Lukewarm Reaction

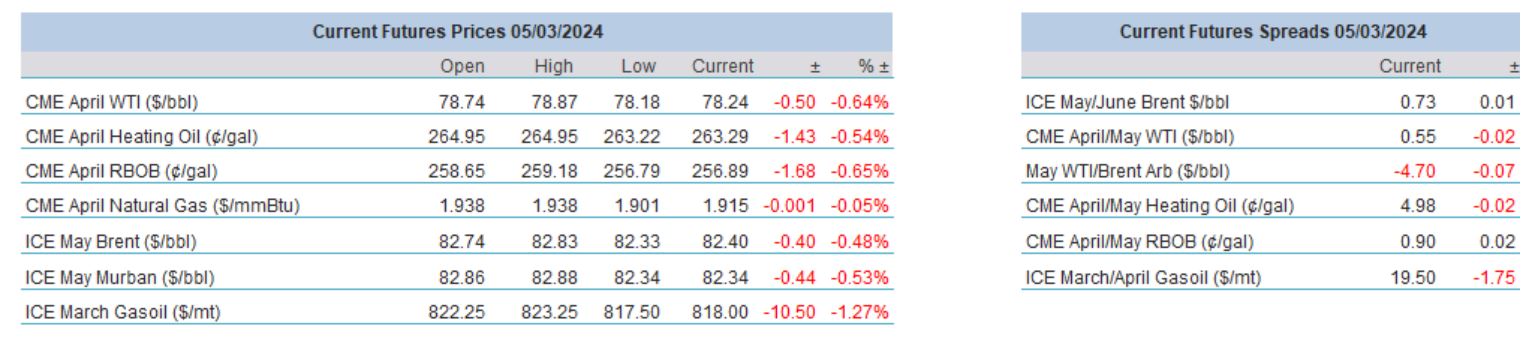

Despite the firm and unequivocal show of unity and solidarity, the weekend’s decision from the OPEC+ producer group to extend the current production levels throughout the first half of 2024 failed to inspire buyers and, apart from a brief rally, sellers dominated yesterday’s session. Notwithstanding the general gloom, it is probably fair to say that if the alliance adheres to its pledge, and admittedly the word ‘if’ must be written in capital letters, global oil inventories will deplete, especially if Russia keeps its promise and implements the additional 471,000 bpd voluntary reduction in production and exports, which is a plausible scenario given the country’s ongoing refinery problems.

For now, though, focus shifted elsewhere, and a smorgasbord of factors sent those with bullish propensity into hiding. Public enemy No 1 of a protracted rally and the $90/bbl oil price is the uncertainty surrounding interest rate cuts. The Fed chair’s testimony and the ECB interest rate decision on Thursday could revive hopes for a June reduction in borrowing costs. Secondly, the weakness in outright prices has been coupled with a significant narrowing of backwardation on WTI and Brent in, at least partly, what seemed the monthly rollover of length.

The third major factor, and this might worry potential buyers more than anything, was the tangible weakness in products. Although early indications imply drawdowns in both US gasoline and distillate inventories in tomorrow’s updated EIA stock data Heating Oil took a proper beating as the end of winter tames demand whilst RBOB was pressured by reports that the US Congress contemplates selling off its roughly 1 million bbls (OPIS estimate) Northeast gasoline reserve in the current fiscal year ending September 30. The ongoing but so far fruitless negotiations of a ceasefire in Gaza has also weighed on sentiment, albeit an eventual truce would not alter the underlying oil balance meaningfully. Further pressure comes overnight amidst concerns that China’s 2024 growth objective of 5% will prove overzealous. Despite yesterday’s somewhat disappointing reaction to the OPEC+ extension, the global oil balance is most likely set to tighten, helping prices rebound from any dips caused by actual or perceived short-term bearish developments.

