Incredible Nvidia, But Maybe Not Quite Enough

There was no heraldic stock market clash of a gong at the release of Nvidia’s first-quarter earnings forecast, rather a collective, almost audible sigh of relief. At any point during last year if the results seen post-close on Wall Street of the world’s most valuable company had matched these latest offerings, the rally across global bourses would have been extensive. As it is, record quarterly revenue of $68.1 billion, up 20 percent from the third quarter and up 73 percent from a year ago, along with record full-year revenue of $215.9 billion, up 65 percent, served to soothe furrowed brows, shift the tech darling’s share price higher by only 5 percent in the early hours which has since been almost all eroded by profit-taking. Its share price is a proxy for the health of A.I. demand and these stellar data indicate that such huge monies invested in tech companies can still be justified and returns gained. Whether this continues and the fears of the A.I. potential of the likes of Anthropic’s ‘Claude’ helper to outperform existing software platforms remains to be seen. Meanwhile, it is an interesting time in trading markets that are boxed in by the A.I. doubt, the incredible development in tariffs and of course the meeting in Geneva today which might just possibly give destiny to where the oil price will go from here.

Inflation is as oil does

We read with interest the handwringing going around the world when it comes to inflation. It may have only been a small upward miss in the CPI reading in Australia yesterday, the year-on-year January reading registered at 3.8 against predictions of 3.7 percent, but it very much outlined and confirmed why the Reserve Bank of Australia has been offering quite a hawkish stance and indeed was the only major central bank to have recently increased interest rates. Earlier in the month the main rate was increased by 25-basis points as the bank explained in its post-decision statement that a wide range of data over recent months have confirmed that inflationary pressures picked up materially in the second half of 2025 and the Monetary Policy Board considered inflation being likely to remain above target for some time.

A bit further north, the Corporate Service Price Index of Japan remained at a stubborn 2.6 percent. The gauge of service inflation is leaned upon to offer a read in company-to-company charges, employment costs and how they might be passed on to Japan’s consumers. The index, having dug in, will now add to the potential clash of wills between the government executive wishing to embark on another broad range of economic stimulus, and the Bank of Japan concerned with not allowing itself to become behind the curve in what can only be an inflationary reaction to Prime Minister Sanae Takaichi’s return to quantitative easing. If the Yen takes another bashing without being rescued by either intervention or a rise in interest rates, the import-inspired inflation will send foodstuffs and energy prices soaring.

While China is still smitten with disinflation and the European Union’s price rises well within the 2 percent target, as seen in yesterday’s posting of 1.7 percent, Uncle Sam’s outlook remains elevated. In a recent opinion piece, J.P. Morgan expects US inflation to stay in the realms of 3 percent. The falling US Dollar aids imports but because of tariffs, the additional costs of goods flowing into the US have been passed onto consumers. Last week’s CPI report was slightly softer than expected and excluding food and energy, the core CPI was up 2.5 percent, the lowest level since April 2021, with December PCE and its Core scoring 2.9 and 3.0 percent respectively.

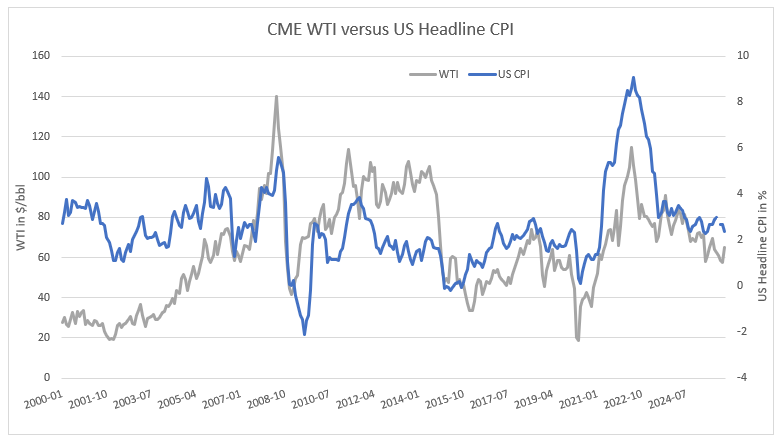

Therein lies the point, global inflation may be mixed but whatever anxieties keepers of economies might have, energy prices are not one of them. The recent spike in oil prices seen since the beginning of the year have failed to register on the radar of increased private and industrial expenditures. In fact, the sullen performances of all energy prices at the end of 2025 were deflationary and without the geopolitical fear of an Iranian conflict, backed up by association and not a game changer in Ukraine, would continue to be so. However, inflation is a self-fuelled rocket where oil is concerned. Heaven forbid a prolonged US/Iranian war where supply disruptions are more than just imagined. The price rises of industrial production, of energy generation, of transportation will see a shock in both CPI and PPI and according to the World Bank, oil price surprises have been the main drivers of variation in global inflation and last year supposed that a “positive oil price shock of around 10 percent, global inflation increases by 0.35 percentage point within a year, and 0.55 percentage point within three years.”

Self-fulfilling indeed. Oil and energy are often regarded as a reliable hedge against rising inflation and within CPI make ups, account for up to 20 percent of consideration. Therefore, if CPI rises significantly, oil has little option other than to follow even if at the start of a price rise cycle it was the major cause. Goldman Sachs took this argument up last year in an insight observing, “historically, energy generated the strongest real returns across assets when inflation surprised to the upside. That’s because energy usually responded both to supply and demand shocks.” The talks in Geneva today become even more important from a global perspective, other than any of us wanting to be shadowed by a big mushroom-shaped cloud, because a sustained run in higher oil prices and inflation will not go unnoticed by institutional investors and while oil has not been part of any commodity cycle of late, it might just create its own.

Overnight Pricing

26 Feb 2026