Exhausting, but Never, Ever Dull

In two-weeks’ time at the expiry of the first interim trade agreement between the US and China, President Trump will have the final say on whether a copycat ninety-day extension will then commence. As a stability move, it is fine and dandy, but even the most avid optimist could not sell it as a closing-in on a final solution. That may only happen if Presidents Xi and Trump meet and despite the public goodwill aired from both sides of the respective negotiating teams, such a sit-down is unlikely much before the year’s end. Unlike the EU, China will be no supplicant to the ways of Washington. It is evenly matched in terms of negotiating firepower with its geological assets of rare-earth minerals being the top of its arsenal. However, both sides realise that a full-blown trade war between the two largest trading nations on the planet would be disaster for the global economy, therefore, the extension seems logical while time is banked in pursuit of an equitable outcome.

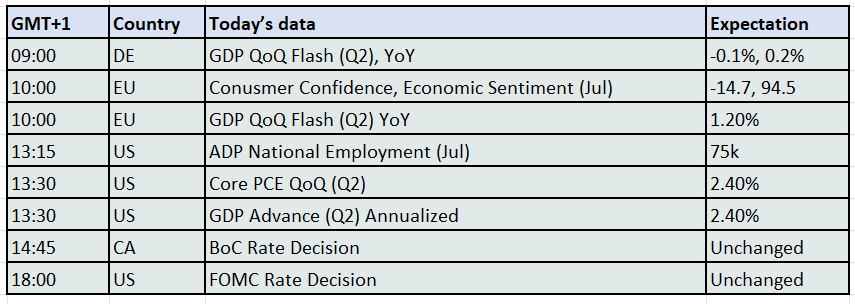

Trade anxiety will still exist though; there are many nations who have yet to come to terms with the US before Friday’s deadline. However, with Japan, the EU and probably China put to bed for the moment, eyes will divert to the tier one economic decisions and metrics of the week, all spiced with very important corporate results. Today alone sees economic sentiment markers from Europe, but the docket from the US will take all the concentration markets can muster. Not only are there advance readings of second-quarter GDP and PCE Prices, but the ADP Employment data is also out in front of Friday’s Non-Farm Payrolls, all topped off by the rate decision from the Federal Reserve. Incidentally, there is a rate decision from the Bank of Canada, but it will get lost in the noise of its neighbour’s data fortunes. The FED is almost nailed-on to keep rates unchanged, but it is to the press conference and comments from other members of the FOMC that wires are eager to hear and whether there is any sort of division brought about by the continued Trump interference. If such meaty influences are not enough to sate one’s attention, then maybe the results of Meta, Microsoft, eBay and Ford will fill any leftover space for absorption.

Removing Russian oil is good as a soundbite....

Oil prices over the last two days had every right to react in upward motion. Emboldened by his incontestable win in the European trade negotiations, US President, Donald Trump, then set about using his golfing holiday in Scotland as a forum to address all the woes and ills of the world with sweeping decrees of intent, covering uranium enrichment in Iran to food drops in Israel. His largesse in opinion knew no bounds as he then turned attention to a non-compliant Russia, and how it refuses, under a cloud of seemingly agreeable obfuscation, to sit at the table of a convened Ukraine ceasefire. Maybe it was the heady mix of Scottish heather and a par at Turnberry’s famous par-3 lighthouse hole or probably that another world leader, Ursula von der Leyen had fallen foul to the art of the deal-maker-in-chief, he appeared to be emboldened and at his shooting-from-the-hip best. Declaring that his frustration with Vladimir Putin would now see the fifty-day time limit set on the 14th of July for Russia to begin ceasefire talks before secondary sanctions would be imposed, cut to a now ten days and repeated yesterday, once again brings the idea of a tighter market to oil thinking.

Days or numbers seem conversational to the President, they appear arbitrary and ill thought out, but on the off chance that one such announcement might actually stick, oil practitioners needed to react. It is only after, that retrospection comes in but taking the threat at its word, and secondary tariffs eventually take Russia’s oil from the market the effect would be great. The IEA estimate, as seen on Reuters, is crude exports from Russia amount to some 4.68mbpd with another 2.5mbpd of products leaving its shores. The main beneficiaries of Russian crude remain China and India with the latter being much more vulnerable if sanctions are indeed pursued and enforced. India imports around ninety percent of oil requirements with up to 1.7mbpd being Russian feedstock. The trouble for India, is that it is much more geopolitically tied with the United States, and Delhi, unlike Beijing cannot afford to cock a snoot at Washington. With a trade deal between the US and India yet to be finalised, negotiations are layered with potential stumbling blocks including India’s support of Russia’s oil industry. Alternative crudes will have to be sourced and while Saudi and its OPEC cohort would be more than willing and able to fill-in, the time it takes to solve the lag will add another prop to near-term price strength. China could not care less, no matter the warning from US Secretary of the Treasury, Scott Bessent, that it would face higher tariffs if it continued in its oil dealings with Moscow. It has extensive pipelines from Russia and seaborne increases of ESPO and Sokol grades and no doubt Urals would all be welcome. However, if the South-East Asia trading giant ends up being nigh on the only lifter of Russia’s oil, one can only imagine the arm-twisted discount it will be able to negotiate, forget the European price cap.

If we accept that it would be 7mbpd of combined oil that might start being removed from the market in ten-days’ time without immediate substitutes being quickly available, we must accept then prices will at least in the short-term soar. However, that acceptance very much relies on the supposition that Mr Trump will indeed go ahead with secondary levies. His ability to flip-flop is now almost legendary and his recent successes in trade deals has much to do with the seeking of certainty from counter parties as it has to do with their believing he would hang tough on his punitive tariff threats. Wander across many opinion pieces and they will example how the supposed twenty-five percent secondary tariff on Venezuelan crude has never been exercised, it is not price convenient. One sure-fire way to get a grumbling American electorate is to hit them with a double-whammy of high inflation and fuel prices. As trade deals are announced, with questionable clarity, they will give an opportunity for those who have held opinion on tariffs being inflationary to be made correct. Insert a period of prolonged Russian oil absence not only will crude and refined fuel prices rise, so will every conceivable nature of goods. Vladimir Putin knows this. He has already looked into the eye of the deal-maker-in-chief and he has found his poker player’s ‘tell’. That ‘tell’ is high oil prices. We do not believe President Trump will take away the ability of Russian oils to make it to customers, well, if he does the price pain will induce a moratorium. At present, the oil market does not believe it either, Brent would be $80 minimum, not $70/barrel if it did.

Overnight Pricing

30 Jul 2025