Having a Much Better Hand, the US President Plays Trumps

The breathless pace at which President Trump rolls out policy and the exorcising process of sharing whatever thought is on his mind, leaves the world and markets bamboozled. Yesterday’s late performance alongside Benjamin Netanyahu in which he speculated on a US taking over of the Gaza Strip, turning it into the Middles East’s Riviera and asking the likes of Jordan and Egypt to take displaced Palestinians, tops the board of impulsive delusion. Or, magnificent performance gamesmanship, depending on one’s point of view.

Earlier in the day, he had already shown intent on Middle East meddling with the ordering of maximum pressure on Iran to stop its nuclear aspirations. Oil participants are very aware that during Trump I, the President oversaw a restrictive campaign that led to Iran’s oil exports reduced to almost nothing. With sanctions on Russia still being worked through, the thought of another source of international supply being stymied, arrested the recent momentum lower in oil prices. The one-month moratorium on Mexican and Canadian tariffs and retaliatory actions from China have served to calm much of the ensuing rally with the oil fraternity awaiting the next deck of cards to be tossed into the air of the Oval Office and where they might land.

Data in the US yesterday saw JOLTs Job Openings and Factory Orders miss forecasts, and taking the route of bad news is good, stock markets returned to their default mode and reclaimed some of the recent lost ground. The tit-for-tat Sino/US tariffs is being viewed by most commentators as limited giving more encouragement to stock market bulls. Yet, and as touched on below, the feelgood buyers are really only Americans for the state of economies elsewhere are troublesome. Australian Manufacturing PMI slumped again, although slightly balanced by a better Services reading. However, the miss in China Caixin Services PMI once again highlights an unbalanced world in which tariffs are most, most unwelcome.

It may not feel appropriate to consider, but we need the US

Canada and Mexico flinch, China gets ready to play tariff cards at the Trump table and Europeans hunker down, hoping Mr Trump does not turn his tariff-play gaze upon them. It does conjure an image of the inhabitants of Tolkien’s Middle Earth and how they try to avoid the gaze of the ‘Great Eye’. Whatever one may think of President Trump he does make for good theatre, with all possible respect to the citizens of Canada, Mexico and China who have skin in this current game. But what of the folk who ticked the ballot boxes enabling the return of such a global political hand grenade? Life appears on the face of it to go on unencumbered, economic exceptionalism may not be aimed at or felt by US citizens, but the investment suites certainly are judging by the reaction in US stock markets. While having checked back, stock prices continue to view dips as opportunities rather than warnings. The DOW still tracks along at 44,000, the S&P at 6,000 and the Nasdaq at 21,000 with all in striking distance of their all-time highs.

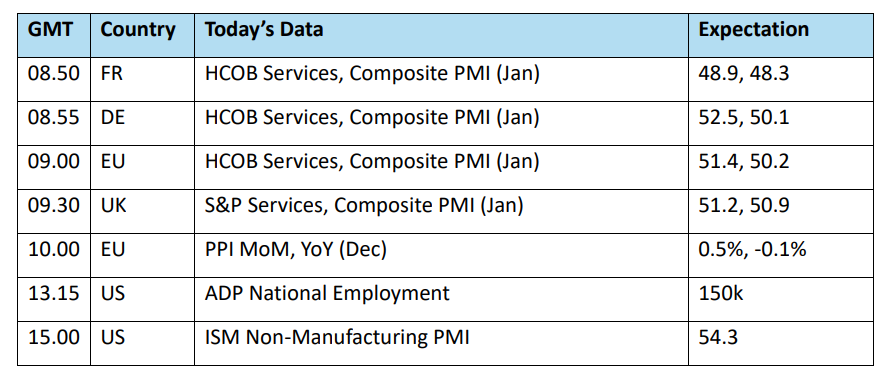

Over-optimism maybe playing its part, the great AI hope has not disappeared even after the hand-wringing sessions post DeepSeek. The other thought pervading markets at present is that tariffs are transactional, they are a hooking method to bring, in the US’s eyes, unbalanced trade partners to negotiation. Given the concessional backing down of Mexico and Canada and China arming itself with ‘measured trade responses’ such attitude does indeed have legs. Adding to the current market propensity to dismiss trading restrictions until they are made solid, is the strong performance of the services sector. It does not have a tangible physical product that might be subject to trade scrutiny and is judged in the main on internal performance. US January Services PMI in fact fell to 52.8, but according to S&P Global, new hiring surged and jobs in the sector rose to the highest level in 30 months. The ISM equivalent is due out later today, but in its December evaluation; Business Activity, New Orders and Deliveries Supplied all expanded and with both PMI’s averaging well over 50, and expansion, for 2024. Markets are concluding that tariffs, in their current fleeting guise, will have limited effect on non-manufacturing.

There is not exactly bad news from US manufacturers either. The ISM said its manufacturing PMI increased to 50.9 last month, the highest reading since September 2022, from 49.2 in December. It was the first time since October 2022 that the PMI rose above the 50-mark, indicating growth in the manufacturing sector, and according to Reuters, accounts for 10.3% of the economy. This expansion is despite stubborn interest rates and the growing belief that the FED will be very cautious in cutting this year. For exporters, the US Dollar is a problem, but growth was seen in textiles, metals and transportation among others and using Reuters again, factory employment expanded for the first time since May 2024. Of course, such increases might be in anticipation of tariffs and front-loading, but expansion appetite is not sullied or cowed as it is in other commercial centres around the world.

The US Conference Board (CB) Consumer Confidence Index, saw a downturn in January to 104.1 from 109.5 in December. Short-term expectations for income, business and jobs fell but remained above the point in which recession might be indicated. While not being explicitly named, the vaunted strategy of tariffs may have dulled enthusiasm, but the CB chief economist pointed out that the index remained stable, has been since 2022 and consumers still planned to spend money on big-ticket items, appliances, electronics and holidays but a reduced rate. Confidence in investment appears sound, Dana M. Peterson went on to say, “over half of consumers (52.9%) expected stock prices to increase over the year ahead, compared to just 23.7% who expected stock prices to decline.”

It is a strange a paradoxical situation. The very nation that could be the cause of global trade strife, is the same nation that abounds with confidence, hope, investment opportunity and the economic power to counteract the funk felt across nearly all other global trading centres. Calendar 2024 was an extraordinary and indeed exceptional year for the United States. The world can ill-afford a reversal in Uncle Sam’s fortunes in 2025.

Overnight Pricing

05 Feb 2025