Near Over-Sold Status Brings Relief, But Oil is Spooked

Ordinarily, the API data on Tuesday evenings is viewed as a signpost to the much more important and watched EIA/DOE inventory report that graces our screens on Wednesdays. However, a missed week by the EIA, due to a systems upgrade, gave more importance to an API Crude build of 12-million barrels and oil prices failed to find much of a bid all day. Other factors that harried prices lower included continued stories of the state in which China’s economic trade finds itself. Analysts spent much of the day pondering over the recent mixed import/export data and most took unkindly to what was revealed. With shrinking refinery margin, opinion from Vortexa suggests that China’s crude inventories are starting to build again and there will be less need to go to market for additional feedstock. Quota for refineries are all but spent and according to OilChem via Bloomberg, oil product exports will plunge by 40% in November compared with October which if anything like true, nails shut the case for short-term crude demand.

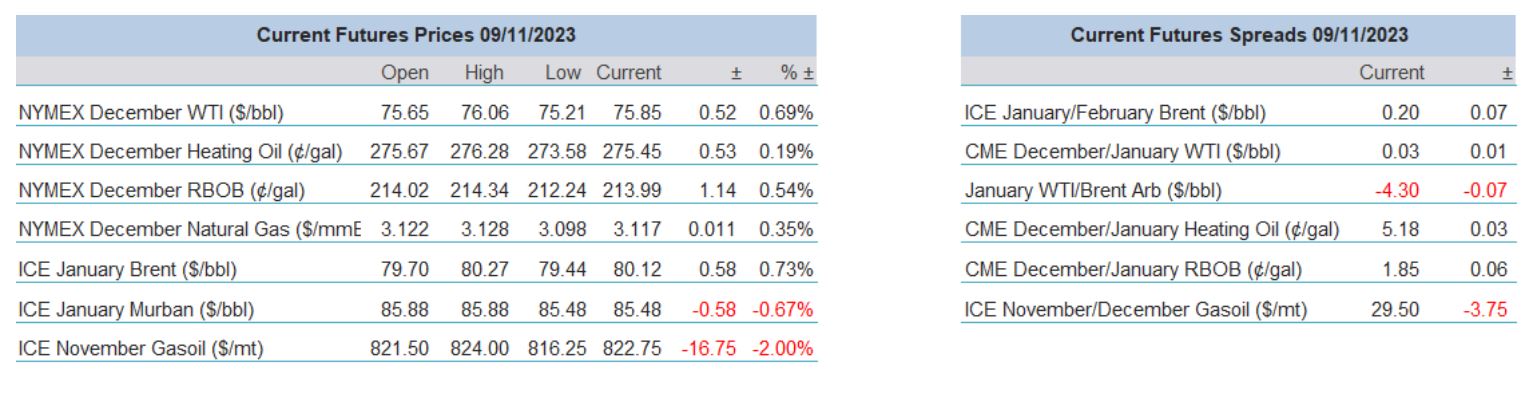

Technicalities came to the fore, and as we discussed recently, futures markets were likely subject to position moves by index fund rolling and using Brent as an example, Open Interest saw a sharp reduction on Tuesday. Front month January lost 36,000 lots and while difficult to prove all was down to financial action, a likely repeat today when Open Interest is published for Wednesday will confirm. Staying loosely aligned with the mathematics involved in markets is how WTI, Brent and Heating oil within 3-days have broken down through the very much watched 100-day and then 200-day moving averages and are in fact, all within sight of being oversold.

It might be that this near oversold status is causing a hiatus in selling this morning. The overnight news gleans little to be particularly positive about and further data from China earlier would ordinarily put industrial commodities on the back foot if it were not for the loss of $5/barrel that Brent has already been subject to in the last 4-trading days. China’s October year-on-year CPI registered a reading of -0.2% against a -0.1% call and although PPI at -2.6% was a tick higher than expectation, China’s economy still stands in the dock, charged with deflation. However, Wall Street has struck a better mood of late and although progress is snail like, S&P 500 has registered 8-consecutive higher days, which will aid oil and offer a chance of a Thursday reversal in relief. The news of a ‘self-defence’ military strike into Syria by the US, is hardly the stuff of DefCon1, but it is a timely reminder that the Middle East is able to trip up those of an overly bearish nature. Still, this recent oil price capitulation is cause for concern with those involved with supply-side management and one wonders if recent Russian oil exports will strain its relationship with Saudi Arabia.

