May We Have an Iran Deal Please? Not a Microchip One

The world will have to wade through another standoff in China before any sort of help from Beijing in ending the greater standoff of the Iranian war. There is no end of flattery and flummery between Presidents Xi and Trump at the start of proceedings and most opinion from a broad range of commentators is how the US President enters the negotiations with a much weaker hand than he might like. With various court decisions still ringing in his ears and pulling the rug from under Trump's tariff policies, Xi will be less inclined to be either brow-beaten or accept China is the weaker partner in this trade relationship. Eyeing events through the prism of an oil perspective, any further trade buddying is a pleasant appendage to dwell upon at a later date, what interests our fraternity is whether China is prepared to use its leverage and bring Iran back to a negotiating point where the US will be able to conduct diplomatic business.

For it appears that the billion barrels of oil stuck behind the Strait of Hormuz is causing consternation within the three agencies that offer monthly perspective of the state of supply and demand in global oil flows. The EIA, IEA and OPEC, which we will touch upon tomorrow, are all warning of depletion in supply that will not come anywhere near satisfying demand. This has been consistently reflected in the recent weekly EIA US Inventory Reports. Crude holdings fell by 4.3mb and within that headline figure, a continued fall in imports and rise in exports. Distillate stocks are 4mb below the 5-year average, and importantly using the same measure for Gasoline, the motor fuel is nearly 7mb short. This is reflecting the Short-Term Energy Outlook produced by the EIA on Tuesday in which it expects global oil stocks to decline by 2.6mbpd on average in 2026. Whatever trade mission the US President thinks he is on in Beijing, the so-called sidecar of Iran is where most of the world’s interest lies.

Inflation can no longer be ignored

It is a convenience to blame the elevated inflation in the United States on the current oil embargo being practiced by both parties in the Persian Gulf. Yet the source and platform for higher prices is the massive stimulus program undertaken by successive Administrations in the post-pandemic, post-Ukraine invasion era. The amount of money washed into the American system is a staggering $5 trillion Dollars, an easy roll off the tongue, but when written down it is $5,000,000,000,000 and almost incomprehensible, and although it never happened, it is worth noting for context purposes that if such monies made it to the 345 million US citizens, it would work out to $15,000 each. Howsoever it landed and in what mode is almost irrelevant, the point is with such money, Uncle Sam, after the ravages of Covid, has been in the market to buy ‘stuff’, and in size, for the past five years.

