A Mixture of Stress and Relief

The whipsawing and day-trading attitude our market is experiencing has inevitably led to similar behaviour across all other investment arenas. The importance of the current war in and around Arabian skies is touched upon below, but to see bourse indices moving in degrees of multiple percentage points and sometimes double-figured ones, is almost as unsettling as the conflict itself. Still, Asian markets today open a little more brightly as some of the woes on the horizon are somewhat soothed. The expectation of an imminent interest rate hike by the Bank of Japan appears unfounded as Bloomberg reports, and although China, in its 2026 outlook set GDP between 4.5 and 5 percent, the lowest in many years, it matches expectation and with it, a pledge to keep stimulus at 4 percent of GDP.

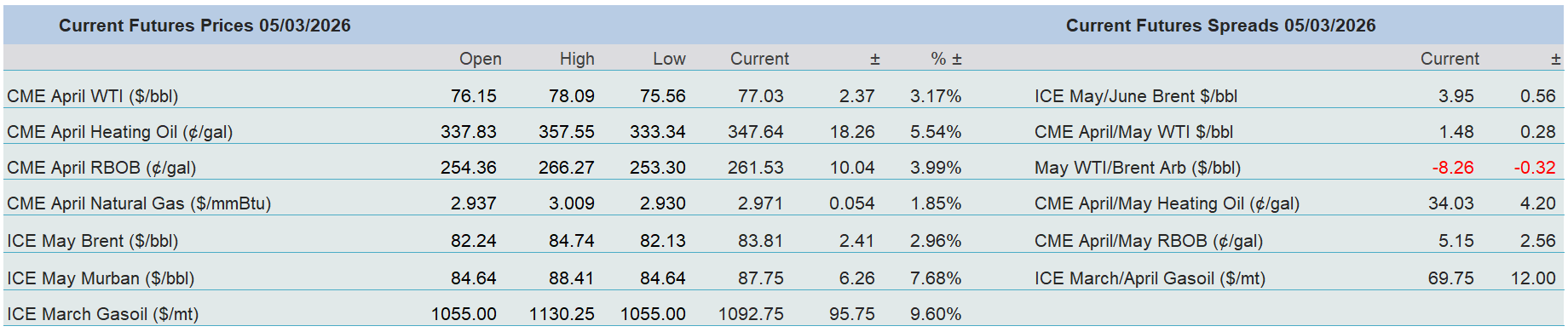

No doubt these swings in sentiment will follow emotions, but it is Asia which is bearing the brunt of the initial costs of war. Oil sees a tightening situation and this morning, and staying with China, its government has turned even more defensive on energy security as, according to Bloomberg, it tells the largest refiners to suspend exports of diesel and gasoline. The immediate outcome is the price of M1 Gasoil futures entering into prices not seen since the Russian invasion of Ukraine. This heightened state of vulnerability is also witnessed in Japan as refiners ask the government to release strategic petroleum reserves. This stress was first represented in Asian crude grades this week and continues with the M1 Brent/Dubai Futures spread trading at an eyewatering $10/barrel this morning, on Friday it settled at $2.39/barrel. With the war almost being ratified by the US Senate which threw out a motion to stop the airstrikes on Iran, and the sinking of an Iranian frigate by a US submarine off the coast of Sri Lanka, this war is taking on a global effect with potentially lasting repercussions.

Back on the menu of dinner party chat

What a remarkable turnaround in relevance. For nearly a year, and apart from the joint US/Israel bombing of Iran’s nuclear facilities in June, the decline in oil prices have matched the interest shown by the myriad investors that stalk the halls of opportunity. Global overproduction, a policy change by OPEC and an ability, learned during the Gaza conflict, to complacently shrug off geopolitical threats, led to not only uninterest from institutional investors but the active trading of commodity trade advisor funds (CTAs) being more likely tracked as being keen shorts. The IEA and its like have performed an about face, albeit reluctantly, their former narratives of ‘peak demand’ without doubt contributed to not only a lack of long-term positioning interest in oil and fossil fuels but might also have been possibly referenced as capex saw a significant shaving.

According to Carbon Tracker, while 2024 investment was up from the lows of the pandemic, it has stabilised at a level roughly 40 percent below the peak of 2014-2015; falling from nearly $900 billion a year to a steady $550-600 per annum. The recent lack of fancy for fossil fuels is plotted well in the weighting of oil companies within the S&P 500. Using the same time frame from 2014-2015, the energy sector’s representation has fallen from around 8 percent to 4 percent in the present. In 2008, Exxon was the highest valued company in the S&P, as of the year end in 2025, it was fourteenth.

Therefore, what harm could a blip higher in oil prices actually do? Ahem. The Cinderella of the investment suite has just turned up to the ball and what a dance it is creating. The hiccup in how the future of A.I. and its associative partners in technology has inspired a rotation in US exposure to other geographies. The ‘sell America, sell the Dollar’ has seen huge interest divesting into the likes of Japan, South Korea and even Europe, whose stock markets and valuations have looked very underweight when compared with those listed in the DOW, S&P and Nasdaq. At close of business last Friday, the Nikkei 225 Index was up 17 percent YTD, it has lost 7 percent of gains since Monday’s opening; the South Korean KOSPI Composite Index was up 49 percent YTD, it is now trimmed to up 33 percent and the Europe STOXX 600 Index was up 7 percent YTD, it is now only up 3.5 percent. What do these three contemporary stock market sufferers have in common? They are all importers of energy.

Adding to the woe of manufacturing exporting countries are the ballooning costs of freight and threats to shipping lanes, albeit in and around the Arabian Peninsula, the very nearby performance of these large theatres of trade are becoming increasingly threatened. Whatever paths the Bank of Japan, the Bank of Korea and the European Central Bank had in mind for interest rates and or stimulus, they will have to be remapped. Even within the US Federal Reserve, those of a mind to be influenced by the constant badgering of Donald Trump for the central bank to lower interest rates, will need a blindfold and noise reducing headphones to ignore the inflation potential of high-flying oil and gas prices.

There are obvious winners, including energy exporting countries and oil companies, but their populations and employees will join the rest of the globe and be subject to the scourge of all economies, inflation. The old saying goes that to keep repeating a mistake is madness, but the world has not wised up from the ravages caused by the oil crisis of the 1970s and every other scuffle since involving this saturated centre of oil and gas production. There is not a crystal ball clear enough to be a seer into where this all ends up. Is it game of counting missiles and who runs out first? We obviously abhor this war, but we love how such conflicts inspire a pleasing turn of phrase which might just be apposite. The cost of anti-missiles such as the US Patriot system is $4 million a pop, the cost of Iranian drones is estimated at $20 thousand, “shooting gold at plastic” indeed. Will it be the miliary cost of the war that ends the US campaign, or will it be crude touching $100/barrel, that will see President Trump take the off ramp? We do not know, and suspect you, dear reader is as such stymied. What we do know is that our market is back in vogue, even if it is not in a good way. Lest we forget, and to ruin a Patrick Swayze moment, “nobody puts oil in a corner.”

Overnight Pricing

05 Mar 2026