FOMC worries the market

A reported divided view in the minutes from July’s FOMC meeting continues to haunt markets and the risk-off attitude sees a follow on into today’s session. Although the views stated were not all bad and indeed, the FED’s own analysts pulled back from their predictions of a recession and forecasting a gradual fall in inflation into 2024, the market in its current mood dwells on the negatives. Among the warnings noted from FED members, and paraphrased, were that inflation was unacceptably high and that the labour market remained very tight. The economy needed to be below current levels of growth and a softer labour market required to achieve economic balance.

However, what really skittled confidence, and with the warning of higher inflation in mind, members accepted that there might be a need for further monetary tightening for which the market immediately presumed to mean another interest rate hike. After the front of the week saw investors suffering from some abject economic data from China, any salve usually found in US investments has for now, abated. Yields continue to rise, which they had done already due to China, dampening risk appetite but the biggest gainer and barrier to all markets is the US dollar. Having spent the early part of the week sitting steady at 103, the US dollar index (DXY) has now pushed on to 103.50 and unfortunately there is not an investment article that can survive the scrutiny of such a jump in the greenback, not even an oil market that is drawing down stock.

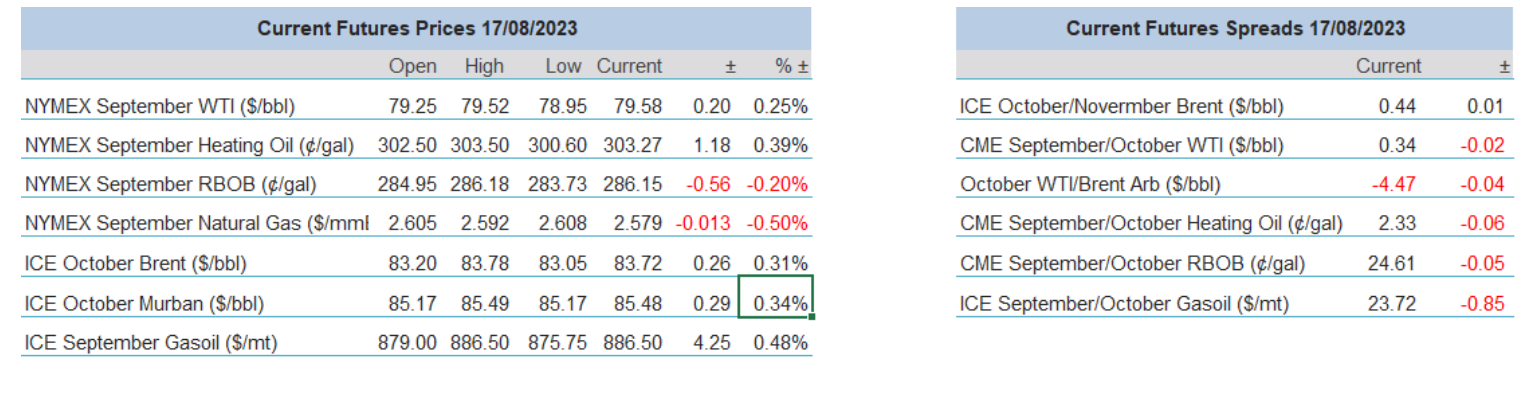

Yesterday’s US Inventory Report saw overall draws; Crude -5.96 million barrels, Gasoline -0.262 million barrels and storage at Cushing Oklahoma -0.8 million barrels. Although there was a small build in Distillate of 0.296 million barrels, total commercial stocks were down 7.398 million barrels. Last week, there were reports of US refiners choosing to up throughput even in dangerously hot weather, this is now confirmed as runs show utilization at 94.7%, up 0.9% on the week and 1% higher than the 4-week average. If the market had received these data in friendlier macro-economic climes, and even though not overtly bullish, the narrative of a tightening market would be at the top of news screens rather than today’s blight of financial considerations. Bulls will be hoping that this is only a hiccup, that the micro story within oil we be able to come back to the fore and that with the next Federal Reserve decision still some way off on 19-20 September, the all-powerful American consumer will still be in a confident disposition.

GMT +1 |

Country |

Today’s Data |

Forecast |

13.30 |

US |

Continuing Jobless Claims |

1.7m |

13.30 |

US |

Initial Jobless Claims |

240k |

15.00 |

US |

CB Leading Index MoM (July) |

-0.4% |

US spending its way into trouble

The US economy continues to astound the financial markets and confound the Federal Reserve as it remains resilient in the face of a long period of climbing interest rates. Despite a cacophony of global warnings of downturn in centres of trade such as China and Europe, Americans continue to spend in seeming gay abandon. Supported by a feeling of security derived from an absence of recession and a labour market that does not appear in any mood to cool, July sees very decent spending which can only come from confidence.

The advance US Retail Sales Report showed an increase in spending by 0.7% against a forecasted 0.4%. This is the fourth consecutive increase in a row and marks a yearly period in which there have only been 4 negative readings. There have been 11 hikes to interest rates in the US since March 2022, therefore the maintaining of appetite from US consumers is all the more impressive. Interestingly, the confidence shown is such that credit card spending has increased and despite higher interest rates, indebtedness has risen. Card credit rose by 4% and for the first time in history balances topped $1 trillion, according to the New York Federal Reserve.

This optimism and appetite for credit risk is expressed in the latest Consumer Confidence Index (CCI) which stands at 117, with 100 being neutral, and is the highest reading for 2-years. The July reading in US CPI was 3.2% up from 3% in June. Retail sales in June were 0.3%, therefore the pace of spending outpaced inflation and must be troubling for the FED that has insisted policy decisions will be fluid and based around contemporary data.

The US Retail Sales number is important for the road on which oil travels at present. Gasoline sales rose 0.4% in July, reaching $3.76 a gallon at the end of the month compared with $3.54 at the beginning, according to energy-data provider OPIS, and have risen further in August. The Gasoline sales data runs slightly in counter to the implied demand shown in yesterday’s US Inventory Report. At 8.851 million barrels, demand showed a reduction of 451,000 barrels on the week and while that may look alarming against pre-pandemic levels of 9.3 million barrels, it is still nonetheless in sight of the 4-week average that sits just under 9 million barrels and in line with the EIA’s long-term gasoline demand outlook that forecasts post-pandemic call on the motor fuel to remain intact at these levels until the end of 2024. Given Americans love affair with cars and their continued capacity to spend, predicting when a gasoline price slump will happen is dependent on how long the forthcoming refinery turnarounds last and when Americans run out of spending ammunition, or are forced to.

Gasoline is such an emotive subject in the US. Arguably elections can be lost or won on verbose campaigning accusing oil companies or OPEC of price gouging and international interference to name a few. However, high retail sales and high gasoline prices will come under the gaze of the Federal Reserve well before the politicians put their bunting up and kiss babies. There are hawks aplenty within the FED; San Francisco President Mary Daly in a recent Yahoo interview reinforced that there is more work to do, ‘the FED is fully committed to resolutely bringing inflation back to its 2% target’. Retail sales, helped by the solid labour market proves that the American economy has tolerance to higher interest rates. Retail appetite, pushing on gasoline prices will see the likes of Daly, judging by yesterday’s FOMC minutes, influence another rate hike which will be crushing for all markets. Our dance between macro-economic considerations and oil demand is set to continue

Overnight Pricing

17 Aug 2023