If it looks like a fudge, smells like a fudge, tastes like a fudge….

Then it is probably a fudge. The manner in which the OPEC/OPEC+ powers that be vacated the airwaves without so much as dropped comment, let alone a press conference, speaks volumes in terms of members not airing their dirty laundry in public. There is success in that, for the ‘sources’ undertaking backdoor hints to journalists dried up and what from the outside looks ostensibly a failure to secure consensus, is covered up with a confusing silence. But frankly, that is the best of it, for the rest is vague.

Giving autonomy in the guise of self-governance never works, institutions from banks, police forces, religious bodies and sports associations have all fallen short in history and so is it likely to be in this case of self-monitoring or if one wants to be cynical, a cheats charter. The Russian stance is perplexing to say the least, announcing yesterday that it will embark on an extra 200kbpd cut that will come from various grades of fuels including products, runs contrary to its recent lifting of all restrictions on refined product exports. It does appear that the much publicised African issue remains, for it seems that Angola have dismissed any notions of cutting production out of hand. The UAE has been harbouring greater quota desires for some time now, there is no point in having all its increased capacity at vast cost only to let it lie fallow at the altar of production unity. And what of Iraq? Given the right piece of signed paper from Turkey, 450kbpd of KRG crude will be making its way to Ceyhan rather quickly.

The flippant tone deployed here is reflective of how the market views OPEC+ decision, or non-decision, for the claim that actions have been taken in the name of stability turns out to be the very antithesis of it and one only has to regard how price has greeted this awkward meeting by threatening the emotional level of $80/barrel in Brent. However, that is not the worst of it. It may be a misreading, but the next OPEC meeting is not until June 2024, with Saudi’s voluntary cut ending in the first quarter. This chimes with those promising to embark on a program of voluntary cuts that will be reassessed in Q1 if the market allows adjustment, leaving an idea that for 3-months the market might just free-wheel. The whole of the oil fraternity will take some time to digest all of this, the near future for price discovery has just been made so very much more difficult. There is probably enough in these cuts to stop a full-blown meltdown of price but it will not stop a billowing cloud of confusion that is going to take the oil market weeks and months to figure out and only if the self-reporting data is indeed reliable.

09.00 | FR, DE, EUR | HCOB Manufacturing PMI (Nov) Final | 42.6, 42.3, 43.8 |

09.30 | UK | S&P/ CIPS Manufacturing PMI (Nov) Final | 46.7 |

15.00 | US | ISM Manufacturing PMI (Nov) | 47.6 |

It is not supply we should be worried about

For calendar year 2023, the EIA has global demand at 101.04 million bpd, the IEA 101.95 million bpd and OPEC 102.11 million bpd and unsurprisingly this pattern in estimation continues into 2024 with the EIA predicting oil need at 102.44, the IEA 102.88 and OPEC 104.35 with the average of their calls being 101.70mbpd for 2023 and 103.22mbpd for 2024. Again, and with little shock, the call on OPEC supply for 2023/2024 in mbpd are EIA 27.48/27.71, IEA 28.73/28.43 and OPEC 28.57/29.88, with agreement being achieved that non-OPEC supply will reach an average of 69.05mbpd for 2024 which is 1.23m higher than that of 2023. Contemplate all one might on demand figures and the differing calls on OPEC oil from the EIA, IEA and OPEC, the reality of nation growth when studied on an individual basis lays low any belief that industrial demand is just around the corner and with it an increased thirst for all that is oil.

It has been well documented on the progress of European economies and by progress one means abjectness, as data within in the last few days has not served to offer any hope of a change of fortunes in the foreseeable future. The National Institute of Statistics and Economic Studies (INSEE) published data showing the French economy reduced in the third quarter of this year by 0.1%, the GDP reading is a stark representation of slowing domestic demand including lower investments and importantly, consumer spending that dropped 0.9%, according to Bloomberg, against an expected decline of 0.2% with outgoings on food and importantly energy making headline reductions.

