Middle East Incursions Throw Oil a Lifeline

Such is the world that we live in that state sponsored murder is measured in geopolitical risk to markets rather than any outrage at cross border assassinations. Whether or not this proves to be the case in the killing of Ismail Haniyeh, the leader of Hamas, in Iran will no doubt come to light, but such incidents remind the market on how it should not take the Middle East as a contained issue. If the reported bombing of the Hamas leader's house does prove to be the work of Israel, it will be responsible for daily back-to-back bombings in two capitals, the first being of the killing of a Hezbollah leader in Beirut. This then is the main reason oil prices pick their skirts up having endured some very negative sessions of late, due mainly to the poor showing of China data and the struggle of crude baskets outside of the North Sea to find anything like its interest, driven by the US influence via the WTI/Midland inclusion. Such tightness is not set to go away according to the API data. Inventories fell across the board, Crude reduced by 4.5 million barrels, the Cushing hub by 0.9mb, Gasoline by 1.9mb and Distillate by 0.3mb. In a different mood, such draws along with bombings would see more of a reaction, but there is an air of defeatism seen by the grind lower in prices and there is not much at present, including an OPEC+ get together, in the near future to suggest any sort of reversal or indeed inspire an interruption to the fixated gaze that dwells on all that is macro.

The wider suite competes for attention, even before the Tier 1 of all Tier 1 data comes in the form of the FOMC rate decision later today. Not that much more than a 'push' should be expected, it will be how future decisions might be framed. In Japan, the BoJ increased rates by a surprising 15-basis points and interestingly will cut its bond buying program in half by 2026. The Yen ticks higher and the Nikkei counter-intuitively rallies hard because the economy is seen on a better footing, however, it is not enough to snatch the all-encompassing attention toward the goings on at the Federal Reserve later. In the arena of corporate profits, Microsoft quarterlies disappointed while AMD's proved that chipmakers rather than the companies that use them remain the darling of investors. The Nasdaq is inspired this morning and tech stocks across the globe account for the rally in bourses, even in China which again suffered another poor showing of contraction in the NBS Manufacturing PMI at 49.4. Such laboured industrial activity will be added to the reasons why China is no friend to oil prices at present.

OPEC pursues hearts and minds

Last year in November’s medium-term outlook, the International Energy Agency upped the ante on its view that oil production and consumption were coming to a zenith, warning that oil and gas industries were about to face their moments of truth and must use every opportunity to join in with the growing advancements in energy transitions. The IEA’s Executive Director Fatih Birol was rather uncompromising in his language saying, “Oil and gas producers around the world need to make profound decisions about their future place in the global energy sector.” The agency’s view extended to something of alarm sounding on fossil fuels being unsound in investment, traditional oil and gas corporations will lose 25% of value and ‘if’ it is the case that climate goals are reached and the world manages to curb global warming to 1.5 degrees Celsius, those valuations could fall by 60%. Run the tape forward to last month and the Paris-based bias shows little sign of abating. Seeing oil markets that will be adequately supplied through to 2030, its preferred pinch point, the end of the decade will be where demand levels out at 106 million barrels per day. Extolling the virtues of renewables in January, the IEA lauded on how capacity to global energy systems increased by 50% in 2023 and predicted a two-and-a-half times increase by the 2030 favourite. Birol continued to push, claiming that onshore wind and solar generation are now more economic than fossil fuel plants giving hope to the COP28 agreement of tripling renewables, doubling energy efficiency, cutting methane, transitioning from fossil fuels and increasing financing for emerging and developing economies.

One wonders whether such zealousness and preaching from the pulpit does not serve proponents of the green agenda poorly. Even knowing the somewhat over-egging of oil demand from OPEC comes from self-interest, it is delivered at least a little more subtly. Odd in these strange times that while parts of the US government are in the process of initiating a probe into suspected collusion between big oil and OPEC, there is growing global antipathy towards a green agenda being forced upon electorates that is fertile ground for nationalists sowing discord and dissension. Timely indeed then that an open letter on Monday posted on OPEC’s website from HE Haitham Al Ghais, the OPEC Secretary, cuts a conciliatory and dare one say an even-mannered approach to new energies from an electricity demand point of view. Debunking the concept of a zero-sum game in energy, where one transposes another, he instead pursues the validity of all available energy resources and questions the logic of date naming energy replacement events. “Reality tells us that oil does not operate in isolation, cut off from other sectors and industries. Rather, such is the versatility of petroleum and petroleum-derived products that they play an indispensable role in a host of other sectors and industries”, so the Secretary continued, adopting the role of a market sage. There is a reminder that all energy, particularly electricity, benefits from having exposure to oil or oil-derived products. Cooling, lubrication, insulation, adding that nearly a quarter of the weight of a large power transformer consists of transformer oil and insulation materials. His transportation observations are obvious but the reliance on electricity to achieve zero emissions by 2050 is worth taking note of. Current global electricity generation is short of 30k Terawatt hours (TWh), that would need to expand massively to up to 130k TWh, a nigh 5 times increase in 25 years. The strain on national electrical grids would be immense, the new roll out of cabling vast and the cost of which enormous. Without a viable alternative to the delicate end part of conductivity, one wonders what the price of copper might just be if this all comes to pass? Haitham Al Ghais finishes in reasonableness that one source of energy need not be contested against another, interrelation should instead be pursued leading to a much more joined up approach. Such diplomacy, even if ultimately driven by self-interest, is likely to fall on receptive ears.

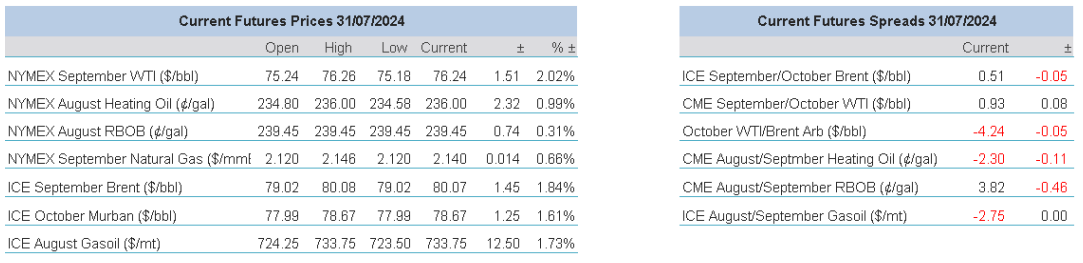

Overnight Pricing

© 2024 PVM Oil Associates Ltd

01 Aug 2024