Just Way Too Early to Call War’s End

The US brokered accord between Russia and Ukraine agreeing to a ceasefire on each other’s energy complexes and a truce to hostilities in the Black Sea might be viewed as progress from Washington but with language already being manipulated (by Russia in the main) hours after the announcement, one can only cast doubt on whether this is a turning point. The wrangle, and where it is-oil sensitive, is over Moscow’s statement that such a halt in hostilities would be linked to the lifting of some sanctions. Kyiv batted this away, countering that such a caveat was false and Russia was already distorting the agreement. Tenuous indeed, this morning sees reports of both protagonists exchanging drone attacks only hours after the supposed agreement.

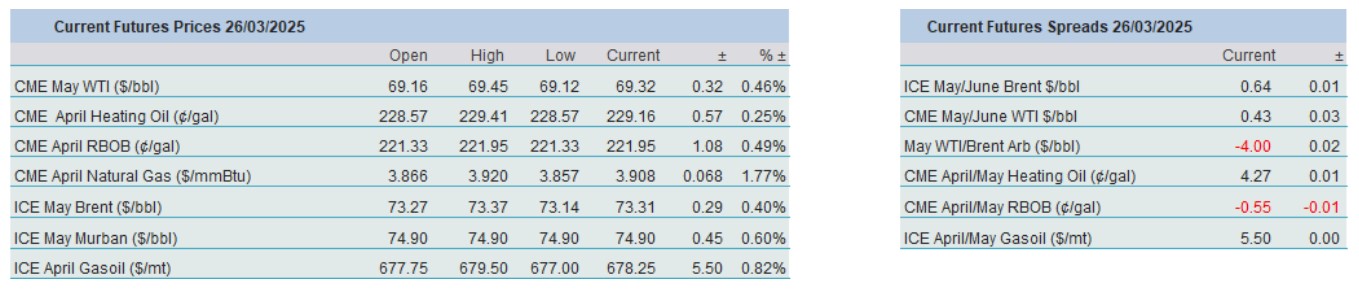

Still, the idea of sanction lifting will bring market considerations of more oil available in the world and maybe just tug on the reins of the current rally. Whether or not this is worthy depends on how Russia will adhere to its quota within OPEC+ and the expert way in which it has avoided sanctions and made its oil akin to an Amazon next day delivery. This is why the across the board draws seen in the API Inventory overnight have thus far had little effect. Crude stocks fell by 4.6mb, Gasoline by 3.3mb and Distillate by 1.3mb. Oil’s current bid is still underwritten by Washington’s sanction attack on customers of Venezuelan and Iranian oil giving rise to alternative grades being sought in the East. Dubai regains its premium over Brent as it did when Joe Biden initiated fresh Russian sanctions at the start of the year. While the arbitrage dynamics do not mathematically work at present, any more of a rally in Asian crude grades will see more bids into structure in the Brent marker and its servicing derivatives.

To flip or to flop, that is the question

Those that have been wishing, and maybe even praying for an end to the tarifflippery being exhibited in the White House should not pin hopes on this current false dawn of market relief. Although the S&P 500 arrested a one-month headlong fall last Friday, it does not suddenly signal an advent in return to stock market buying ways. Even if this week sees companies posting decent earnings, it does feel as if confidence is being clung to by nails only, but those cuticles are being nibbled at by the fear of whatever fallout comes from the reciprocal tariffs due to be implemented next week. The Trump administration is well aware of the state of the stock markets which is why appeasing notions of ‘targeted’ tariffs rather than blanket ones are uttered in public circles. But trust is wearing thin, and all markets need confidence for higher progress.

What is an illuminating indicator to the presence of mind on Main Street, USA was yesterday’s Conference Board Conference Board’s Consumer Confidence. Once again, and for the fourth-straight month the reading fell, this time to 92.9 against an expected 94.5, but what is significant is that the metric is at a 12-year low. The financial futures of Americans are riddled with anxiety and while many argue against emotional readings versus explicit numbers, a continuation in loss of faith will eventually lead to quantitative failings.

One thing the market is always fearful of and indeed will track to the point of boredom is the US PCE (Personal Consumption Expenditure) Index. It has been well established that in terms of monetary policy the US Federal Reserve much prefers to plot the fate of the PCE rather than CPI. Published monthly by the Bureau of Economic Analysis (BEA), the PCE gauge is an active tracker of how US homes are spending. Its make up is comprehensive and includes goods and services such as housing, food, fuel, health along with many others and are even scrutinised into subsets. This then gives dynamic data and a wider look into the behaviour of those that make the economy tick reflecting patterns of inflation. Therefore, this week of important US data will be rounded off by the PCE reading on Friday and investors will reprice the hopes of interest rate cuts accordingly.

Yet even this hallowed of economic indicators might just find its normal reach of influence impaired. The FED’s key borrowing rate range remains 4.25% to 4.5% after last week’s FOMC meeting and there was not much in there to believe its central bankers would play loose and fast with impossible-to-predict future economic outcomes. Post-decision last week Jerome Powell described uncertainty faced by rate setters as “unusually elevated”, sentiment was experiencing “turmoil” leaving the FED to deal with an “inertia” caused by a vacillating outlook. Indeed, the influential Atlanta Federal Reserve President Raphael Bostic on Monday anticipated slower progress on inflation. He adjusted his view on two-cuts in rates for 2025 to just one not only for the unreliable outlook, but how businesses are expected to add the cost of coming tariffs to their prices, leading him to predict that, "the appropriate path for policy is also going to be pushed back," in an interview on Bloomberg.

Trying to alleviate some of the worrying seen in the performance of markets and economic journals alike, any tariff-inspired inflation should be transitory so said the Fed Chair. However, markets have long memories and sprawled across many of Wall Street’s pamphlets are reminders of the last time ‘transitory’ was wheeled out by Jerome Powell. This was post-pandemic and his predictions for temporary price rises turned out to be wrong for 2 years. It is very possible that ‘higher for longer’ will once again be paraded by market observers and those that are in the business of interest rate divining. Embarking on predictions of a US stock market meltdown is inappropriate, but it does not preclude periods of investor confidence absenteeism and therefore slumps, one of which we are enjoying at present. Be they qualitative or quantitative, data sets will be outTrumped by tarifflipperry or tariffloppery and unease is now haute couture in global economies and those that invest in them.

Overnight Pricing

26 Mar 2025