Interest Rates Will Not Leave Oil Alone

The oil market has at last experienced a seasonal demand indicator as seen in the Distillate draw in the US EIA Inventory Report. Stocks of the middle barrel product reduced by 3.2mb against a build expectation of 0.7mb. However, what brings seasonal cheer is at the current 4.5mbpd demand, it is the highest since early 2022. Although the Crude decrease in inventory of 0.934mb was lower than the expected 1.6mb draw and very much shy of the API 4.7mb decline, it still represented 4-straight weeks of reduction. There is little doubt that stockpiles in Crude are due to increasing exports, which according to the report stands at 4.89mbpd and is also cheering data for demand, yet oil prices failed to take advantage of the data with the day ending up being only marked with modest gains.

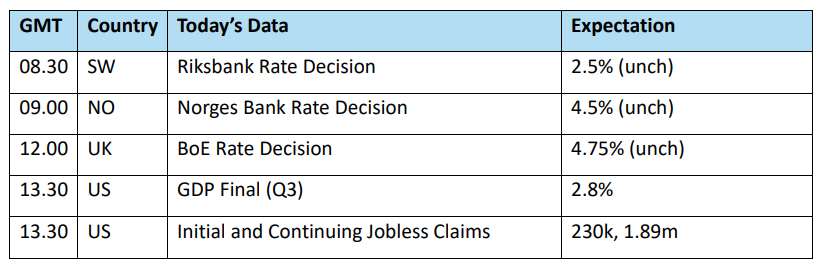

Once again, the macro suite ran as the great interferer as the FOMC decision, which came as no surprise at -0.25%, was accompanied with realised fear of a future conservative interest rate path. Inflation seemed to be in the mind of the FED Chair Jerome Powell as he warned, “we have been moving sideways on 12-month inflation." While he was not prepared to comment on what a Trump administration would mean for markets, the much vaunted 'dot plot' now only allows for 50-basis point cuts in 2025, which is half of market expectation, and the reason stock markets had a mini meltdown that infected all investment suites and sent the US Dollar Index (DXY) soaring to over 108.00. The fallout is not done with yet, and with the BoJ this morning leaving rates steady and BoE unlikely to cut, oil's induvial journey will be curtailed by greater and more weighty influences from the macro scene.

Sanctions keep oil bulls interested

As with most of the investment suite, the oil market is not being served well by the nearness of central bank decisions to the end of year proceedings. Commitment to moves either way is ephemeral, and prices draw themselves into another huddle. Ask any technical analyst and they will point to how all the moving averages are converging. Yet, for bulls it is encouraging that Brent has not lost its ‘$70’ handle despite all the gloom surrounding China’s future oil demand and the negative undertones involved in OPEC+’s delay of reintroducing thus far shuttered barrels.

One of the final acts of Joe Biden, a palatable one, is to introduce further sanctions on Russia. The restrictions are bundled in with efforts to disrupt the military relationship between Russia and North Korea. Moscow and Pyongyang have embarked on a relationship of convenience involving oil and arms and personnel exchanges and while that is important in geopolitical terms, the expanded tariffs on Russia are where the interest lies for the oil community. The current US administration is trying, in belated fashion, to aid Ukraine before the horse trading of war settlement might involve President Zelensky ceding land if Donald Trump fulfils his claim on solving the war in 24 hours. The US Treasury sanctions involve freezing certain entity assets, bar any access to the US financial system and block transactions which might involve US citizens.

The US sanctions come hotfoot on tightening of trade practices from the European Union. The EU has adopted its now fifteenth package of sanctions against Russia. Circumvention by Russia has been almost accepted by the market as it makes use of it shadow fleet and if anyone in the US or the EU were to put a hand up in acknowledgement, the truth is that Russian oil being able to get to water has been a contributing factor in the demise oil prices. Cast a cynical eye over these latest measures and one does wonder if Brent was printing something near $100/barrel would such fervour in concern for Ukraine be so verbose or sanctions be so punitive?

For in the EU package there is an aggressive change, it actually targets Russia’s customer base. As the European Commission describes it, “the EU has, for the first time, imposed ‘fully-fledged' sanctions (travel ban, asset freeze and prohibition to make economic resources available) on various Chinese actors.” The targeting of specific ship companies and individual vessels themselves by the US, EU and joined by the UK yesterday squeezes the availability of freight and therefore the cost for Russian exports that can still make sail. One of the biproducts of the sanctions is that older, less seaworthy and dangerous ships are hopefully taken from sea routes and environmental risks reduced. Something rather apposite bearing in mind the recent sinkings of barely-welded-together Russian tankers in the Black Sea.

Apart from actually boarding all suspicious ships at sea or other such direct action, relying on economic measures to counter military aggression remains questionable. Sanctions may have been made more effective, but they are somewhat telegraphed and hardly proactive. If Russia in recent history has deployed chess-like circumvention, it can do so again. Posterity will be the judge, but can Ukraine wait for history? Still, despite such cautionary ponderings they do not dispel that the net, be it a slowly moving one, is drawing in on Russia and its capability to produce petrodollars. The obvious consequence is that if Russia experiences tightness in ability to export, the oil market as a whole will enjoy less oil to keep prices bridled. Whether or not these new bouts of sanctions are effective remains to be seen, but they, with a market bought into the idea of a Trump administration going after Iran, means that oil is able to keep a bid into the New Year. Until of course the new US President is sworn in, when all bets are off.

Overnight Pricing

19 Dec 2024