High Correlation between Truth and Oil Prices

It sounds surreal. A one-page document outlining a 30-day truce, following a war that has cost the US $25 billion in military spending alone, has pushed oil prices down by $18/bbl in the space of three trading sessions. Investors and traders, justifiably or not, believe that some kind of ceasefire, during which the Strait would reopen and blockades would be lifted, is imminent; hence the sharp sell-off in oil.

Whilst such a move would undeniably be a welcome development, stark reminders arrived from both sides yesterday afternoon. An Iranian official, quoted by Reuters, said the Strait would remain shut under “an unrealistic plan” and that reparations to Iran would be a precondition for any deal. Almost simultaneously, the Wall Street Journal reported that Saudi Arabia and Kuwait had lifted curbs on US military access to their bases and airspace — an ominous sign that does not point towards a moratorium, armistice, or peace. Naturally, oil has recovered most of the day’s losses, although it still finished the day in the red. Overnight, the adversaries exchanged fire in the Strait, accusing each other of starting the hostility.

As liberating as it would be to cite refinery outages, changes in demand patterns, weather-related disruptions, climate change, manufacturing activity, trade deals, or job data as the major driving forces behind different asset classes, it seems that the Iranian saga will remain with us for the foreseeable future.

Falling Prices, Falling Stocks

It is irrelevant whether the oil price weakness of the last few days and the ostensibly insatiable appetite for equities over the last one and a half months are viewed with a jaundiced eye or an “I-told-you-so” attitude. Clearly, the long-term adverse impact of the Iranian crisis has been discounted, and there is a discernible consensus that the damage it has caused, and will continue to cause, can be contained. As Churchill observed, war does not determine who is right, only who is left. Perceptions and fictions are powerful drivers of sentiment, and the current narrative is undeniably buoyant about bringing the conflict to a reassuring end. To set the market mood against the realities of oil fundamentals, in other words, in an attempt to establish the physical backdrop, it is probably useful to round up the current state of global oil inventories, albeit without concluding.

As touched upon recently, and using monthly EIA data, global and OECD commercial stock levels have been revised downward. The global 2Q and 3Q stock builds of 3.03 mbpd and 2.68 mbpd projected in February have been turned into a stock draw of 5.09 mbpd and a modest build of just 290,000 bpd, respectively, and might be revised even lower when the updated findings are released next Tuesday. OECD industrial stocks are predicted to stand at 2.711 billion bbls in 2Q (versus 3.02 billion bbls three months ago) and 2.704 billion bbls in 3Q (against 3.069 billion bbls). These are substantial adjustments.

Investment bank Goldman Sachs sees global oil inventories reaching their lowest level in eight years shortly. Although the influential researcher does not expect inventories to decline to minimum operational levels this summer, it finds it concerning that they may fall from 101 days of demand to 98 days by the end of this month. It estimates that refined product stockpiles have plummeted from 50 days of demand pre-conflict to 45 days.

This prognosis chimes with that of S&P Energy, which reckons that crude oil stockpiles fell at a rate of 6.6 mbpd in April, faster than the 5 mbpd decline in demand. The combined loss now amounts to 1 billion bbls, the researcher estimates. According to S&P Global Energy, global oil reserves stand at around 4 billion bbls, but a significant portion cannot be utilised because of operational constraints, such as the need to keep pipelines pressurised and refineries running.

The regional outlook is equally troubling. Combined US crude oil and commercial product inventories fell by nearly 3%, to 1.241 billion bbls, in only six weeks. Although crude oil stocks are holding up comparatively well, distillate and gasoline inventories are both considerably below year-ago levels and long-term seasonal averages and have shrunk by around 15% since the end of February. The reason is prosaic: US refined product exports are accelerating as competition from Europe and Asia for available barrels intensifies. The latest weekly EIA report suggests that net US product exports jumped to 6.481 mbpd, the highest level on record. Morgan Stanley anticipates US gasoline inventories falling to record lows during the peak of the upcoming driving season, as refiners prioritise diesel and jet fuel production while gasoline imports have almost completely dried up.

In the Singapore hub, as reported by Enterprise Singapore, product inventories have plunged by 14% since the end of March, a particularly severe decline in light distillate stocks (-20%). Some comfort, nonetheless, can be drawn from the fact that combined product inventories, at 44.8 million bbls, are in line with the five-year average. Somewhat closer to home, in the UAE’s Fujairah Oil Industry Zone, total product inventories, comprising Light and Middle Distillates together with Residual Fuels, finished last week at 6.5 million bbls, the lowest level ever recorded and some 73% below the corresponding week in 2025, Reuters calculates. There is no denying that the situation is dire in Asia, as reflected in the region’s falling product exports. Combined diesel, jet fuel and gasoline exports were 3 mbpd below the pre-conflict three-month average, according to Kpler data. In the Amsterdam-Rotterdam-Antwerp region, total product stocks have recorded their fifth consecutive drawdown, leaving them 24% below end-February and May 2025 levels and 20% below the seasonal norm, PJK/Insight Global estimates.

The Strait of Hormuz might remain closed, which would exacerbate anxiety over product stocks. Or it might reopen soon. Yet if that happens without the removal of the Iranian regime or without a long-term nuclear deal, whatever peace is achieved will remain fragile. Ships may be eager to leave the Strait, but incoming traffic could stay well below average. Who would risk getting stranded again for weeks or months? Even in the event of a historic US-Iran rapprochement, which would amount to the greatest and most beautiful embrace the world has ever seen, it would still take months to restart production, refining and exports. And the conclusion? We will not draw one. Instead, we will watch how headlines and social media posts shape sentiment — sometimes in disbelief, occasionally with satisfaction, but certainly not in awe.

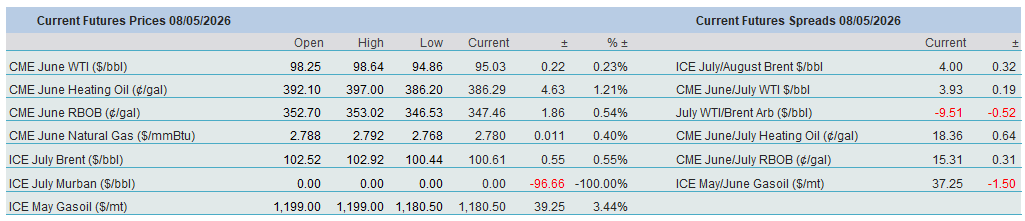

Overnight Pricing

08 May 2026