Gulf Oil Output, Refining and Transport at Standstill, Oil is Above $100

What a week it was, and what a week it will be. Researchers and analysts have been vague in predicting the next steps or outcomes of the Iranian conflict, which erupted a little over a week ago. The situation changes so rapidly that by the time the ‘send’ button is pressed, the content will already have become obsolete. Financial investors and oil traders do not have such qualms; they cannot afford the luxury of being slow to act. They voted, and will continue to vote, with their dollars. Last week’s performance conspicuously displayed the elevated level of anxiety about real and potential supply shortages.

Curiously, the updated reports from the CFTC and ICE show a paltry $5 billion increase in money managers' assets under management across the five major futures and options contracts. In fact, Brent, Heating Oil, and Gasoil all experienced a reduction in their net exposure. The latest reporting period ended on Tuesday, March 3, but the week-on-week price jumps would have warranted a significant increase in NSL across every contract. Given the relentless ascent throughout the week, no doubt the change in investors’ sentiment will be on display in the next set of data.

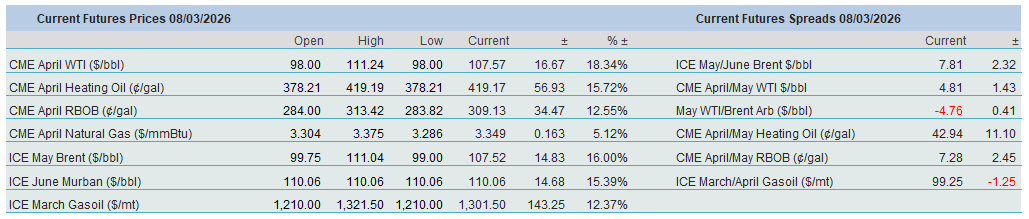

The growing anxiety about the geopolitical risk premium turning into an actual supply-shortage premium is unmistakable in the gains the contracts made over the calendar week. The winner was the ICE Gasoil contract, with a weekly return of 54%, followed by CME Heating Oil, which rallied 40%, despite its lacklustre performance on Friday. WTI managed to jump 36%, Brent 27%, and RBOB 21%. As a result, distillate crack spreads received a decent boost, and the structure of the main crude oil futures contracts strengthened considerably. The M1/M7 WTI backwardation widened by $17/bbl throughout the week, and the same spread in Brent climbed by $15/bbl.

It is well worth pointing out that WTI weakened relative to Brent in the first half of the week but strengthened later. Its discount narrowed by $2.75/bbl, from $7.94/bbl on Wednesday to $5.19/bbl by the close of business on Friday. This might seem a perplexing move, since the Iranian crisis has a much more tangible impact on European and Asian crude oil prices; however, it just shows that the situation is so desperate that Asian refineries are now trying to source barrels from the other side of the Atlantic as well.

Headlines and news kept traders occupied throughout the week and will do the same in the foreseeable future. After it became apparent that the Strait of Hormuz was effectively shut, 20 mbpd of crude oil and products became trapped, while shipping and insurance costs skyrocketed. As a consequence, Gulf producers were forced to fill up storage; Iraq had to scale production back by around 3 mbpd, and the rest of the region is following suit after the weekend’s developments. Alternative routes that circumvent the pivotal chokepoint in the Gulf, such as the Saudi and UAE pipelines, can only make up for a tiny portion of the stranded barrels. The Qatari energy minister warned of an oil price of $150/bbl, as regional producers are unable to pump.

Asia, the traditional buyer of Middle Eastern crude oil, bears the brunt of the Iranian crisis. According to Energy Intelligence (EI), China, India, Japan, and South Korea collectively demand 14 mbpd of Middle Eastern crude, the lion’s share of which arrives through Hormuz. Well, it is not arriving these days; therefore, EI estimates that regional refineries are being forced to contemplate the painful move of cutting runs, perhaps by as much as 30% of their nameplate capacity. It is no surprise, then, that China has already suspended diesel and gasoline exports, and Platts reported a Dubai cash premium of nearly $20/bbl on Thursday and rising. Competition for available barrels is intensifying. Two Reliance cargoes carrying diesel and jet fuel abruptly changed course and are now headed to Asia, not Europe.

The US and Israeli strikes on Iran continued throughout the week, killing the country’s supreme leader and several other high-ranking officials. Iran, in response, flooded Israel, Bahrain, Kuwait, and Saudi Arabia, among others, with missiles and drones. The US President poured cold water on hopes of de-escalation on Friday by firmly stating that only unconditional surrender is acceptable to the US, raising fears of a prolonged conflict.

The ante was upped over the weekend. The Iranian President’s apology to its neighbours for recent strikes against them appears to be empty words, as Bahrain, Kuwait, Saudi Arabia, and the UAE all said they intercepted Iranian attacks, with Saudi Arabia claiming that its Shaybah and Berri fields have come under fire. In return, fuel depots in Tehran and Karaj were hit, and reports are circulating that the US might have the critical Kharg Island—responsible for almost all Iranian oil exports—in its crosshairs. On Sunday night, Iran named the son of its former supreme leader as successor, while the US President refused to rule out sending ground troops to Iran.

How far the possible oil shortage will expand is not clear at this stage, but this week will see the release of updated monthly reports on the global oil balance. Most probably, the impact of the Iran conflict on DoC supply will be acknowledged, but its extent remains equivocal. In February, all forecasters anticipated rising inventories in the second quarter to varying degrees. The predicted surplus will likely be reduced by a great margin or, in the case of OPEC, might even turn into a deficit.

Although belligerent rhetoric and military action remain perfectly aligned, there have been attempts to mitigate the catastrophic impact of the conflict. China has started direct negotiations with Iran to allow ships carrying Chinese oil through the Strait. The US Treasury granted a 30-day waiver to India to buy sanctioned Russian oil. The US Development Finance Corporation is reportedly working on launching an insurance scheme worth $20 billion to help shipping traffic move through the Strait again. Simultaneously, Donald Trump floated the idea of the US Navy escorting tankers through the narrow passageway. By US law, the Navy can only escort US-flagged ships, but most likely, this would not be an impediment to executing the President’s order.

These US initiatives might be taken as an implicit admission of miscalculating the impact of the war against Iran on oil prices, as what started as a tripartite hostility quickly turned into a regional affair. Notwithstanding these efforts, the market is unmoved, as mirrored in last week’s price movements and in the continuing overnight rally.

It is almost trivial that elevated oil prices are causing growing concern among equity investors. Global stocks fell 3.72%, and the S&P 500 index shed 2% of its value—not exactly a bloodbath, but more of a warning sign of the adverse economic effects of galloping oil prices (with US retail gasoline prices now around $3.5/gallon). US stock futures, nonetheless, opened sharply lower on Sunday night. JP Morgan estimates that a rise of 10% in the price of oil would raise US inflation by 0.1% and cut GDP growth by 0.2%.

With the US labour market weakening and concerns about energy and food inflationary pressures rising, it was somewhat puzzling to hear the announcement from the US Treasury Secretary that global US import tariffs, following the Supreme Court decision, would probably be lifted from 10% to 15% soon. If there is any conclusion to be drawn after the first week of the most consequential war in the Middle East in decades, it is that the longer the conflict drags on, the more dire the political and economic repercussions will be—both globally and for the US itself.

Overnight Pricing

09 Mar 2026