Moving Target

This is a conflict that started more than three weeks ago, and was meant to destroy Iran’s nuclear capabilities, eliminate its missile threats, and pre-empt an imminent attack. Now it is a war aimed at preventing oil prices from rising further. If you have a sense of déjà vu, it is because you have read Winston Churchill’s witty paraprosdokians, one of which reads: “Shoot first and call whatever you hit the target.”

The next $20 move is unclear, but expensive energy is clearly taking its toll. Global business activity has sharply reversed, as purchasing managers’ indexes confirm. With oil around and above $100/bbl, private sector growth has stalled from Australia to Europe and the US. Fear of inflation is rising, and talk of stagflation is growing louder.

Notwithstanding Monday’s sharp fall in oil prices and the rally in equity markets, the promise of constructive negotiations between Iran and the US is, for now, proving to be a nothingburger, even though progress is claimed repeatedly by the US, which sent a 15-point plan to Iran overnight to end hostilities. Hence, the renewed selling pressure in oil. Its seriousness is called into question by reports of the US deploying 3,000 troops to the region, as reported by The Wall Street Journal. The next deadline, whether meaningful or not, is likely Friday. The 48-hour window presented to Iran on Friday to open the Strait was extended to five days on Sunday.

Sometimes, indeed, increasingly, it appears that the US administration itself does not know how to mitigate the adverse impact of its apparent miscalculation of the resilience of the Iranian regime and the likely duration of the war. The US President’s press conferences are confusing and incoherent. The next steps are unforeseeable. The US could declare victory and withdraw from the region today or tomorrow, or invade Kharg Island on Donald Trump’s whim. Politicians like to boast that every option is on the table. In this conflict, it actually is.

What is curious to observe is that the Israeli legislative election is scheduled to be held by October 27, while the US midterm elections are on November 3. It is an ironic twist of fate that both Israel and Iran have vested interests, albeit for very different reasons, in prolonging the conflict into the fourth quarter of the year. The end is nowhere in sight. But it can turn on a dime, faster than an oil tanker can in the Strait of Hormuz.

Peace Talks or Not, Tightness Will Persist

Prior to Monday’s bloodbath, triggered by reports of an ostensible diplomatic push to amicably resolve the Iranian crisis, the prevalent view on oil prices was one of decoupling. Futures prices, the thinking went, did not truthfully reflect the gravity of the situation in the Persian Gulf. The short-, medium- and long-term damage from the joint Israeli/US attack on Iran, and the resultant retaliatory measures, including the closure of the Strait of Hormuz and assaults on the region’s energy infrastructure, was far more severe than the Brent rally to $119/bbl implied.

In light of this week’s turn of events, the same question can be asked: was Monday’s sharp sell-off, and this morning’s move, an over- or underreaction to reports that the conflict would soon be over? How much weight should be placed on the words of a rambunctious US president, whose behaviour could at times be deemed more erratic than that of Louis XIV after an eventful weekend? To extrapolate this dilemma to the oil market, two questions need to be asked: Will there actually be a long-term, reliable ceasefire between Iran and its adversaries? And how will oil prices react if the answer is yes, and if it is no?

To begin with, what are the chances of a sustainable agreement between Iran and the US? The fact that Iran was swift to rebuff the US claim of talks does not bode well for the prospects of resolving the conflict. Of course, the word “resolving” has more than one definition, but given the differing interests of the parties involved, namely the US, Iran and Israel, it is overzealous to envisage an agreement that can be relied upon for years to come. The current Iranian president, Masoud Pezeshkian, recently laid down his country’s conditions for ending the war: compensation for the damage caused by US and Israeli bombardment, the right to enrich uranium, solid guarantees to prevent future attacks, and possibly sanctions relief. Israel, whose objective is to obliterate Iran’s nuclear programme and remove the hard-line regime, is unlikely to agree to such conditions. A substantial and enforceable ceasefire will therefore remain elusive.

If one assumes that there will be one, at least on paper, and that the Strait of Hormuz reopens, will oil prices return to where they were? The chasm in views is yawning. During this week’s CERA conference in Houston, the US energy secretary put on the obligatory brave face and said that oil prices have not climbed high enough to hurt demand (so why the perceived negotiations with Iran, one might ask). Other industry leaders disagree. The CEO of ADNOC warned of slowing economic growth, while investment bank JP Morgan concluded that the closure of the Strait and the shut-ins of energy installations had led Asian consumers to rush to secure crude oil, product and LNG supplies.

There is a strong case to be made that outright price movements, both higher and lower, reflect the expectations of financial investors. It is the unmitigated hope that the crisis will be resolved sooner rather than later. Spreads, particularly the price difference between products and crude oil, mirror the reality in the physical market. Take yesterday’s performance as a vivid example: the US crude oil benchmark ended the day $4.22/bbl higher, but Heating Oil gained $9.86/bbl equivalent. The crack spread remains strong for a good reason. The damage inflicted on energy infrastructure so far will take a long time to mitigate. Global, and especially Far Eastern, product inventories are likely to plunge in the foreseeable future as competition for diminished supply intensifies. The destruction suffered by Qatar’s pivotal LNG plant, which could reportedly take as long as five years to repair, will have a knock-on effect on Asian crude oil and product supply.

It is never wise to underestimate the power of financial players, and time will tell whether they are being complacent about the medium- to long-term ramifications of the Iranian war on oil supply. Yet the fragile status quo observed in the Middle East before this month has been upended for years to come. The amount of capital allocated to oil will remain elevated compared with pre-war levels, simply because the global oil balance will tighten, global and Asian oil stocks will deplete, and the world’s most salient oil-producing region will have become a riskier place than before. And if the announced peace talks turn out to be a damp squib and hostilities continue, revisiting recent peaks cannot be ruled out either.

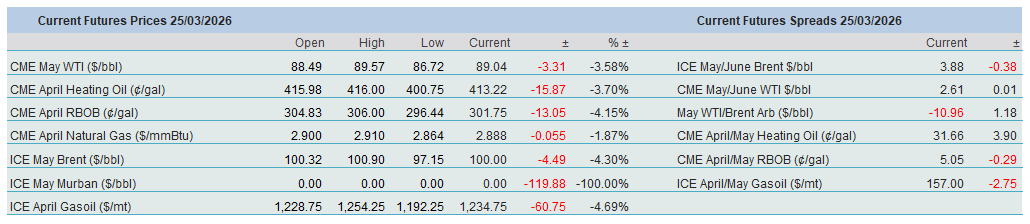

Overnight Pricing

25 Mar 2026