Heads are Spinning, Eyes are Rolling

From taking over Iran’s oil industry to a handshake — all within the space of four hours. It is the contemporary standard in diplomacy. Threaten to hit your enemy "VERY HARD," then embrace them. Whatever the outcome, claim victory. Call off the strike and announce a deal with Iran that has been approved by "all parties."

Yet the announcement, which sent oil down $4 in an hour, came in typical Trumpian fashion. "Discussions and final points have been, in both concept and great detail, approved by all parties involved, including the United States, Israel, Saudi Arabia, UAE, Qatar, Turkey, Pakistan, Kuwait, Jordan, Egypt, and others."

Where is Iran on the list? The sceptic asks.

The Strait, President Trump claims, will reopen upon signing, which could happen on Saturday or Monday. Iran will not have a nuclear weapon, the thickest red line throughout the negotiations. Several other questions require exhaustive answers, including whether the deal is the extension of the expired ceasefire or a permanent peace agreement.

And the most important one: with the agreement ostensibly approved, would you go home long, short, or square the book ahead of the weekend?

Oil Prices Do Not Listen to Oil Inventories

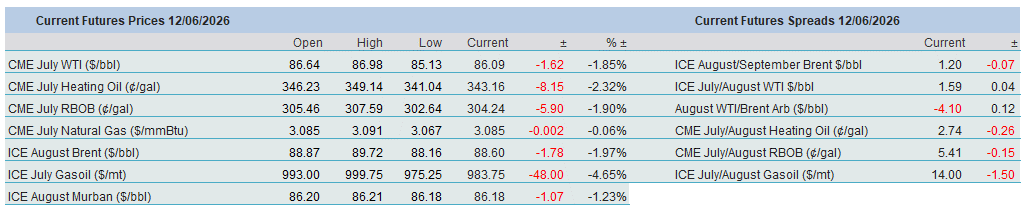

Looking at last night’s developments with healthy optimism, but with reasonable doubt, it is worth taking a look at the recent disconnect between oil inventories and prices. There is no denying that oil prices remain high by pre-crisis standards. They have a tangible impact on economic data, chief among them inflation. In the US, consumer prices, including food and energy, rose by 4.2% in May compared with the same period a year earlier, the largest increase since 2023. On the other hand, the seemingly unstoppable retreat since mid-May has pushed the price of the European crude benchmark down by a perplexing $23/bbl, or 20%, even as tensions in the Persian Gulf have not eased.

It is both possible and necessary to identify the factors behind this downward move while keeping in mind that, in peacetime, the Strait of Hormuz allows around 20 mbpd of crude oil and petroleum products to transit. Alternative routes, such as Saudi Arabia's East-West Pipeline and the UAE pipeline running from Habshan to Fujairah, mitigate the disruption to the extent of 4–6 mbpd. Waivers on Russian and Iranian oil already afloat may account for an additional 100,000 bpd. Recent estimates suggest that around 2 mbpd of oil is currently exiting through this critical chokepoint, although, given the volatile situation, that figure is probably changing by the day. Releases from strategic stockpiles, coordinated by the IEA, have also added supply. Assuming that the confirmed release amounts to roughly 200 million barrels out of the planned 400 million barrels, this translates into approximately 2 mbpd.

Then there is demand. It is impossible to determine precisely the extent of demand destruction caused by elevated oil prices and galloping inflation, but several countries have introduced measures such as homeworking, increased use of public transport, financial relief for households, and the promotion of renewable energy. The 29% plunge in Chinese crude oil imports in May reduced the country's demand for foreign oil from 11.9 mbpd in February to 7.8 mbpd last month. Between February and June, the EIA downgraded its global oil demand estimates for the second through fourth quarters of this year by 2.39 mbpd. Looking at the broader picture, the collective changes in supply and demand add up to somewhere between 13 and 15 mbpd, perhaps even more if the opaque volumes transported by the so-called dark fleet are included, compared with the roughly 20 mbpd that passed through the Strait before the crisis.

Finally, and perhaps most importantly, the consistently muted market reaction to fresh developments in this seemingly perpetual conflict also reflects how financial investors currently view various asset classes. As my colleague aptly described, "rotation" plays a pivotal role in oil price formation. Simply put, a bullish fundamental backdrop does not necessarily imply that prices will surge, as higher profit potential elsewhere, in this case, AI-related equities, can significantly reduce financial demand for oil. Recall the sharp decline in trading volumes from March to June, as noted in yesterday's report. Although tensions remain elevated in the Middle East, equities are perceived to offer more attractive returns than oil, or so the prevailing narrative suggests.

The combination of the market's remarkable ability to adapt to supply constraints and the financial community's shift toward technology stocks and IPOs has left oil prices unable to recover. Yet one must not lose sight of the hard numbers underpinning the global and regional oil balance. Returning once again to the latest EIA monthly report, global oil inventories are currently projected to decline by 5.31 mbpd between the second and fourth quarters of this year. OECD commercial inventories are expected to fall to 2.359 billion barrels by the end of the third quarter and to 2.269 billion barrels three months later. They ended 2025 at 2.816 billion barrels.

In the US, commercial oil inventories have declined for nine consecutive weeks. They currently stand at 1.21 billion barrels, 2.5% below the comparable level in 2025. As the US has become an important release valve for global market tightness, net crude oil and petroleum product exports are hovering around 5 mbpd. While this is 1.5 mbpd below the April peak, it remains well above the 2025 average of 3.24 mbpd. The retreat should not come as a complete surprise, given the rapid depletion of both commercial and strategic inventories; after all, ensuring domestic supply takes precedence. If the US decides to scale back further its role as the world's swing exporter, what will happen to European and Far Eastern product inventories, which are already worryingly below both year-ago levels and long-term seasonal averages?

One of the cornerstones of chart analysis is the notion that history repeats itself. In the geopolitical arena of 2026, however, it does not. It does not even rhyme. If it did, oil prices would have been significantly higher. Yet we must remind ourselves, and our readers, that the oil balance remains in a sizeable deficit. Global oil inventories will most likely continue to be drawn down in the immediate future, regardless of a deal or no-deal between Iran and the US. Should oil stocks remain suppressed, today’s AI story could give way to an oil fable once again.

Overnight Pricing

12 Jun 2026