Inflation is a Fact, not a Possibility

Markets could barely give any attention to the Federal Open Market Committee and its decision, unsurprisingly, to keep interest rates on hold. Frankly, if it were not for how the United States puts its clocks forward before the rest of the world, it might not have received much attention at all. Such was the bagatelle-like spinning and pinging of oil price numbers. The 11 against 1 vote, Stephen Miran (a Trumper) obviously wanted a cut, noted that inflation remains elevated and trending way above the 2 percent target. Not that the higher than forecast PPI posting by the US Labour Department would have had any effect, but it justifies the FOMC’s decision to be vigilant. What is intriguing and a knife to those who hope for an easing in the Fed’s attitude, is how the Core PPI, which is assessed without the biggest of data movers of food, energy and trade services rose 0.5 percent month-on-month and 3.9 percent year-on-year. If price rises are seen in data classes not affected by energy, then there is little wonder that the CME FedWatch tool is pricing at least a 70 percent change of no change of rates until December, and even then, it is 58 percent. We will look at the ‘Jones Act’ at a later date, but the relaxing of its shipping rules where foreign shipping cannot move goods domestically does not ostensibly affect global oil prices, it aims at keeping bottleneck inflation occurring in a variety of goods including being mindful of States that rely on sea-delivered fuels such as Florida. The US Federal Reserve is preparing for inflation; the US Government is preparing for inflation and energy prices will certainly oblige.

One step back; two, three, four steps forward

One would need be a muddle expert to wander through pressing urgency in each new development in our oil world. We all love an expert. ‘X’ being the unknown quantity, and ‘spurt’ a pressurised drip. How apposite when talking about oil, and the newfound importance of Hormuz which is spoken on by so many people as if they went to bed for the last ten years worrying about the shipping which traversed the strait. Most people we know thought Hormuz was something served in an South-Asian restaurant, but maybe our cutlery has too much of a cynical edge. Still, the price of oil is nothing new to the social consciousness and every part of global current affairs which might intrude in the passage of energy prices is debated from boardroom to household kitchen tables.

We witness how tightly oil prices are strung in the reaction yesterday morning on the news that, at last, the Kurdish Regional Government and Baghdad have agreed a deal which allows exports to once again flow into the world’s seaways via the Ceyhan pipeline. How an initial 100kbpd of new supply makes any difference in the world losing 8mbpd, is emotionally rather than mathematically relevant, but such is the importance attached to anything that shows movement of oil supplies. According to Reuters, Kurdish tensions with Baghdad were heightened after the federal government implemented an electronic customs system to monitor flows, allowing for easier assessment of imports and revenue which the KRG described as a threat to its autonomy. One can only assume that the current massive prices being paid for Middle Eastern crude grades is the inspiration of this bout of accord rather than some diplomatic breakthrough, because the pie to share suddenly just became markedly larger. We await with interest if such reasonableness abides if crude prices were to miraculously fall back toward $60/barrel.

However, old foes to lower prices seem never far away. Libya's National Oil Corporation reported yesterday that a fire had interrupted flows on a pipeline that serviced the Sharara oilfield, and while supplies were being directed through alternative means, that fact that the statement went on to say the diversion would "significantly reduce losses," it all but admits that supply is reduced. News from Libya is never straightforward or indeed readily shared, and how damaging or how long this issue might last is more than a counter to any extra flows emerging from Turkey. Additionally, the greatest saviour of oil prices last year, namely Chinese SPR builds, shows no sign of letting up and if anything, the concept of energy security is prioritised in the minds of the powers that be because not only does China sponge any Asian grade or Russian crude it can get its hands on, it is now operating under a regime of zero exports for refined products which is accelerating gasoline, diesel and jet fuel prices in the Asia supply theatre and will eventually knock on globally. There are no other countries with the refining capability of China, it is described by notable shipping and oil supply agencies as the ‘swing supplier’ of refined fuels, therefore, if it carries on excusing itself from market contribution in fuels the effect is likely to be profound.

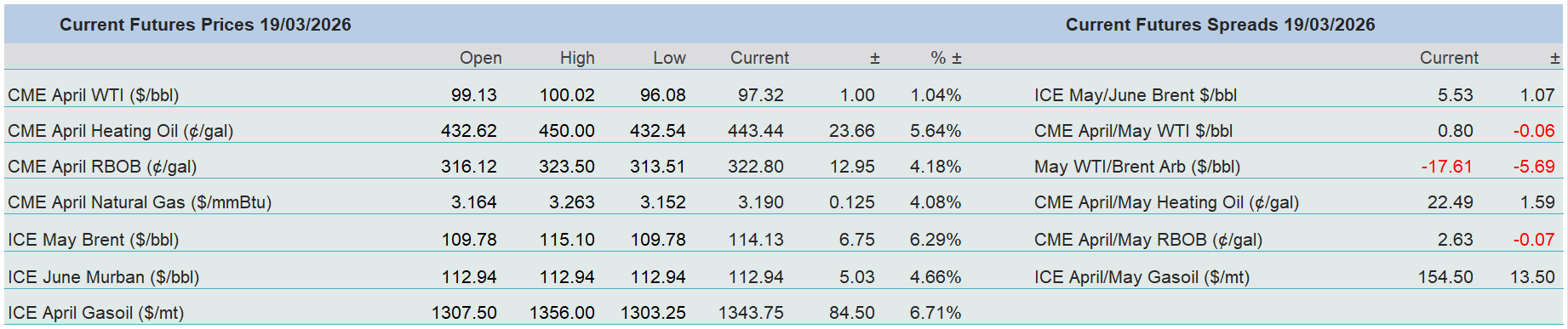

The process of equalisation of bullish and bearishness stories becomes moot in the face of the arbiter of all our anxiety, this new Gulf war. Whatever containment the market feels the war might restrict itself to was breached by Israel’s attack yesterday morning on the Iranian South Pars gas field. Iran mouthed retaliation and then proceeded to attack the Ras Laffan Industrial City in Qatar which is responsible for 20 percent of global gas processing. Tehran also targeted other sensitive areas in the UAE and Saudi, and by doing so has sent alarm through not just energy markets but the White House, which this morning denied prior knowledge of the South Pars attack and stated that no further strikes would be made. However, de-escalation is nowhere in sight, but what is for the Brent futures price, is the spike high of $119.50/barrel seen on the first realisation that Hormuz was closed.

The point is that as much as the market scavenges for bearish supply stories, there are always new or old points of demand, or pinches in supply to call or even raise the ante. Would that we could sashay away from being caught in the spin of Hormuz. But this dance to the sound of American, Israeli and Iranian warfare will continue to gather pace as other bullish drivers reveal themselves and will only stop when the orchestral sound of explosions completely stops, and even then, only after the encore of repairing oil communications to its previous state.

Overnight Pricing

19 Mar 2026