Middle East Premium Subsides, Macro is Front and Centre

It would appear as emotive as the current situation in Gaza/Israel is, cooler heads are prevailing and the idea of conflict spread is slowly turning into, and stealing from the alternative energy lobby, conflict capture. The murderous incursion into Israel and subsequent horrific flattening of parts of Gaza saw Brent rally $10/barrel from 06/10/2023 to 20/10/2023, but has now given nearly all of those gains back. Our view remains that to dismiss the situation as done is way too soon, however, the immediacy of attention has abated allowing the investor community to glance further afield and take into account other drivers that might impinge on oil’s progress, and excluding the United States, they are by in large troubling.

Some of the morning’s attention turns to China and the somewhat nascent mini-revival going on. Results from stimulus are mixed but it does appear that government without taking the ‘gloves off’ are attempting to find new ways in aiding economic recovery. In a Bloomberg opinion reporting on Central Financial Work Conference that only occurs twice a decade, it comments on laser-attention to the financial system and the stern approach being showed by delegates. However, at present, ‘nascent’ is as close as a revival might be for yesterday’s misses in the NBS PMIs is followed today by private Caixin Manufacturing PMI for October which missed the forecasted 50.8 level and shows contraction at 49.5.

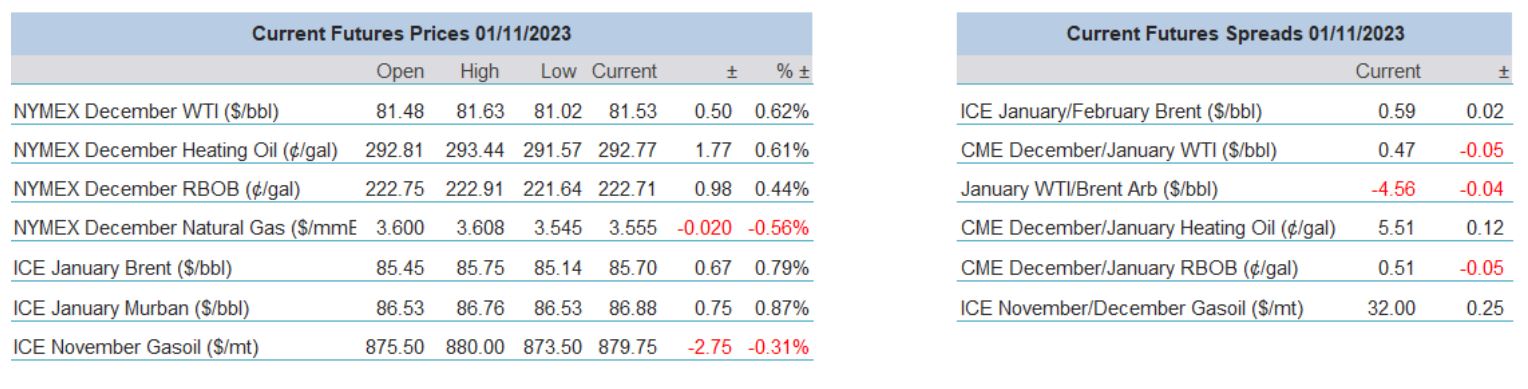

The API inventory report offers draws in Gasoline of 0.4 million barrels and Distillate of 2.5 million barrels. This might be explained away by last week cut in refinery runs and utilisation. Those that have been concerned by the very short state of stocks at Cushing, Oklahoma will note a small build of 0.4 million barrels which is line with the TankWatch build call of 0.34. The crude build of 1.3 million barrels is hardly surprising bearing in mind the high level of production that the US is achieving at present and we await confirmation from the EIA report later. Builds, low runs and the inability of US crude to get to water because of freight will continue to trouble arbitrage values. What will trouble all thinking today is US based, from ADP and JOLTs numbers in employment, ISM for Manufacturing PMI, but mostly the FED interest rate decision at 18.00 GMT. That the rate will be unchanged is almost a given, but it will be what the all monetary-powerful Jerome Powell has to say in the presser afterwards and if his words can bring light onto a recently grim global economic outlook, particularly that of Europe.

GMT | Country | Today’s Data | Expectation |

12.15 | US | ADP National Employment (Oct) | 150k |

14.00 | US | ISM Manufacturing PMI (Oct) | 49 |

18.00 | US | FOMC Rate Decision | 5.375% |

Europe struggles on

Things in the main do appear a little brighter in France. After last week’s affirmation by the rating agency ‘Fitch’, confirming AA- standing and offering an overall opinion that the outlook was stable and although growth will likely slow for calendar 2023 at 0.8%, it should outperform the forecasted 0.6% of the Eurozone as a whole. This slightly rosier outlook was confirmed by the quarter-on-quarter GDP growth of 0.1% published yesterday in line with expectations. Bloomberg Economics are a little more expansive and possibly a little more optimistic referring to an increase in household demand and business investment. Cushioning France’s populace from strangling ECB interest rates is the high level of fixed rate mortgages.

Italy remains a topic for alarm among European watchers. This is despite recently managing to avoid a downgrading by Standard & Poors, holding onto its BBB rating and for the moment keeping some distance away from ‘junk’ status which it is closer to in the eyes of Moody’s. Currently standing at 0.7% for calendar 2023 GDP, S&P predicts a return to 1% growth by 2025 which is also why Italy has held onto a ‘stable’ labelling. Yesterday Italy scraped both a 0% reading on year-on-year and quarter-on-quarter growth against a joint +0.1% call and according to some economists just managed to avoid recession.

Germany will be the only G7 country to see contraction this year as the IMF recently forecasted its calendar 2023 GDP growth to be -0.5%. That view is probably unlikely to change even after it yesterday it beat year-on-year (-0.3% versus -0.7%) and quarter-on-quarter (-0.1% versus -0.3%) GDP in what has been a miserable time for economic markers and recession chat is never far away. However, in the event of a continued fall in oil prices Germany’s outlook will improve, yesterday’s year-on-year October inflation of 3.8% reading, beating the forecasted 4% is due in part to the fall in overall oil prices.

This influence on economic endeavour by the oil price is reflected by Eurostat, the statistical office of the European Union and the collator of ‘Euroindicators’. Eurozone October year-on-year CPI flash was 2.9%, beating the expectation of 3.1%, much improved on September’s 4.3% and at the lowest level for over 2 years. The breakdown shows the following expectations in the flash assessment; alcohol and tobacco 7.5% versus 8.8% in September, services 4.6% versus 4.7%, industrial goods 3.5% versus 4.1% and finally the major influence being energy at -11.1% versus -4.6% in September. As much as this temporary taming of inflation is welcome, it appears that Christine Lagarde’s attitude that consideration of a pivot in interest rate policy is premature is somewhat justified, and one wonders if consideration is being given to the outsize influence energy has in the Eurozone. The awful PMIs of last week are confirmed in their signposting of an economic struggling block as the October year-on-year GDP flash read -0.1% against a +0.2% call and September’s level of +0.5%.

Not everything in Europe’s economic woe is all about oil. The make-up of a country’s financial identity is not easily picked apart or even easily compared with other similar size economies, let alone how they interweave into a bloc such as the EU’s Eurozone. For all the virtue signalling of alternative energy and net-zero targets, Europe is vulnerable to energy shifts which seem to have been made worse after losing the cheap energy source of Russia and indeed energy security. Oil demand will depend on price and industrial performance for some time yet and that relationship for good or ill will continue to be newsworthy.

Overnight Pricing

01 Nov 2023