Geneva, The Centre of Diplomacy

It is greatly disturbing that warmongers find it tempting, and even necessary, to flex their muscles while negotiations over conflicts in which they are involved are ongoing. Russia regularly intensifies its attacks on Ukrainian targets, including civilians, whenever seemingly moribund peace talks get underway. Yesterday, as representatives of Iran and the US attempted to reconcile their differences in Geneva with Oman acting as mediator, the Persian Gulf OPEC nation deemed it timely to partially shut the crucial shipping artery, the Strait of Hormuz, for a few hours due to “security precautions.” It is truly questionable whether its intention to avoid direct US military action is genuine, just as Russian peace efforts do not appear sincere either.

The good news is that oil traders placed much more weight on the words of the Iranian Foreign Minister, who sounded obligatorily buoyant when he announced an understanding with the US on the main “guiding principles.” These two words were sufficient to send oil more than $1/bbl lower. However, none of you is fooled: tensions continue to brew and boil.

Prior to the indirect Iranian–US nuclear dialogue, Ukrainian–Russian efforts to inch closer to some kind of truce in the picturesque Swiss city did not disappoint, largely because expectations were low, and the issue of ceding Ukrainian land to Russia remains unresolved. As is customary, Russia launched overnight attacks on its neighbour’s power networks, and Ukraine responded with assaults on a Russian port, a chemical plant, and a refinery. If you characterise both talks to restore normalcy as stand-offs, then it becomes blatantly obvious why oil prices are unable to break out of the current $65–$72/bbl Brent range.

The Pot Calling the Kettle Black

The unorthodox economic policies of the incumbent US administration have, to put it mildly, both raised eyebrows and received plaudits domestically as well as globally. Whichever side one is on, it is reasonable to observe that, in its effort to make the country great and prioritise its interests above all else, the US does not shy away from using unconventional tools to achieve its ultimate objectives, be it exploitation, threats or confrontation. The one word missing from its vocabulary — no, it is not “tariff” — is “co-operation”.

Belligerent rhetoric and action inevitably lead to acrimonious relationships with trading partners, among which China is the most significant as far as the global economy is concerned. It was less than a year ago that the outraged bull, the US President, started to run amok in the China shop, leading to a war of words when the world’s two largest economies threatened one another with punitive duties of well over 100%. Think what you may of the often-outlandish economic policies of Donald Trump, but this particular coin, the US–China relationship, also has two sides, and China, not in rhetoric but in substance, has certainly been proving a worthy foe to the US.

China’s economic potential, given the sheer size of its territory and population, was always discernible. The real boon arrived at the dawn of the new millennium when the country was invited to join the World Trade Organisation. The combined value of its goods and services rose from $1.3 trillion to $18 trillion over the following 20 years. It became a global manufacturing hub; its growth was led by exports, foreign direct investment grew exponentially, and the country underwent rapid industrialisation and urbanisation.

Brighter economic prospects led to the pursuit of expansion beyond China’s borders, the most striking example of which is the Belt and Road Initiative (BRI), launched by Xi Jinping in 2013 to develop new trade routes. China’s growing influence in the developing world, coupled with its rising wealth, naturally resulted in trade frictions with other nations, and trading partners increasingly became competitors in the battle for global economic dominance. Accusations of intellectual property theft, industrial subsidies and forced technology transfer eventually culminated in a tariff war launched by the first Trump administration in 2018. Trade tensions are mitigated now and again, see the 2020 Phase One deal, only to flare up once more. And given China’s ongoing trade practices, they are unlikely to subside for good, as international trade rules can only be adhered to but not effectively enforced.

The trade and economic conflict between China and the US, and other economies, namely the EU, escalated further after the devastation of COVID-19, from which the Chinese economy emerged seriously wounded and seemingly unable to recover fully. The property crisis and the sharp shift in consumer behaviour towards saving rather than spending have considerably impeded domestic aggregate demand growth, and attempts to boost consumption, support the service sector or regulate key industries have so far proven ineffectual. Chinese deflation cannot be tamed.

Naturally, what is not consumed domestically will ultimately find its way abroad, leading to trade frictions and even anti-dumping investigations. Although the temperature of US–China trade tensions has cooled somewhat since last year’s reciprocal tariff threats, partly because both countries wield considerable leverage over the other (China commands a vast supply of critical minerals, while the US remains a technological pacesetter), the former has proved nifty in finding alternative markets for its goods. This is profoundly reflected in the country’s record $1.2 trillion trade surplus at the end of last year, even as its shipments to the US reportedly fell by 20% in 2025 and by 30% last December.

There is no need for a calculator to conclude that a ballooning Chinese trade surplus can severely hamper the growth potential of recipient economies; consequently, frictions are unlikely to evaporate. The US justifiably receives its fair share of criticism for its coercive and myopic trade policies; however, it takes two, or, on the global economic stage, three or more, to tango. As the rules-based global order increasingly appears a thing of the past and unlikely to return any time soon, intransigence rather than co-operation is set to dominate trade relationships, with repercussions for economic growth and, ultimately, the oil balance. Welcome to the era of spheres of influence.

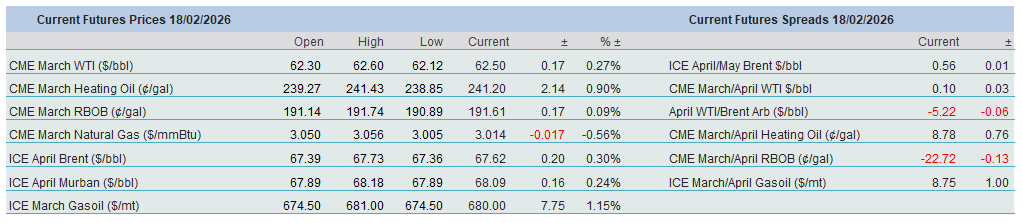

Overnight Pricing

18 Feb 2026