next few weeks without encountering serious respiratory problems.

GMT+1 | Country | Today’s data | Expectation |

10.00 | Euro zone | Core Inflation rate YoY Final (Apr) | 2.7% |

10.00 | Euro zone | Inflation rate YoY Final (Apr) | 2.4% |

Unchanged Baselines, Unchanged Quotas – for Now

When energy ministers from OPEC and their non-OPEC colleagues come together in Vienna the purpose of their meeting is to discuss production levels going forward. Sometimes it is nothing more than formality. During the health crisis when discussions were held in the virtual space agreements were reached within minutes. Other times, talks can get heated. The alliance’s target is to balance the oil market and bring supply in line with predicted consumption but there is understandable competition within the group as member states usually try to demand more auspicious conditions for themselves than their peers.

The upcoming Joint Ministerial Monitoring Committee meeting, which is a little over two weeks away is likely to be a non-event unless production levels beyond 2024 will be discussed. Although Iraq fired a shot across the bow a week ago by declaring that it would not agree to any extra reductions in oil output as it feels it had sacrificed enough to support the market, it quickly backtracked on its claim. (It is one of the member countries with the most flexible attitude towards compliance.) The June meeting might prove to be the calm before the impending storm.

Whilst investors are chiefly concerned about quotas and actual production levels, the coalition of oil producers bases its ceiling on baselines and talks will plausibly intensify when the 2025 strategy is laid out and centered around this standard. As Energy Intelligence points out, the organization has commissioned three consultancies to run independent assessments of production capacities and present the result by the end of June. Since this deadline is a few weeks after the upcoming JMMC meeting it indicates that re-negotiating of baseline will possibly be on the agenda post-June. Still, it is a useful exercise to take a look at how production capacities, using IEA estimates, relate to production quotas and attempt to draw a conclusion which country might be in the position to call for an increase in baseline – and hence in quota.

Production capacity, logic dictates, should highly correlate to baseline and to quota, yet what one finds is that this ratio greatly diverge amongst member countries. On one end of the spectrum is Nigeria, whose production capacity of 1.5 mbpd equals to its baseline and its quota. There is no potential to increase baseline, its leverage is 0%. The other extreme is the UAE. Its production capacity of 4.3 mbpd compares to a base production figure of 3.219 mbpd and to a quota of 2.912 mbpd equating to 34% and 48%, respectively. The same figures for Saudi Arabia are 16% and 36% with a production capacity of 12.2 mbpd. The voluntary supply cuts from the latter two are responsible for the differences between baseline and quota.

In the non-OPEC segment, the two salient countries with significant production capabilities are Russia and Kazakhstan (Mexico is not bound by output restraints). The former ought not to be part of the calculus since there is a strong case that given its ongoing violence against Ukraine and its chronic need to finance its war, it will always pump as much as it can regardless how it labels its production levels. Kazakhstan’s production capacity is 4% above the baseline and 16% higher than its limit but it routinely overproduces. Yet, it reportedly requested higher production level for next year.

Baselines and production quotas are out of line with production capacities, it appears that the playing field is anything but level, admittedly partly because of the voluntary reduction in output from several producers – some countries’ baselines are disproportionately below its capacity compared to others. The numbers suggest that only those with voluntary cuts could justify increased baselines and consequently higher ceilings, at least on paper. Saudi Arabia is unlikely to do so as the Kingdom is targeting tighter oil balance and higher prices because of its budgetary needs. The UAE is the great unknown. It has rocked the boat in the past. By increasing its production capacity, it has claimed higher baseline – and got it. A renewed attempt to do the same together with requests from others to elevate baseline/quota could not be ruled out when 2025 will be on the menu, especially if the independent assessments, as expected, will be passionately deliberated. Again, apart from the 2.2 mbpd voluntary cuts that expires at the end of next month, we would not expect quotas and baselines to be a topic of contention in two weeks’ time (the meeting could be held online), but delicate and potentially perilous negotiations are anticipated beyond that. The producer group must show unity, yet in these precarious times nothing can be taken for granted. Supply war is not an unheard phrase amongst allies.

© 2024 PVM Oil Associates Ltd

17 May 2024