GMT | Country | Today’s Data | Expectation |

13.30 | US | Initial Jobless Claims | 218k |

13.30 | US | Continuing Jobless Claims | 1.82m |

Russia and Saudi Arabia might need an awkward conversation

All news services be they recorders of everyday events or financial, are as fickle as a teenager’s a-la-mode fashion fancy. The easy to write upon eternal intrigue in the Holy Lands lends itself to a scribe’s embellishments and it would take someone of a limited imagination not to air flow charts of thought that involve an Armageddon spread of the current conflict. Competing in immediacy, and what feels like adherence to an IT Managers mantra, is the idea of an interest rate reprieve which is switched on and switched off on a daily basis. These 2 largely opposing protagonists allow for other pressing global contentions to fall off the scope, for when was the last time much was written on the Ukraine war and its biproducts that have befallen the world’s trade such as sanction?

This week, with what does feel like limited copy and reaction, rumours of increased Russian oil flows gained substance as agencies reported an increase of oils making it to water and even destinations serviced by pipelines. This is even after a swingeing attempt by the US to target shippers that it deemed to be running the sanction blockade. Damning estimations from Rystad have that exports are way and above agreed levels by some 400,000 barrels per day and convergence in that approximation comes from Bloomberg Research reporting about 3.48 million barrels a day of crude was shipped from Russian ports in the four weeks to Nov. 5. ‘Damning’, bearing in mind the song and dance that Russia have made in trying to convince the world of its adherence to the 300,000 barrel per day voluntary cut, which is part of an agreement with Saudi to achieve stability, and it was only in August that Deputy Prime Minister Alexander Novak declared that Russia would keep the reduction cut of exports below the May to June average for the balance of 2023.

Language is a matter of convenience here, in a recent interview with Interfax, Novak said that a 300,000-barrel per day export cut included products. Bearing in mind the recent refinery issues and the ban on some fuels because of a national shortage, the convenience is not in words alone. Russia can now make a case for playing catch up with its OPEC+ cohorts but how that is received time will only tell. Yesterday saw a Reuters piece quoting the Russian Energy Minister via Interfax saying a consideration was underway lifting the export ban on some forms of gasoline, which will raise eyebrows because extra supply into an already depressed market is hardly a thing of stability.

Where this all ultimately leads to is Saudi. The Kingdom has yet again made all the sacrifice and engaged in most of, if not all, the heavy lifting and is now faced with the awful truth of an oil price that will not be controlled by supply, especially if supposed allies are not as strict as they might be. As we touched on recently, the oil giant has lost enormous amounts of GDP, of market share and petrodollars. Extra crude with no homes appears to be readily available from the USA, from Africa and from South America and the once red-hot distillate market is slowly becoming tepid and benign in keeping with the Northern Hemisphere’s winter. Basis Brent, not only has the market erased the Middle East conflict premium, but it has also now erased over 50% of the rally from the low of May and 75% of the rally from the beginning of July from when Saudi’s voluntary cut started.

Where does oil’s central bank go from here? Probably not to the panic button. Oil has developed a penchant of overshooting. After the COVID years and Ukraine, followed by the latest bout of Middle East slaughter, spikes are understandable and so is the hyperbole that follows them. This move down is yet another reaction to an over-reaction but comes at a time of resetting and financial rolling and is made that much worse. The winter still has a bite to come, albeit late, and who really can rest easy in saying that Gaza/Israel is contained? Still, these are trying times for the Gulf State and its patience is not limitless. In point of fact its history of meeting out lessons to non-conformists in oil production agreement are well recorded but it is doubtful that we have yet to come to such a crossroads. However, Saudi has a lot to ponder here, and a lot to lose and the market waits with more than a curious eye as to how the next chapter in this intriguing, and from a trading point of view, heart-stopping drama plays out.

Overnight Pricing

09 Nov 2023