Less Crude More Sanctions

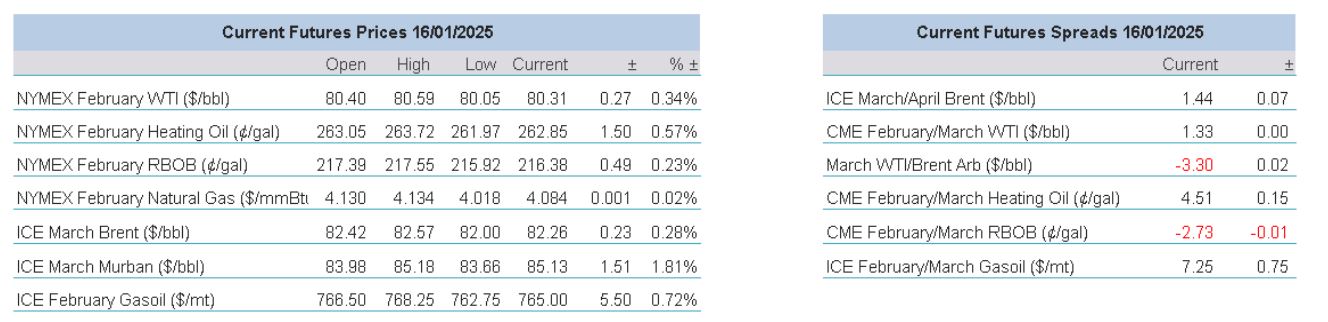

On the face of it, yesterday's US Inventory Report was something of a mixed bag as the build in Gasoline stocks of 5.8mb and 3mb in Distillate would ordinarily have compensated for the 1.96mb draw in Crude inventory. However, due to another anomaly where imports of Crude into the US fell by 1.3mb and exports increased by 1mb, holdings in the base oil show a little historical sparsity. The EIA reports outside of the SPR, Crude levels are at their lowest for nearly 3 years. Indeed, stockpiles are 17.23mb below that of last year and 24.54mb below the 5-year average. This brought a new bout of vim and vigour from bulls and the main M1 futures contracts finished higher with WTI +$2.54/bbl (3.28%), Brent +$2.11/bbl (2.64%), Heat +8.82c/gal (3.49%), RBOB +5.43c/gal (2.58%) and Gasoil +$18/Mt (2.43%). Yesterday's rally also came equipped with greater interest in Crude spreads with M1/M2 WTI and Brent finishing higher by 20c and 33c/bbl respectively as the fears of global tightness due to the new sanctions on Russia were quickly married to the diminished state of US Crude stores.

Yesterday, Joe Biden's outgoing administration imposed another fresh bout of sanctions, and although they are not oil specific, they are intended to tighten existing restrictions on already sanctioned entities making evasion and avoidance much trickier. Although there was a US CPI relief rally yesterday, inflation only quickened slightly, stock markets and other investment medium are caught up in results season, tit-for-tat tech trade restrictions and of course the swearing-in of the new US President on Monday. Therefore, oil has become something of a destination for investment tourists and the narrative at present offers friendly climes, of which the cold weather that is set to continue is a contributary. Not even a ceasefire in Gaza is enough to quell oil prices at present. Sadly, the importance of that centre of horror has become less and less and over the last year the oil market has learned to ignore what has been going on from a bull perspective, why should it be any different now from a bearish settlement one?

Hail to the chief

We could be accused here of being besotted by all that is Donald Trump, but is there a bigger ticket on the horizon that has as much global influence? His inauguration, or coronation if one were to believe some of his die-hard supporters, leaves no stone of world affairs that cannot be unturned. Justin Trudeau’s fate was likely already sealed but was massively accelerated by the soft tactics deployed in The Donald’s rhetoric regarding Canada’s trade surplus and immigration issues with the United States. By many media accounts, President Zelensky of Ukraine is expected to cede territory to a Trump-led war intervention, and can it be in any doubt that a much-avoided ceasefire in Gaza is has found resolution because of Trump advisors being in the latest room that held discussions?

Therefore, howsoever the new presidency meanders, we can be assured that there will be a profound effect on energy markets. If the MAGA supporters are pleased, then the lobbyists of the oil industry are veritably cock-a-hoop. Quoted in the WSJ, Mike Sommers, the president of the API said, “Energy clearly was on the ballot, and we’re going to make the case that energy won.” This is in reference to how Mr Trump, on his way to the White House, could be heard by those that were actually listening rather than believing polls, espoused the virtues of global ‘energy dominance’ since proven to have been a vote swayer within the electorate.

Oil and Gas companies smell opportunity, and it aligns with the parochial attitude of the new administration. Think of a new twist in ‘buy American’ as a thriving domestic market forgoes any need for foreign oil and allows the playing of the ‘interest of national security’ card. Drilling, production, exports and most important of all, profits, will increase. That is of course supposing a steady oil price not suffering under a trading world contracting due to tariffs. The Outer Continental Shelf Lands Acts was used by President Biden to restrict domestic drilling, the same law can now be used by the President-Elect to banner his infamous “drill baby, drill.” With that in mind, the current White House resident’s New Year banning of offshore drilling over 625 million acres including the Bering Sea, Gulf of Mexico and both coasts might be the shortest-lived restriction in recent history.

The political ping-pong surrounding America’s huge oil industry is already wreaking havoc in oil prices. Joe Biden’s new sanctions on Russia are arguably primed to give his nemesis a massive oil price spike and inflation headache while arming Ukraine with a better negotiating position. However, it also plays into the new President’s hand as leverage against Russia and logically allows any increase in US exports to find markets once occupied by Russian oil. We will look at the monthly reports tomorrow, but even the oil-price-churlish IEA reckons on a significant disruption to Russian supplies under the new and recent sanctions, although in an interview with Bloomberg its oil market division head, Toril Bosoni, was reluctant to put a number to the significance.

The green lobby will have to look the other way for the next four years. By the look of things, and all political intent ought to be treated as a proverbial ‘pinch of salt’, there is about to be an explosion in the oil industry of the US. Many a proponent of alternative energy fear a US withdrawal from the Paris accords and domestically a revoking of tail-pipe emission rules and according to the WSJ an expectation to curtail fuel-economy rules known as the Corporate Average Fuel Economy, or CAFE, standards. As much as Donald Trump bellows support for fossil fuels, oil companies, the auto trade and ‘energy dominance’ the path is less than clear. The variables in price, value for shareholders, international relations and his potential interference in conflict situations mean that policy could well be ephemeral and will only lead to more market flux. Which is why, we stand guilty as charged of being besotted by the greatest market influencer in history and wonder along with all, what comes next?

Overnight Pricing

16 Jan 2025