It All Adds Up to Confusion as Sellers Remain Reluctant

If there is any consistency in the oil market, it is that every day our fraternity wakes up to yet another headline-competing and oppositional influence/s that just adds to the ball of confusion. The mini hiatus in poor relations between the US and Venezuela is seemingly over as the Caracas government seeks to uphold a ban on an opposition candidate to run for president bringing a swift response from Washington that if such a political omission occurs, then previous sanctions will be restored. The amount of Venezuelan crude making its way to the market has thus far been way below the potential of a future free from restrictions, but the South American country was brought back into the fold as an antidote to OPEC cuts, therefore the curbing of another potential source of supply runs with the current narrative of 'tightening'.

Running in somewhat counter to this, is the fresh ceasefire proposal brokered by Qatar between Israel and Hamas. As reported in the Guardian, Qatar’s prime minister, Sheikh Mohammed bin Abdulrahman Al Thani, said speaking after talks in Paris between officials from the US, Qatar, Egypt and Israel, “We are in a better place than we were a few weeks ago.” The deal involves a hostage exchange of 40 Israelis and 4000 Palestinians over a 6-week period according to the Jerusalem Post, and if that manages to manifest into a lengthy ceasefire then there will be a cooling of the source to the current Middle East strife.

Meanwhile, wider markets will have to contend with the many and varied headlines and pre-moves that accompany any US Federal Reserve rate decision which will be announced tomorrow. Pricing tools such as CME's FEDwatch and other sources are very much in agreement that there will be no change, but it will be all about the language deployed in the ensuing press conference. Even though US bourses continue to make record highs, the picture is nonetheless weaker elsewhere in global equities.

This is particularly true in China that has in recent days enjoyed some good news as the government and the PBoC try to render support from various sources including a $140-billion boost in liquidity for stock markets and a curbing of short-selling and stock lending. Unfortunately, this has all come undone after the announcement of a Hong Kong court that it is dissatisfied with Evergrande's restructure program, and ordered it to liquidate. There is such noise in the market that the enormity of this decision is somewhat overlooked, but with property giant's exposure estimated at well over $300 billion, the ramifications of a possible collapse in the China's property sector makes moot any authority stimulus and will have very negative global shockwaves. Investors continue to spin plates.

GMT | Country | Today’s Data | Expectation |

09.00 | DE | GDP Growth Rate Flash YoY, QoQ | -0.2%, -0.3% |

10.00 | EU | GDP Growth Rate Flash YoY, QoQ | 0%, -0.1% |

15.00 | US | CB Consumer Confidence | 115 |

15.00 | US | JOLTs Job Openings (Dec) | 8.75m |

Will Iran’s links with malcontents backfire?

It is a common thought, and one that we share here, that of all the biggest drivers that will bring stormy waters to the fate of economic progression and the price of oil this year will be the US Election. Therefore, the inauspicious attack on Tower 22 in Jordan, which is reported to be a logistics centre for the US military, and claimed in responsibility by the Islamic Resistance in Iraq which according to regional commentators is a beneficiary of Iranian support, not only brings abhorrence due to the lives lost but might have far-reaching effects on the US election that these satellite terrorists groups have not thought of and have probably not occurred to the idealogues of Iran itself.

No matter then that the Iran’s mission to the United Nations quickly absolved itself by offering that it had no connection to the attacks and blamed an ongoing conflict between resistance groups and US forces in the region, the current crop of movers and shakers that aim to shape the narrative within the United States are intent on blaming Iran. President Joe Biden’s currency on international affairs, particularly those that have a military edge, runs at a very low level and even though the US forces withdrawal from Afghanistan 3-years ago was penned and initiated under the previous administration, what is seen as capitulation and Vietnam-like embarrassment is rounded up and piled at the President’s door.

It is an open wound for the President and one that his predecessor, ex-President Trump (the author of the Afghan withdrawal) is more than willing to nag at and worsen by bringing charges of foreign policy ineptitude saying, “this brazen attack on the United States is yet another horrific and tragic consequence of Joe Biden's weakness and surrender." The Republicans, listed by Reuters, were in full battle cry with Mitch McConnell’s undisguised political poke, “we cannot afford to keep responding to this violent aggression with hesitation and half-measures”, and Michael McCaul, House foreign affairs chair scoring more points with "We need a major reset of our Middle East policy to protect our national security interests and restore deterrence." The sitting President could only muster how an account would be held at a time and manner of our choosing, which seemed to be the party stump as almost a verbatim repetition was heard from the US Defence Secretary Lloyd Austin, and in the face of such gung-ho language from those across the political aisle, sounded rather wet.

