Never a Dull Day

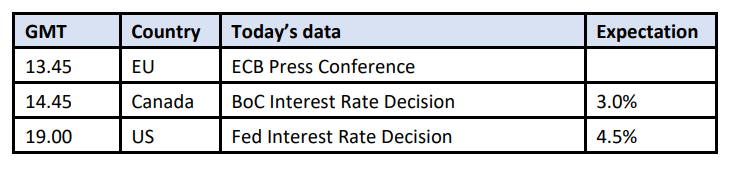

Markets and investor’s sentiment are still characterized by uncertainties and by the resultant inclination to react to headlines, rather than take a longer-term view. Equities stabilized after Monday’s sharp sell-off caused by the launch of AI models by Chinese start-up, Deepseek. The company is being accused by OpenAI of using its model to train its own competitor, thus raising the prospect of intellectual property theft. No doubt, the latest chapter of the fight for AI dominance has quite a few more pages waiting to be written but attention now is turning towards central banks and inflation. Today will see the Bank of Canada and the Fed to decide on the cost of borrowing. The former is expected to lower rates, but the US central bank is to stay put. Tomorrow it is the ECB’s turn and if Europe decides to support the block’s economy by lowering interest rates the gap between the US and the EU will widen with positive consequences for the dollar and the exact opposite impact on oil.

The two major crude oil contracts edged higher because protests in Libya reportedly halted crude oil loading at two of the country’s terminals, although the situation normalized towards the end of the day. The post-settlement API report was a mixed bag. Crude oil and gasoline inventories were seen rising last week but distillate stocks dropped sharply. Despite the healthy drawdown in the latter, weather-related price support is being gradually withdrawn as temperatures are rising in the northern hemisphere. The approaching expiry of the Brent contract and the self-imposed deadline of February 1 by the US administration on tariffs on Canada and Mexico, which will have a significant effect on US crude oil imports and product exports will guarantee volatile trading conditions. The OPEC+ JMMC meeting next Monday, discussed below, will be another source of ambiguity in the current worryingly unpredictable political and economic environment.

Between the Devil and the Deep Blue See

The next round of discussions between OPEC+ producers to decide on production levels will come on Monday, February 3. The Joint Ministerial Monitoring Committee (JMMC) is set to meet every two months to review the latest developments in the oil market and recommend the possible course of action for the energy ministers of the member states. The last get-together was held on December 5 last year on the sidelines of the latest OPEC and non-OPEC Ministerial Meeting. The group agreed to extend the overall production levels as laid out during the 35th Ministerial Meeting until December 31, 2026. Additionally, the eight producing countries that had decided to cut their output levels to support the market voluntarily agreed that the 1.65 mbpd reduction announced in April 2023 is extended until the end of next year. The additional 2.2 mbpd curtailment announced in November 2023 is extended until the end of 1Q 2025 and then will be phased out monthly until the end of September 2026, releasing 122,000 bpd of oil every month to the market. Of course, this is merely a broad framework as the monthly increases can be paused and even reversed depending on market conditions.

The modus operandi is clear. It appears that the decisions over the past 2 years to keep output levels constrained and take nearly 6 mbpd off the market were predominantly influenced by the absolute price level of oil, even though OPEC has been predicting a resoundingly tight global oil balance. Hypothetically and based on their forecasts, raising output would have been justified. Anyway, this status quo might well be upended by the re-election of Donald Trump and his transactional view on the state of the world and within that, the oil market.

The producer alliance could easily find itself in a situation, which is akin to the famous psychological experiment. If you are given $1,000 and asked to choose between a 50% chance of WINNING $1,000 or getting $500 for sure, most would opt for the second option. Conversely, if one is asked to choose between a 50% chance of LOSING $1,000 or giving up $500 for sure, most would opt for the first option. The study concluded when all options are unfavourable one tends to be more risk-seeking as the attitude toward profit or loss can and does diverge.

And with the US president demanding the OPEC group to increase production, the choices are anything but auspicious. With the re-emergence of Donald Trump OPEC is now facing a recalcitrant disruptor who does not shy away from using his economic might to achieve whatever his goal is. In this case, the objective is to force Russia, one of the allies of Saudi Arabia and the heavyweight in the OPEC+ group, to the negotiating table to end its hostilities against Ukraine by lowering oil prices via increased production with the side effects being mitigated inflation and lower domestic pump prices, the US thinking goes.

Given the current price environment and the market’s reluctance to push prices meaningfully above $80/bbl OPEC and Saudi Arabia would shoot themselves in the foot by complying. Fiscal breakeven prices of member nations, albeit varying, are meaningfully higher than the current level and the potential of the cheapening of oil will have a profoundly adverse impact on domestic economies at a time when every available petrodollar is precious. An uncooperative attitude, on the other hand, could lead to the souring of the fragile US-Saudi relations and could endanger any possible Middle East peace prospects that might be on the horizon. The nuclear option, a price war, similar to the one experienced in 2014-2015, which pushed the price of Brent down from $115/bbl to $27/bbl cannot be discounted either.

It is impossible to predict the outcome of Monday’s JMMC gathering. The gradual tapering of the 2.2 mbpd voluntary cuts from April will loosen the current oil balance by 610,000 bpd on average between 2Q and 4Q 2025. A pledge to start unwinding from 2H onwards, maybe a healthy compromise, will add 427,000 bpd to the market this year. Doing nothing will provoke the ire of the US president. Something must change, at least on a rhetorical level, and firm commitments must be presented towards the US. There are seemingly only bleak options for oil producers. Monday’s decision might shed light on how OPEC and Saudi Arabia intend to manage their delicate relationship with the new US Administration.

Overnight Pricing

29 Jan 2025