Last Month

By any standard, the month of March was shocking, unprecedented, turbulent, vicious, and nightmarish—take your pick. The returns of the five major oil futures and options contracts were eye-watering. They are summarised in the table below, with rollovers arbitrarily taking place on the penultimate trading day of March.

Given the dramatic widening of backwardation across all contracts, returns on the structure have been even more astounding if one takes a tabloid view of March performance. The standout was WTI, which generated a return of over 3,000% as the May/June spread widened from 22 cents/bbl at the end of February to $6.86/bbl a month later.

The prospect of buoyant returns driven by Middle Eastern geopolitical upheaval, almost by definition, made money managers ravenous, as illustrated by the Commitment of Traders reports from both the CFTC and ICE throughout March 24, although, as was characteristic of the month, there were a few surprises.

Combined assets under management grew from $45 billion to $77 billion, an increase of 71%, broadly matching the average return of the oil complex. What is notable is that net speculative length (NSL) increased in WTI (+57%) and Brent (+27%) over the past four weeks but declined in products: -17% in Heating Oil, -19% in RBOB, and -22% in Gasoil. The share of the two crude oil futures contracts in the total rose from 62% to 70%, while that of products fell from 38% to 30%.

Meanwhile, crack spreads widened considerably. The CME 3-2-1 crack doubled in value, from $27.19/bbl to $55.87/bbl between February 24 and March 24. Over the same period, the ICE Gasoil/Brent differential widened from $27.37/bbl to $69.66/bbl.

This anomaly suggests heavy, and understandable, refinery buying of products to fulfil contractual obligations amid scarce crude availability and reduced runs, as reflected in the significant trimming of net short positions in the producer category. It is likely that, as persistent product shortages become more apparent in the coming weeks, money managers will follow suit, supporting crack spreads and allocating relatively more capital to products than to crude oil.

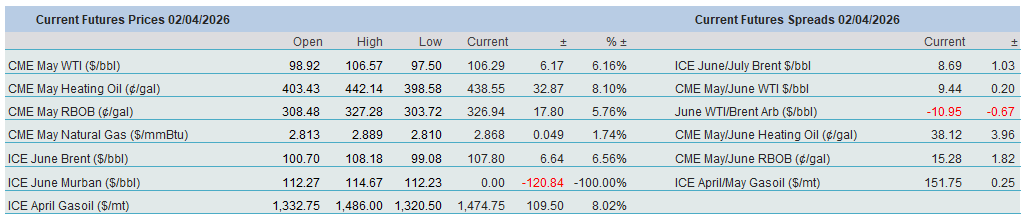

Yesterday

The first day of the new month and the new quarter was rich in narrative but scarce in progress. Contradictory statements characterised trading, and whether they were genuine or taken as April Fool’s jokes depends on one’s taste, beliefs, and possibly positioning. Given the general weakness in oil prices, it can be concluded that investors were giving yet another chance to the fast-diminishing credibility of the US President, who claimed that the end of the Iranian war is within spitting distance and that the outcome is exclusively under US control. In any case, these were the major news items yesterday:

• “The Strait of Hormuz will never open,” said the deputy speaker of the Iranian parliament.

• “Iran’s new regime president has asked for a ceasefire,” said President Trump.

• The claim that Iran has asked for a ceasefire is “false and baseless,” according to Iran’s foreign ministry.

• The Strait of Hormuz will remain closed to Iran’s enemies, according to the Islamic Revolutionary Guard Corps.

• The UK is to host a meeting of 35 countries on reopening the key oil shipping channel, according to the BBC.

• The US will leave Iran “pretty quickly” and return if needed, President Trump told Reuters.

• Israel continues to attack Iran and Lebanon. A Qatari oil tanker was struck by an Iranian missile. Iran also continues its attacks on Israel.

• Oil supply crunch will deteriorate further this month – IEA

Overnight

The US President addressed the nation after markets closed last night. As is customary, he delivered yet another reversal and threatened to hit Iran ‘extremely hard’ in the coming weeks. Hopes of a ceasefire and de-escalation, raised by the President just a few hours earlier, were quickly dashed. He warned US allies, if any remain, that they would have to take the initiative in reopening the pivotal Strait of Hormuz.

The renewed, though hardly surprising, sabre-rattling came amid falling domestic approval ratings and rising retail gasoline and diesel prices. Failing to reassure the US public and global investors that oil would soon flow through the Strait, oil prices rallied while equities plunged. Inflation fears remain elevated as the war of choice continues.

Overnight Pricing

02 Apr 2026