GMT | Country | Today’s data | Expectation |

14.45 | US | S&P Global Composite PMI Final (Feb) | 51.4 |

15.00 | US | ISM Services PMI (Feb) | 53 |

20.30 | US | Fed Barr Speech |

|

SPR aka PPR

Replenishing the US Strategic Petroleum Reserve is undoubtedly under way. The SPR played a pivotal, albeit controversial, role to calm galloping prices in the immediate aftermath of Russia’s full-scale invasion of Ukraine in 2022. Nearly 220 million bbls of crude oil was released collectively from emergency stocks; on top of the 180 million bbls that was sold during a six-month period the sale of 38 million Congress-mandated barrels was also part of the whole package.

In effect, the drawdown on SPR more or less matched the intended total volume. Strategic stocks bottomed out at 347 million bbls in July last year, which were some 230 million bbl or 40% lower than in March 2022. However, SPR crude oil inventories had been gradually depleted from the peak of over 720 million bbls observed in 2011 close to 620 million bbls by 2021 as US shale production increased.

Back to the latest release, the US administration collected around $95 for every barrel it sold out of the Reserve and its declared goal is to buy them back around $79/bbl, potentially enriching the taxpayer by nearly $3 billion. So far, less than 30 million bbls have been replaced and the Department of Energy will plausibly bide its time to completely re-fill the SPR being cognizant of the impact a sudden rush to the market might cause to domestic retail gasoline prices in an election year.

Considering the seismic changes the US oil industry has undergone in the past 10 years the role of the SPR has clearly been reassessed. In layman’s term, it is becoming a political tool. The world’s biggest consumer has also found itself to be the biggest producer and consequently its reliance on foreign oil has considerably diminished. US crude oil production nearly tripled in 16 years. After lifting the crude oil export ban at the end of 2015, the country has turned into a net exporter. In 2015, the US demanded more than 5 mbpd of foreign crude oil and products to satisfy its thirst but last year they sent nearly 2 mbpd overseas on a net basis.

Which means, that strictly speaking the US does not need to maintain strategic stocks as defined by the International Energy Agency. The IEA requires member countries to hold strategic oil inventories, that equal at least 90 days of net imports of the previous year. The status of the US as a net exporter does not entail maintaining SPR.

Reality, nonetheless, deviates from theory. In fact, Democrats have been coming under pressure from Republican lawmakers for allowing strategic stocks to fall to their lowest level for 40 years. Of course, it is chiefly part of political horse trading as in case of a genuine emergency, let it be unforeseen global disruption in oil production or weather-related domestic supply issues the US is ill-prepared to manage crisis situations as nearly all of its SPR is in crude oil and concentrated in four caverns along the Texas and Louisiana coastline.

Yet, the SPR will probably play a salient role as a modus operandi for the US administration, but it might have to be re-christened to PPR – Political Petroleum Reserve. Prior to the 2022 sales SPR had only been used three times as emergency drawdown with the 2011 IEA coordinated release due to Libyan supply disruptions being the last occasion. It has been utilized a few times as exchange agreements with private companies whilst non-emergency sales, to respond to lesser supply disruptions or to raise revenues, have been authorized 9 times in the 30 years.

It is debatable whether the 2022 drawdown fits into any of these categories. Firstly, the volume is unprecedented, it was almost 10 days of US oil demand. Secondly, US commercial stocks did not plunge considerably after Russia’s invasion of Ukraine, in fact, they started to build from April onwards. Domestic crude oil production had also been recovering uninterruptedly from the pandemic-induced devastation and the US remained a net exporter of crude oil and petroleum products. Its oil supply was never in danger. As a matter of fact, 2022 was the first full calendar year when its net export volume exceeded 1 mbpd. The release was most likely politically motivated to rein in gasoline prices, something that is expected to happen on a more frequent basis going forward. At the same time, the basic concept of petroleum reverse might be recalibrated and turned into energy reserve as the transition from fossil fuel to renewables will appreciate the relevance of other minerals and raw materials in the energy mix.

Overnight Pricing

© 2024 PVM Oil Associates Ltd

05 Mar 2024