Failed Peace Talks, Falling Popularity

An eventful weekend saw the first direct talks between the US and Iran in nearly 50 years bear no fruit, while the MAGA movement suffered a significant setback. After declaring a two-week ceasefire last week, negotiations between the warring parties failed to produce an agreement. A predictable chasm in views and objectives, such as Iran’s nuclear ambitions and the reopening of the Strait of Hormuz, proved irreconcilable in Pakistan. The US vice president stated that Iran refused to commit to never acquiring a nuclear weapon, while Iran described the meeting as being characterised by mistrust and suspicion. Uncertainty, therefore, persists, and since the US president decided to blockade the Strait from 10 am Eastern time today (not targeting ships from non-Iranian ports), the fragile truce is as good as over, with the flow of oil unlikely to resume in the foreseeable future. Oil is back above $100/bbl.

If ending this war of choice represents an undeniable reversal of fortune, further bad news arrived for the US administration and the president, a few thousand miles northwest of Iran. One of Donald Trump’s most loyal and unconditional allies in Europe, Hungarian Prime Minister Viktor Orbán, suffered a crushing defeat in the weekend’s parliamentary election. Not only did the US and the MAGA movement lose a faithful servant, but the European Union will likely feel emboldened in negotiations with the US on Ukraine, NATO and even on trade. In fact, considering that last year liberal prime ministers in Canada and Australia were elected not despite the US president endorsing their far-right opponents, but because of it, it is tempting to point to growing evidence of a “Trump curse.” It appears that crony capitalism and economic mismanagement can be tolerated for so long, a stark warning to the US. The Iranian reluctance to bow to US demands and the diminishing popularity of nationalist movements in Europe serve as a reminder that Niccolò Machiavelli’s saying—“it is safer for a leader to be feared than loved”—may no longer apply to Donald Trump, as both his approval rating and his fearsome image appear to be in decline.

Whether this shift toward the centre of the political spectrum will continue in other countries, further undermining what the MAGA movement stands for from social, political, and economic perspectives, remains to be seen. What is becoming increasingly apparent is that the Iranian war has upended short- and medium-term expectations for the global oil balance. Before the joint US/Israeli attack on Iran began at the end of February, there was a consensus that the market would be oversupplied in 2026 and 2027, gradually turning into a deficit toward the end of the decade due to insufficient investment in exploration and production. The conflict and the closure of the Strait of Hormuz have created an acute supply shortage, pushing oil prices above $100/bbl. What was expected to be a well-supplied market has turned into a race for available barrels. Elevated oil prices will undoubtedly increase pressure on consumer prices, as illustrated by US CPI data for March and rising Chinese producer prices. Global and regional economies will inevitably come under strain, and central banks may be forced to raise borrowing costs. The damage precipitated by the Iranian war, however, is proving so severe that immediate price fall is unlikely, even if the Strait were to reopen tomorrow.

Re-establishing the Status Quo Will Take Time

Wherever one looks, there is ample evidence that the global oil market is gradually becoming paralysed, and the current shortage will not disappear overnight. Ship-tracking firm Kpler, as cited by Energy Intelligence (EI), estimates that around 200 tankers are stranded behind the Strait, holding 132 million barrels of crude oil and 40 million barrels of refined products. This backlog will clear in months, rather than weeks. What was expected to be a well-supplied second quarter in February (+3 mbpd), as reflected in the EIA’s monthly Short-Term Energy Outlook, has turned into a 5.1 mbpd deficit. Although the EIA currently expects a global stock build of 300,000 bpd in the third quarter, this figure will be revised meaningfully lower if the Strait remains closed. OPEC’s second-quarter output (crude oil and other liquids) has been downgraded from 34.26 mbpd to 27.01 mbpd. Energy Intelligence estimates that OPEC-12 March crude oil production fell to 19.94 mbpd from 29.47 mbpd in February. Similar revisions are likely from OPEC today and the IEA tomorrow. It will be interesting to see how inventories, as measured in days of forward cover, a useful gauge of tightness, have evolved.

Weekly data also point to a growing oil shortage, particularly in refined products. Although total US commercial oil inventories have increased since the end of February, distillate stockpiles have fallen by 6 million barrels and gasoline inventories by 14 million barrels. In Europe’s ARA hub, as reported by PJK International, total product stocks declined from 5.86 million tonnes at the end of February to 4.91 million tonnes for the week ending April 10, with gasoline and gasoil accounting for almost half of this decline. In Singapore, a 2.5 million barrel drawdown in gasoline stocks between early March and early April stands out.

The impact is most acutely felt in Asia. After all, more than three-quarters of the oil flowing through the Strait of Hormuz is destined for the region. Several countries in the Far East have been forced to introduce emergency measures, including export bans on refined products, the use of strategic reserves, work-from-home mandates, and speed limits. Europe is not immune to the consequences of the closure of this pivotal chokepoint. Heavily reliant on the Middle East for nearly half of its jet fuel needs, the region is also adversely affected.

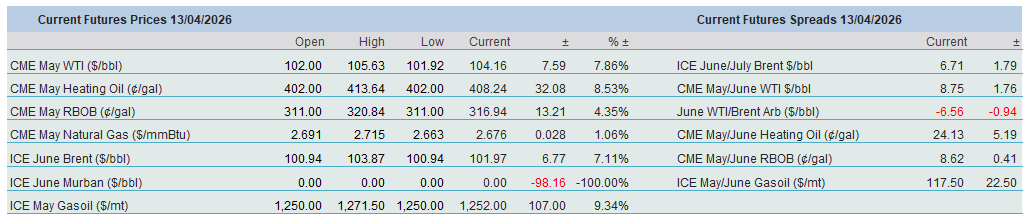

As concerns over supply shortages show no signs of abating, the US has emerged as the marginal supplier of both crude oil and refined products. US crude exports are rising and are expected to increase further in the coming weeks. The Financial Times, citing Kpler estimates, reports that around 68 empty tankers are en route to the US, nearly triple the number seen at the end of February. This development is providing strong support to WTI relative to Brent. The June arbitrage has narrowed from -$21 on March 20 to -$5.62 by Friday’s close. Although the heating oil crack spread has weakened somewhat recently, at above $60/bbl it remains historically strong. Given that US diesel is being shipped as far as Australia and jet fuel is in high demand in the UK and Europe, US product exports are also set to rise, and no collapse in distillate crack spreads is anticipated.

The Iranian conflict is proving to be an ill-fated war. An autocratic and ruthless regime with nothing to lose will not obey the dictates of a coercive US. Tensions and hostilities will continue to flare up, and the end of the conflict is not nigh. Only a regime change in Iran and/or an abdication in the US would definitively settle the conflict, which should not have begun in the first place. And we all know the disheartening odds of either of these possibilities.

Overnight Pricing

13 Apr 2026