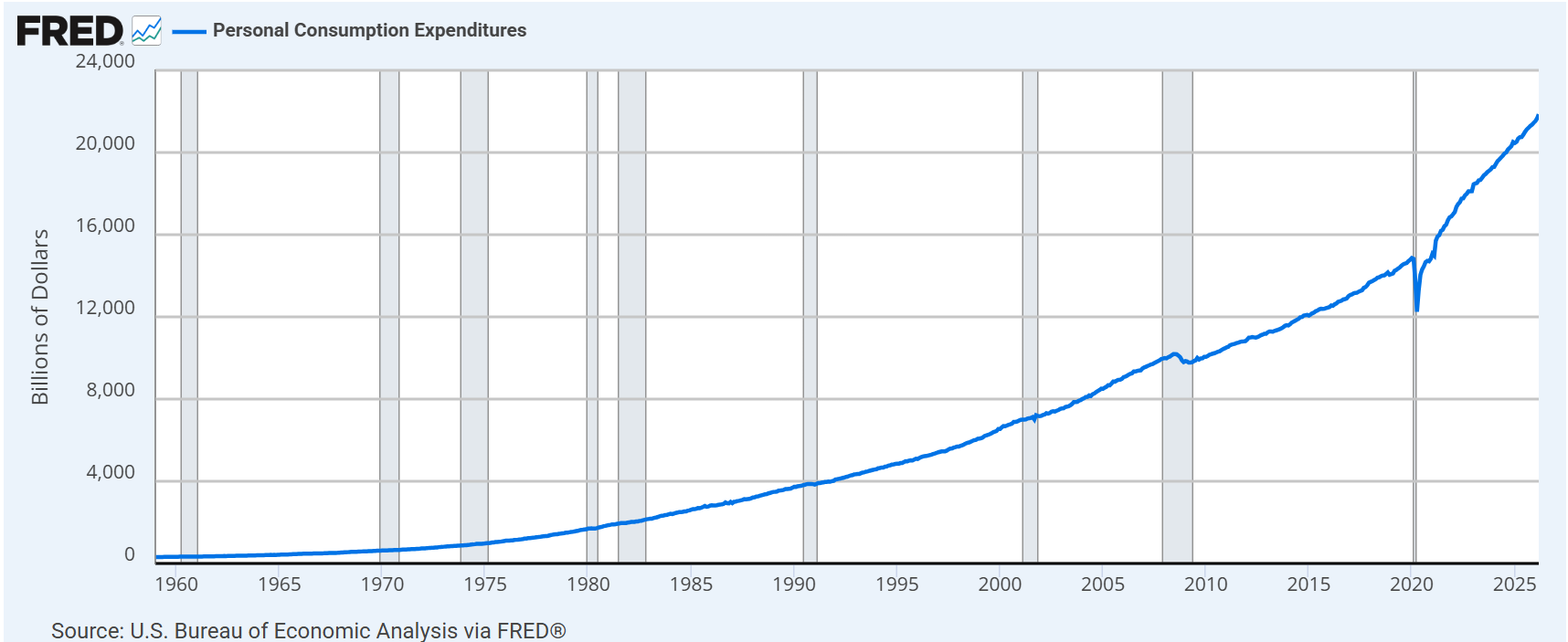

The shaded areas in the above chart indicate US recessions, but the acceleration in personal consumption expenditure is plain to see after the pandemic. Within this period the IMF has noted continued labour income growth has been supporting consumption across all segments of the income distribution, with the post-pandemic period registering a somewhat higher marginal propensity to consume out of that income. This has changed in recent times due to instability. According to the Peterson Institute year-on-year average hourly earnings sit at roughly 3.6 percent. However, this marks a deceleration from the annualized 4.1 percent growth seen between mid-2023 and 2025, largely driven by a slowdown in the health and education sectors. Yet when adjusted for inflation, disposable personal income is still showing steady monthly increases of around 0.6 percent. Direct personal stimulus cheques have ended, but with the state running guarantor for almost everything after the pandemic, with unemployment benefits expanding and rocketing prices in stock markets and real estate, US household net worth has hit record highs, although it is worth noting that the wealth gap has increased commensurately.

All of this is obviously inflationary and the reason why Jerome Powell has led a call of caution when urged to unshackle the US economy from higher interest rates. It has been a battle to tame CPI from its bottle-necked, price-gouged highs of 9.1 percent in July 2022, but it has never managed to hit the 2 percent target so yearned for by this current stock of Federal Reserve members. Therefore, Tuesday’s hotter-than-expected CPI reading of 3.8 percent, is once again drifting higher and away from comfort for the Fed and makes the newly confirmed Chair Kevin Warsh’s job so much harder. In fact, markets are now pricing in an additional rate hike before the end of the year which will have a certain commander-in-chief preparing both his ‘Truth Social’ barrels for an early morning tirade. Indeed, the Fed-watched Core PCE Price Index, in unison with the above image, is knocking on the door of 4 percent and there can be now no way the Fed, no matter the make up of the board, will tempt inflation higher by unleashing more easing into an American public, while slightly cowed, shows more than willing to take up the mantle of spenders.

However, in the CPI report, services, gasoline, electricity, and food all spiked, and while the foundation of inflation discussed above echoes through the economy, whatever inflation was caused by the outbreak of the Ukraine war can easily be repeated in the more important bottleneck of Hormuz. There is no getting away from it, this war is starting to bite and has come home to haunt the great American consumer. According to GasBuddy, at the end of February, the 18-month average retail price for regular Gasoline in the US was $2.90/gallon, it is now $4.50/gallon and in some areas already printing above $5 and in California, $6. Iran’s game play is to export its Pinch of Hormuz to the US homeland, and it has indeed arrived. The warnings and now truth of inflation are starting to hit, and the importance cannot be overstated. Such inflation will change the spending of Americans and by doing so, how debt, based on growth, is serviced. This war needs to be over very soon, for the sake of all.

Overnight Pricing

14 May 2026