Since the turn of the century, Germany has seen an economic growth rate that has been the envy of its European peers, let alone other economies of the world. In the world of literature, a peripetia is a tragic turn of fortune, and such is the dramatic fall from grace of Germany’s powerhouse status, it is not hyperbole to apply it to the about-face in its economic performance. Aptly, through oil-centric eyes, the inflection point came after the Russian invasion of Ukraine leading ultimately to Germany’s loss of many forms of cheap energy that were supplied by Russia. Industrial business models, built around a concept of a future containing limitless cheap energy, now lie in tatters with once thriving businesses unable to afford the subsequent prices of alternatively supplied fuels. Out of the last 6 quarters, the economy has only grown in 2, 3Q/2023 GDP printed -0.1% from 2Q and according to ING research, on the year, Germany’s economy shrank by 0.4% and barely above the pre-pandemic level.

On the other side of the world, China, greater in degree but comparable in the story of success to Germany, struggles to hit its much-jawboned stimulus fire striker on the flint of economic activity, with just not enough spark to get the Asian trading behemoth moving. Yesterday, November National Bureau of Statistics (NBS) Manufacturing PMI came in at 49.5 and yet again in contraction. Not only was the figure -0.1 from the previous month, but China in 2023 has had 4 months of expansion with 2 just barely and the other 6 in contraction and arguably could have been worse if it were not for the stimulus and threat of stimulus that authorities laud from the rafters. The business consortium research publication, the Conference Board, observes that China, as of next year, is likely to enter a prolonged period of lower growth while dealing with structural imbalances and tension in geopolitical relationships.

Even the United States, that has been the bastion of hope for all investors and the driver of demand through personal behaviour is currently seeing somewhat of a slowdown in its oil needs as inventories begin to build. The main storage hub at Cushing, Oklahoma was recently charged with being in danger of bottoming, but since has seen consistent builds with at week-on-week increase of 1.854mb and a year-on-year increase of 3.407mb. With refined products having been such the focus of recent bullish rhetoric, it is interesting to see that implied demand this week for Gasoline decreased by 274kb and in Distillate by 1.096mb. Whether or not the high interest rate environment is starting to bite into the US consumers’ confidence that would affect oil needs, remains to be seen. The point of all this to-ing and fro-ing across a snapshot of the world’s economies is that we continue to believe that oil prices can only be truly represented on how much demand there is and not supply.

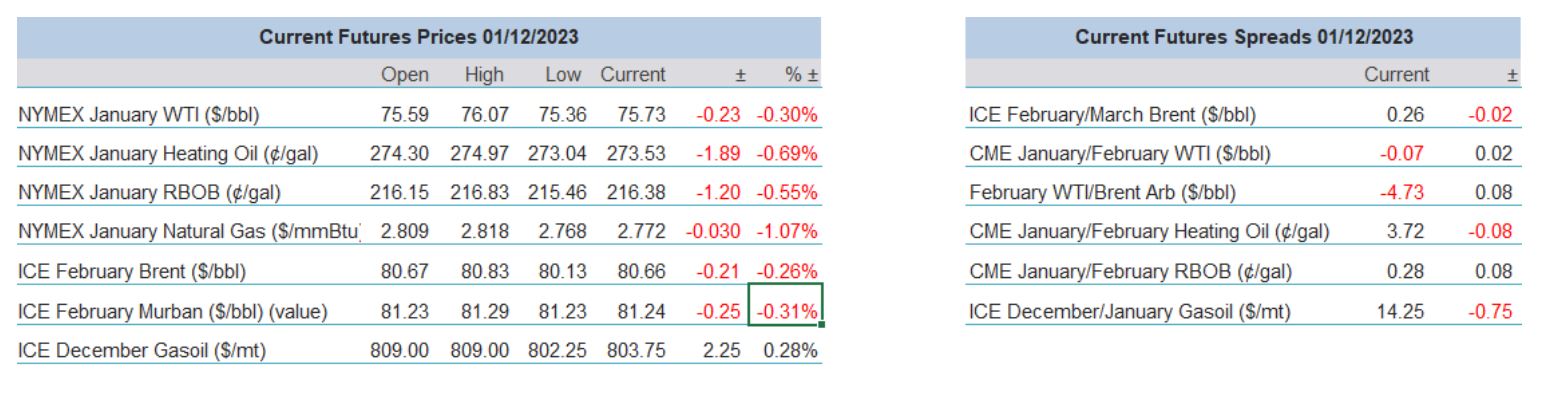

Overnight Pricing

01 Dec 2023