Petroleum Intelligence Weekly (PIW), informs that Iranian crude and condensate exports last year registered their highest level since Trump-era US sanctions came into force in 2019 with China the main destination of up to 90% of internationals shipments. At the end of November 2023, and according to Reuters, the Islamic Republic’s output was around 3.2mbpd, total exports being 1.4 mbpd for calendar 2023, Vortexa reports, and again the highest since 2018 before sanctions were initiated. This pattern of increased oil to water is also picked up by Kpler, via PIW, which not only aligns with analytics of Iranian exports being 1.3mbpd but showcases the increased freedom that Iran is enjoying having only exported 880,000bpd in calendar 2022.

There is little doubt that increased exports from Iran is a matter of convenience for the United States and its allies that are turning a blind eye to sanction evasion because of the many-edged effects of high oil prices including inflation, industrial activity and most importantly for politicians, the influence it has on voters particularly in an election year. However, when it comes to fatal attacks on US servicemen and women, explaining the intricacies of global oil trading are not needed for political gain against an incumbent President, just a verbose and insistent campaign on national interest weakness even when the commander-in-chief is striving for proportionate responses and a joined up foreign policy.

It may very well turn out that the militants and resistance groups reportedly funded by Iran, are doing great work for the Donald or any other now unlikely Republican substitute, by highlighting the holes or perceived and/or advertised holes that are appearing in President Biden’s resolve and his ability to sell his Middle East plan to not only Israel, Hamas but all other protagonists, will end up marching a hard-liner into the White House who will stop Iranian oil exports quicker than you can say ‘sanction’. National hardship will return to Iran, not that it has entirely left, and when it does the logic of financially arming the plethora of anti-American, anti-Israel, anti-West indignants will be rightfully questioned.

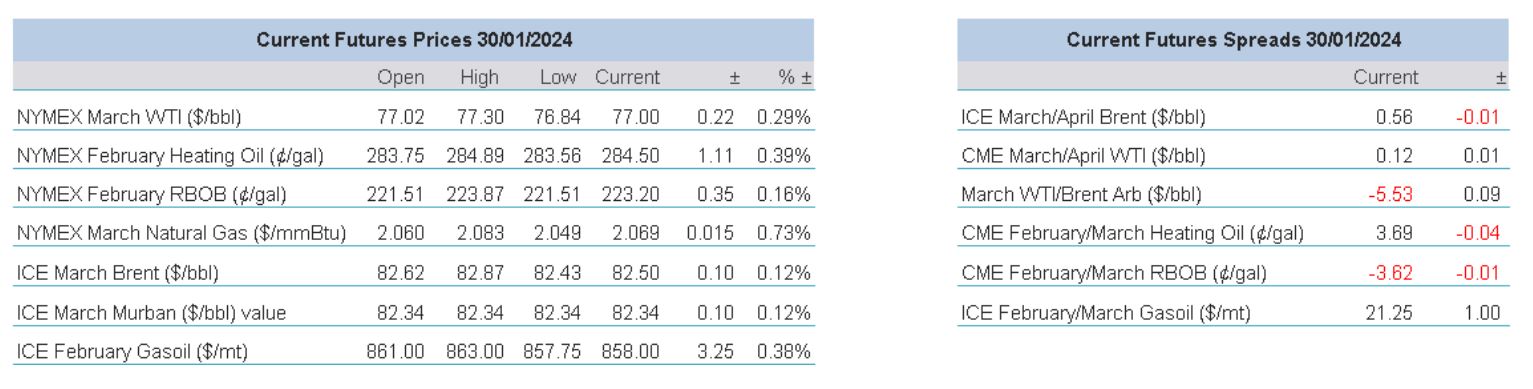

Overnight Pricing

© 2024 PVM Oil Associates Ltd

30 Jan 2024