Loading Resumes, Sanctions Might Tighten

The Russian-Ukrainian war, with all its consequences for the short and medium-term oil balance, remains at the centre of investors’ attention. Yesterday’s conflicting performance—RBOB falling, distillates rising, and crude oil settling broadly unchanged—suggests an undecided or cautious approach for now. The best way to sum up the current backdrop is to ask questions. Will the restart of oil loading at the port of Novorossiysk provide sufficient volumes of Russian products for willing buyers? Or will the threat of new US legislation imposing additional tariffs on countries dealing with Russia create further shortages, especially if effective Ukrainian strikes on Russian refineries continue unabated? Or will the widely anticipated stock build next year tip the scales to the downside? These are all valid questions with many possible answers; however, the ubiquitous view seems to be one that envisions no significant downside potential as long as Russian product availability remains scarce.

Stock markets are preoccupied with their own idiosyncratic puzzles. Nvidia’s quarterly earnings, due out tomorrow, are eagerly awaited, as is a series of delayed US economic data, chief among them Friday’s jobs report, which will decisively shape market expectations for the Federal Reserve’s next interest rate move. Uncertainty, unsurprisingly, lingers, and equities drifted lower yesterday. The souring of the mood was partly due to Amazon joining the wave of debt issuance in the tech sector as spending on AI infrastructure intensifies. When growth is fuelled by debt rather than equity, the repercussions of a potential downturn, which is by no means imminent, would be more severe, hence the pause in the stock market rally.

Changing with the Times

A month or two before the release of last week’s World Energy Outlook 2025 from the IEA, the upcoming revisions were explicitly advertised. It was well known that the energy agency of the developed world would now anticipate a prolonged reliance on fossil fuels, particularly oil, reversing the view it had held for the past five or six years. Its 2021 claim that no new investment in oil and gas projects would be needed to meet global warming targets, a stance that triggered a rather acrimonious relationship with OPEC, has been reversed, and those who accused the Agency of intransigence now feel vindicated.

Reality is usually more nuanced than headlines, and that is precisely the case here. First, without taking sides, it is worth noting that in 2021, the medium-term impact of the health crisis, which devastated the global economy, the refinery sector, and bankrupted several oil producers, was still unclear. Secondly, Russia’s nefarious invasion of Ukraine, which prioritised energy security and prompted calls for renewed investment in the oil sector, could not be foreseen. Nor was the re-election of a fossil-fuel-friendly US president in 2024, who brazenly uses his country’s dominant political and economic might to achieve its goals. Or, in a more PC-compatible formulation: the Trump administration’s requests have in several cases been acknowledged and granted by partners, including the IEA. The collective effect of these three major developments, each with far-reaching consequences for geopolitics, the economy, and the oil balance, has forced the IEA to change its mind, as embodied in the updated Outlook, probably a year or two later than warranted, some would argue.

When predicting the future, one must be prepared for all eventualities. While hoping for the best may be a cognitive bias, expecting the worst at the same time is simply common sense. From this angle, another argument goes, all that has happened is that a previously dormant scenario, the Current Policies Scenario (CPS), now complements the Stated Policies Scenario (STEPS) and the Net Zero Emissions by 2050 Scenario (NZE). It is tempting to resort to rudimentary interpretations and label CPS as “contemporary action,” STEPS as “political narratives,” and the NZE, quite simply, as implausible.

Whichever viewpoint one subscribes to, it is undeniable that the IEA now expects a heavier and more prolonged reliance on oil than previously projected. In the Executive Summary of the latest annual report, the head of the Agency emphasises that governmental and international efforts to limit global warming and reduce greenhouse-gas emissions are in decline; last year was the hottest on record; and the rise in global temperature has already surpassed 1.5 °C above pre-industrial levels.

Under STEPS, total oil demand is expected to peak at 102 mbpd around 2030 before gradually declining to 97 mbpd twenty years later. Global electric-car sales are forecast to rise from 20% to over 50% by 2035, although electric-vehicle (EV) sales will struggle in the US. One of the main reasons for peak oil demand around 2030 in STEPS is the assumption that 840 million EVs will displace 10 mbpd of oil consumption, chiefly in Asia and Europe. From 2030 onward, additional global energy demand will be met by renewables, which are projected to account for two-thirds of electricity generation by 2050.

The picture under CPS is markedly different. Oil demand will rise to 113 mbpd by 2050. (For comparison, in its latest monthly report, the IEA put next year’s global oil demand at 104.63 mbpd.) The main drivers of this growth are road transport in emerging and developing economies, increased demand for petrochemical feedstocks, and the resilience of aviation. Because of a lack of policy support, global EV uptake will slow, with China and Europe being the main exceptions. Oil and gas prices will rise through 2050. The US will remain the largest oil and gas producer, but production from the OPEC+ group will be 15% higher by 2050 than at any time before.

Reinstating CPS might be seen as an alignment with new circumstances, and a clear change in outlook, or, at the very least, a broadening of the horizon. It is nonetheless noteworthy that while the IEA forecasts 113 mbpd of oil demand under CPS by 2050, OPEC projected this level for 2030 in its World Oil Outlook 2025, published in July. By 2050, OPEC puts oil consumption at 122.9 mbpd. This gap is narrower than the one between 97 mbpd (STEPS) and 122.9 mbpd, but remains significant. Yet the fact that demand growth now seems a universally accepted base case raises the question of whether supply can keep up, given that the IEA estimates an 8% annual decline rate, equivalent to 8 mbpd, in production from existing oil fields. Next year may still see an abundance of oil supply, but based on the latest data from both the IEA and OPEC, and notwithstanding the still-yawning chasm between their demand projections, a tighter oil balance appears to be the recipe for a structural bull market around 2030 and beyond.

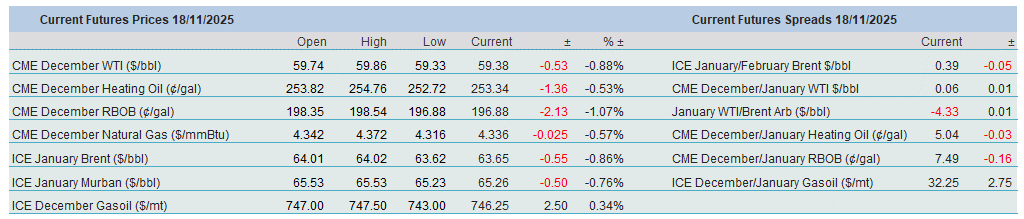

Overnight Pricing

18 Nov 2025