Invisible Strings

The move higher continued unabated yesterday and justifiably so. Or, if we could be slightly more nuanced, it looks as though some pre-EIA profit taking in crack spreads helped crude oil rally greatly aided by financial data whilst products failed to catch up. China’s pledge to help its struggling economy kicked off a buoyant day as investors are clearly unmoved by darkening clouds gathering above the country’s economy. Deteriorating German business morale was casually ignored, and attention turned to the update World Economic Outlook from the IMF. The multilateral lender sees resilient global economy and upgraded its 2023 forecast by 0.2% to 3% but warned of challenges ahead caused by aging population while also noting that scarce credit could lead to debt distress. Equities received further boost yesterday from the rise in US consumer confidence although the Conference Board was at pains to explain that the fears of recession have not subsided yet. The same rhetoric is heard from the Federal Reserve. Today’s rate hike, if it occurs, is widely anticipated to be the last one before a long pause, yet Fed officials will be very wary of raising false hopes of calling a day on the unprecedented monetary tightening programme. Data is constructive and strings that are attached to them are hiding in plain sight.

|

GMT +1 |

Country |

Today’s data |

Expectation |

|

15.00 |

US |

New Home Sales June |

725,000 |

|

15.30 |

US |

EIA Weekly Petroleum Status Report |

|

|

19.00 |

US |

Fed Interest Rate Decision |

5.5% |

|

19.30 |

US |

Fed Press Conference |

Bright prospects lie ahead

No doubt the second half of the year kicked off in a sanguine mood. After a three-month hiatus and following a complete lack of conviction during which oil was stuck in a narrow range there has been an upside break-out in July. After front-month Brent started to come off the April peak it moved in a range of a mere $7/bbl and yo-yoed between $71/bbl and $78/bbl until the end of June. Then a newly found optimism re-invigorated buyers and now challenging the high of $87.47/bbl in April and the 2023 peak of $89.09/bbl achieved in January cannot be ruled out.

The reason for this upbeat mood is well-publicized. The second half of the year was always believed to be tighter than the January-June period. This tightness is the result of a significant upgrade in demand estimates and the perseverance of the OPEC+ producer group to do a “whatever it takes” a la Mario Draghi and cut output until the market reacts. This month’s updated OPEC data sees global oil demand to be around 102.58 mbpd in 2H 23, a tad down from the June estimate but 1.16 mbpd higher than in 1H. Non-OPEC supply, on the other hand, is expected to decrease by 780,000 bpd during the same period effectively providing a massive boost to OPEC’s oil call. Demand for the organization’s oil is pencilled in at 30.40 mbpd for the latter part of this year, up nearly 2 mbpd on the first half. OPEC output in 1H will plausibly exceed that of in 2H. Global oil inventories should decline 1.95 mbpd compared to a build 120,000 bpd in 1H.

Accordingly, OECD oil inventories, which show a robust inverse correlation to prices, ought to deplete considerably. OPEC data suggests they rose from 2.761 billion bbls in 1Q to 2.815 billion bbls in 2Q and at the same time the European benchmark average price of $77.73/bbl in the April-June period was $4.37/bbl under the 1Q price. So, what to expect for the coming quarters? Assuming that around 40% of the global stock draw occurs in the developed part of the world, OECD stocks should fall to 2.741 billion bbls in the incumbent quarter and to 2.672 billion bbls towards the end of the year ostensibly meaning higher prices.

The latest available set of data from the research arm of the producer group implies thinner OECD oil inventories in 3Q and 4Q than estimated the month before. They should stand 2.741 billion bbls in 3Q and 2.672 billion bbls in 4Q, a monthly downgrade of over 20 million bbls. Accounting for seasonality, these predicted inventory levels then would correspond to an average Brent price of $98.60/bbl for July-September and $95.30/bbl for the last quarter of the year.

These estimates might turn out overly optimistic, nonetheless the direction is clear. Perceived tightness should keep prices resilient. What could throw a spanner in the works? On the supply side, there are no surprises anticipated from non-OPEC+. The producer alliance, on the other hand, might decide to increase output if prices remain stable. Whilst it is certainly a possibility not to be ruled out, the OPEC heavyweight, Saudi Arabia is desperate to support prices and will probably keep its voluntary reduction of 1 mbpd in place at least throughout September. Russian crude oil prices vary from $65/bbl (Urals FOB Novo Afra) to $84/bbl (KEBCO), according to S&P Global Commodity Insight. They are above the G7 price cap therefore every single barrel of Russian seaborne crude oil is now, in theory, at least, sold without Western ships and insurance possibly limiting the country’s ability to maintain healthy export levels.

On the demand side the question mark is China. The economic revival after the lifting of Covid restrictions has been a disappointment. Dismal sets of data (export, import, manufacturing, retail sales, the troubled property sector) is set against government efforts to shore up the ailing economy. The country’s oil demand for the second half of the year at 15.74 mbpd remains sturdy and is higher than projected six months ago. Continuously discouraging growth prospects could lead to a downward revision in demand, palpably souring the presently buoyant mood, but such concerns are seemingly swept under the carpet for now. In the present uncertain trading environment one must be intellectually flexible to amend his/her market view nimbly if needed but the latest snapshot suggests a jump to $90/bbl and maybe even briefly above that as the oil balance tightens meaningfully.

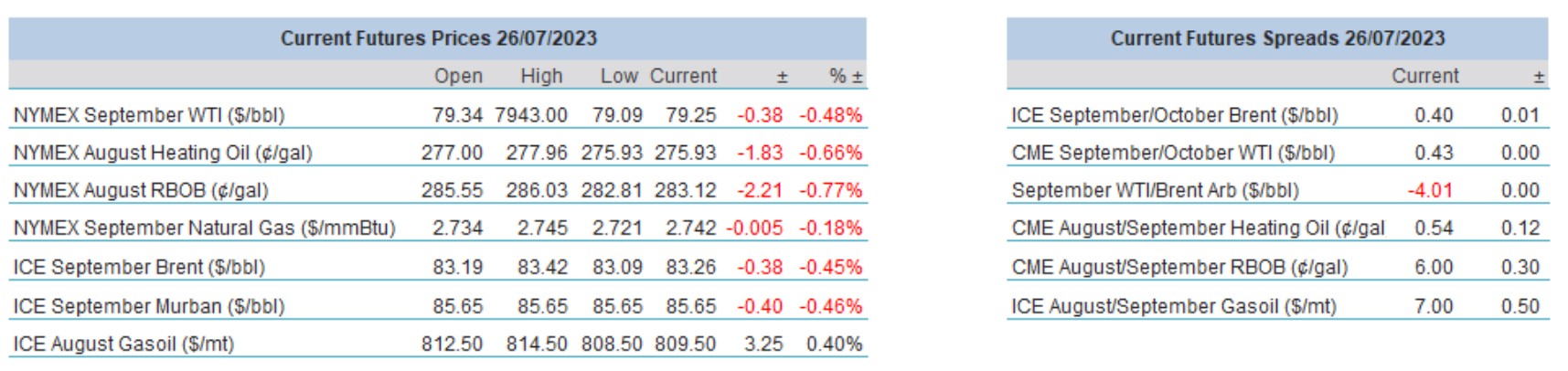

Overnight Pricing