Investors Become Defensive as the US Dollar soars

The forward outlook as seen from the US Federal Reserve is not done with influencing investors toward the year end. Fewer interest rate cuts from the US will not only reverberate now but echo all the way to the Presidential inauguration on January 25. The obvious beneficiary is the US currency with the Dollar Index (108.35) entertaining 2-year highs and making anything priced in the American marker more expensive against local currencies and so the wobble in oil prices. With China's PBoC keeping both the 1 and 5-year LPR interest rate markers unchanged, China offers little for oil protagonists other than to dwell on the disappointment of a year of failed stimulus promises and warnings of falling demand. Yesterday the latest one came from Sinopec saying that 2023 was the peak for Gasoline demand and predicted a similar Crude import high in 2025. Market participation is diminishing as investors dial back and caution is the word of the day, even Bitcoin crashes back through $100,000, with one last marker of the year to digest. The preferred inflation marker of the US Fed, the Core Personal Consumption Expenditure Price Index (PCE), may just find a market made sensitive due to the new 'dot plot' and anything above expectation will have an outsized effect on proceedings. Adding to concern, and in Europe a sense of foreboding, is that according to news sources, President-elect Trump has posted on Truth Social that the EU must address the deficit with the US "otherwise it is tariffs all the way!"

2025 will be all about the US, again

Yesterday we touched upon the bullish undertones the oil market was feeling going into the year end as the new bout of sanctions on Russian oil capabilities brings to mind greater effectiveness and therefore less oil on international waters. However, there is always a ‘but’, and this one comes in the form of the ever-present influence of the new US President as he approaches his Part II tenure in the White House. Donald Trump does bring some potentially glaringly opposing policies that may affect the fortunes of oil prices next year, with one of the obvious and probable immediate short-term being sanctions. Russia aside, the President-elect has publicly and privately expressed concerns about Iran achieving a breakthrough in developing nuclear weapons. Sanctions on Iran have not changed, they just have not been enforced and the politics of convenience are once again to blame. After the Russian invasion of Ukraine, and as Crude prices dallied with 3-digits, taking the then 1.1mbpd of Iran exports away from the oil supply puzzle would have had a disastrous upward effect. In current climes, and with the spare capacity of OPEC and increasing supply from the Americas, the sensitivity of blockading Iranian Crude is much reduced even though exports now stand at 1.7mbpd. Still, when coupled with similar restrictive practices on Russia, a bump in prices is all but assured but there is an added kicker. Mr Trump has refused to rule out the possibility of war with Iran and stories of how the US is weighing up strike options against Iran’s nuclear capability will only act as an accelerative to those who see a wider war developing in the Middle East.

Running counter to this and once again a measure of paradox that will be a contingency in any policy from the new administration, is an attitude that needs no explanation in “drill, baby drill.” The EIA expects US production to reach 13.5mbpd in 2025, up 300kbpd from 2024. Standing firmly behind oil producers will be one of US oil’s greatest fans, whipping production along at a galloping rate. Keeping a fire under drillers and frackers must be an imperative if the shear amount of US oil that hits international markets is maintained and thus nullifies any potential side effect of sanctions. Mr Trump has also expressed in loud terms that the security of the United States should never be comprised because it might run out of oil. Currently Strategic Petroleum Reserve (SPR) stands at 392mb. Back in August, and on the campaign trail, he bemoaned how SPR, at the time 375mb, stood at the “lowest number it has ever been,” and vowed to fill it to the capacity of 714mb. No doubt the rate of filling will be variable depending on the global situation. If tight, US production will go to water and the recent record of nearly 5mbpd will not be in isolation as it will be as a counteracting remedy to any possible shortfall caused by sanctions. If the global situation is sloppy, then US producers have a ready customer in SPR buying.

Mr Trump’s choosing of department heads see cheerleaders of fossil fuels and America’s oil industry. Chris Wright, the candidate for Secretary of Energy is a leading light in the fracking industry. He is a climate change sceptic who previously said he does not care where energy comes from, it needs to be cost effective, reliable and able to better lives and fossil fuels are needed to lift people from poverty around the world. Whatever pauses in licensing, investment in EVs and renewables there have been under the massively expensive Inflation Reduction Act (IRA), they are likely to be undone by Mr Wright. Another fossil fuel-phile is being nominated for the Secretary of Treasury. Scott Bessent, a fund manager by trade, counts oil as one of his future economic drivers. In a 3-3-3 plan, his proposal is to cut the budget deficit to 3% of GDP, boost GDP growth to 3% which will be aided by increasing US energy production by the equivalent of 3mbpd. Quantifying ‘equivalent’ is impossible without meat on the bone to his plan, but such aspiration might see US Crude production close to 16mbpd. It will be a hard sell to shareholders of the US oil sector who would rather be profitable than be the world’s swing producer. However, with such pro-oil governmental Secretaries willing to keep the US oil spigots fully open, the contrarian possible influence within a Trump administration will keep us fascinated all year. This past year, we have always believed the biggest event would be, was and is the US Presidential Election. In 2025, the product of that election will be the premier driver in all market considerations.

PVM Reports will return on Monday, 6th January. A Merry Christmas and Happy New year to all.

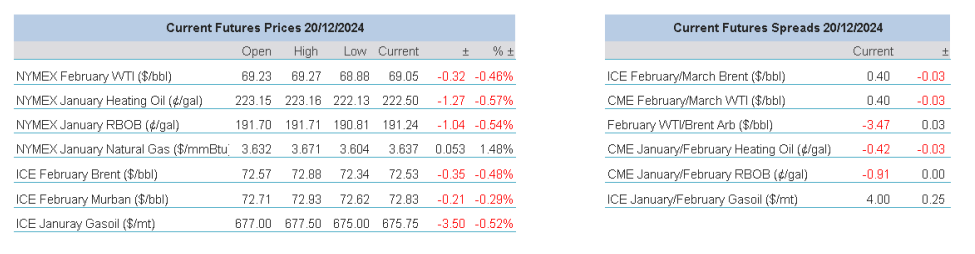

Overnight Pricing

20 Dec 2024