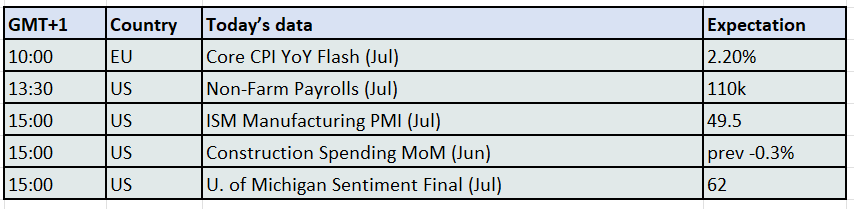

Honestly, Who Knows?

After once again blowout results, not even the amazing sight of Microsoft joining Nvidia as a $4 trillion valued company and Apple joining Google as $2 trillion one can inspire the three houses of bourse power, the Dow, S&P and Nasdaq (or as some say, the three horses of the Apocalypse) to march on again to all-time highs. Meta, Microsoft, and Alphabet have spent $186 billion on capital expenditures over the past year, which amounts to nearly all the revenue of the S&P 500 companies. In another time, in another week such mana for tech-stock bulls would see sympathetic buying across all classes, but not this jam-packed sennight. Spirits have been dampened, and it is not just that the US PCE price index inflation rose by 0.3 percent month-on-month in June, the largest increase for four months, with May’s reading being revised up 0.2%. The Fed Chair’s reticence to blink when under pressure to cut rates is proving prescient and with PCE being the favoured measure for price increases, interest rate adjustment just took a back seat and allowing the US Dollar to flex its muscles and yields to adjust higher accordingly. Yet, and still, these are not the cold waters which quell stock market fervour, it is tariffs.

The August 1st deadline is upon us and while there are levies that match expectations, such as India’s 25 percent, Switzerland’s 39 percent, Taiwan’s 20 percent and 10 percent on Brazil, there is so much more in the usual style of ambiguity. Mexico has been given another ninety-day stay of hand, whereas Canada’s tariff has been increased to 35% from 25%, but not to include goods covered by USMCA free trade agreement. In a barrage of words, from a barrage of White House spokespersons the antipathy of BRICS was mentioned, as was Russia’s oil relationship with India and that negotiations with China were moving forward, all made more confusing on the President having not decided to sign the ninety-day extension thrashed out in Stockholm. Pharmaceutical names took a stock market turn for the worse as Trump wrote to seventeen of them urging them to take action to lower prices or the Administration will deploy a tool to protect US citizens within sixty days. This then is the current tariff version, who knows how many Roman numerals will eventually be affixed, it is apparently to be signed by August 7th and until then all participants in all investment and trading derivatives are rightly thanking God it is Friday.

A Copper-bottomed lesson

Do we live in a Trumpian dystopia, a Trumpian empire or Trumpian boom? Only our descendants will be able to answer this. For the moment, it is all the world can do to keep up with the pace of geopolitical and geoeconomic current affairs. This was always going to be a busy week, the data docket foregrounded it, but add in the tariff, sanctions and war considerations, there has thus been a deluge of global drivers. They are not just economic, they are political; blurred lines have become open doors, and we should not be surprised given the world is now ruled by an entrepreneur. This is all rather obvious, cliched and said before, even on these pages, but nonetheless made contemporary by each day of renewed flux. It is maddening for those of us trying to compose a legible narrative, there is always something to miss, some utterance or piece of data making thoughts obsolete. More importantly, for our readers who take decisions of risk, second guessing becomes third and fourth, and unlearning positional habits is a must to survive.

Arguably, for there are many, one of the favourite picks of the week to example a need to be vigilant were the comings and goings seen in the Copper market on Wednesday. Comex M1 Copper Futures printed a high of $5.6280/lb on Wednesday and fell to around $4.4900/lb at the opening on Thursday morning and constitutes a 19% collapse in a single trading session. Did the US suddenly find the largest global Copper deposits in one of those far-flung States whose borders make up the patchwork of the American atlas? Or had AI achieved something useful for a change and enabled extraction by recycling of industrial waste and the millions of rotting car carcasses? Indeed not. It takes no Hercule Poirot, the imagined detective of Agatha Christie, to source cause for the violent price behaviour, for it is indeed one Donald J. Before a cabinet meeting on 8th July, he said, “today we’re doing copper,” proposing a 50% tariff rate for imports. It led to a stilted arbitrage market where the premium of US copper to comparable London Metal Exchange (LME) contracts soared to an all-time 30%, which duly evaporated. It really turned out to be a classic reaction to prohibitive legislation. If the only source of a good is a domestic one, then its price can only go one way. The pinched screams of domestic end-users from Silicon Valley to any number of companies involved in conducting electricity from one place to another finally met with reaction from the White House. Wednesday then saw the US President give exemption to refined metals, which is all but saying there is no tariff, and traders and those that had scrambled to secure enough supply before the August 1st deadline proceeded to abandon their longs.

Why this brush-up on ‘poor man’s gold?’ Well, Copper should always be tracked because it has a longstanding relationship with oil prices, not just for demand indications, but its similarity in processing and universal use, not forgetting the energy required to produce it. But that is not the point. It is how tariffs are put in place and removed with no thoughts of consequence. Whatever has befallen Copper this week most definitely has the political ability to migrate into our market. The oil fraternity would do well in keeping this lesson of trusting to the tariff or sanction words. Jeopardy lies in wait for those that are taking more than a short-term view on how secondary tariffs will be applied if Russia does not acquiesce in sitting down at a negotiating table to discuss a Ukraine ceasefire. Double jeopardy comes from a situation when after the ten days limit, levies are in fact announced only to be rescinded at a later date. Time limits are for quiz shows, supermarket sell-by-dates and sports games. They mean zero to the author of the tariff tribulation and from now on in, and using the Copper example, we should give them similar respect.

Overnight Pricing

01 Aug 2025