No-one Can Avoid the Churn

The quite remarkable market carnage seen yesterday has been somewhat calmed with the biggest catalyst for all the damage, namely the Nikkei, recovering nearly 75% of the value it lost. Experts and commentators pick over the bones of yesterday's bloodbath and again blame mainly falls onto Japan and the BoJ's probable quantitative tightening, the strength in the Yen and an evacuation of the so called 'carry' trade in global assets priced to Japan's currency. However, the confluence of poor US employment, a week of worrisome tech stock data and narrative joined forces and overwhelmed all before it. The Nikkei is notoriously fickle and reactionary and although the rally back will be welcomed, the S&P 500, probably a more reliable source of market sentiment, is better by 1.5% today having given away nearly 8% yesterday, therefore there is welcome relief, but one that is rightly guarded. The prop that finally came to the rescue was the US ISM Services PMI, registering at 51.4 above the 51.0 expectation and a vast improvement on 48.8 seen in June. As good as the turn from contraction to expansion seems, it is not without troubles, which we touch on below.

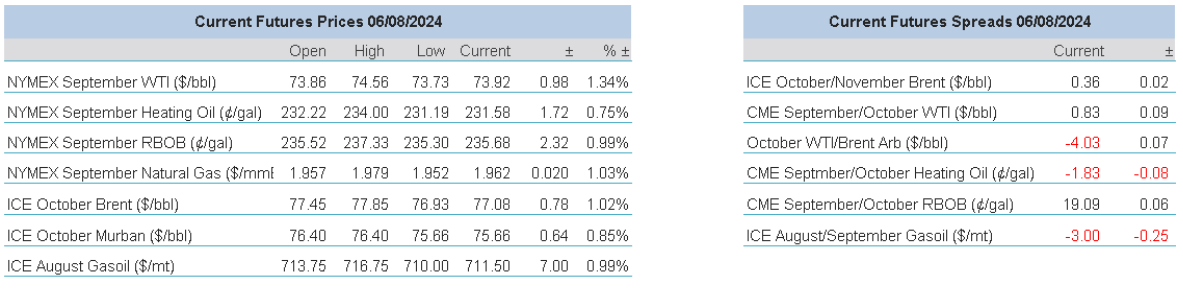

Oil prices yesterday had little choice other than to march to the tune of the wider suite. Not that encouragement lower was hard to find anyway. The spate of global economic warnings and problems in demand so very much highlighted by the ails of China offered a market that was in boxing parlance ‘leading with its chin’. However, $75/barrel in Brent is an awfully brave sale and will indeed offer a psychological support that for the moment may be relied upon. Aiding this mental floor was once again trouble in Libya. The factions of government are at loggerheads again and while initial reports that the Sharara field was experiencing partial closure, it seems that things have escalated and the whole of production is now down. In yesterday's melee, the threats of Iran and its proxies were forgotten, but a rude awakening is found in the attack on the US airbase at al-Asad in Iraq. This comes hotfoot on the warning from US Secretary of State, Antony Blinken, to the G7 that an Iranian attack on Israel is imminent. From whatever angle one gazes upon all markets, the churn is on.

Oil is a ramble to who knows where at present

‘You pays your money and you takes your choice’. So the old proverb goes. Investing in markets is about having bought the right to be involved, the freedom to then make decisions is one’s own. As there is no justification in blaming others on how one might have fared, there is also none in schadenfreude, which is a no-no more so in markets than in real world life. We hate to see or hear of folk losing money, whatever the suite or fraternity, defensive markets and negative profit and loss statements can only bode ill. However, it does become something rather cloying when there is a gathering of groans aiming complaint at the Federal Reserve. Ever since March 2022 when the FED made its first interest rate hike, Jerome Powell, hardly a figure of excess, has been persistently grey and conservatively stalwart of ‘following the data’. For every charge laid at the door of the US’s economic protector that it has been pedestrian in bringing about rate cuts in order to avoid recession, it can be answered that the bank’s reticence has been the fault of over exuberant buyers. The mere whiff of a 25-basis point cut has been greeted by nearly a year’s worth of buying and the role of the mega-cap tech stocks does not need any more study or does AI as their driver within. The wealth generated has been a self-fuelling, self-fulfilling and a massive inflationary influence. In plain-speak, each time the FED offered a veiled chance of relief, in came the hordes only to push back whatever timings had been quietly contemplated. The peripetia, or tragic turn of events, is the change in fortune of the employment market within the United States. Powell has almost been prescient in citing the jobs situation as being as important an indicator as that of inflation itself. The double whammy of poor Non-Farm Payrolls and higher US unemployment was an invitation to the clamouring longs to take a seat for a while and contemplate their navels.

Last week’s ISM Manufacturing gave something of a signposting to problems within the economy for employment. Existing orders shrank, along with output and productivity and the Employment Index registered 43.4 percent, down 5.9 percentage points from June’s figure of 49.3 percent. However, this is tempered somewhat by yesterday’s ISM Services PMI where the Employment Index reading of 51.1 percent is a 5-percentage point increase compared to the 46.1 percent recorded in June. Indeed, there was expansion overall in the micro indexes that make up the PMI, but the report warned of slower increases in new orders, restaurant sales and traffic being static on last year with some warnings of inflation mark ups and higher costs in foodstuffs and building materials.

Have we gone from one ‘r’ word rally to another ‘r’ word, recession in the stock market world? Crystal ball stuff, something that we are not equipped with. However, sentiment has a hold of this market, and how. It does not matter whether oil’s flat price is oversold and making a mockery of some of the nearby demand shown in crude backwardations. This is throwing the baby out with the bath water time, for if stock market holdings need to be financed by relinquishing other assets, then out those assets will surely go. Under such a backdrop, even if Iran makes good on any of its threats to Israel, our inkling is that rather than bring about a rush of buying, it will instead reinforce the idea of market avoidance and oil as a wait and see opportunity.

What of OPEC? Yes, well, what of OPEC? The cartel and running mates have been playing their own game of chicken with the US Federal Reserve. The more the FED ‘tightened’ the more OPEC+ took barrels off of the market, much to the chagrin of not only the world’s bankers but those of a mind who give support to NOPEC in the US houses of government. Happenstance possibly, but it did feel as if any moves made by central bankers to tame inflation was immediately undone by voluntary cuts inspired and policed by Saudi Arabia. How much of a shooting in one’s own foot this turns out to be, will be how and if there is a reversal on the forthcoming relinquishment of the self-imposed refrain. So far, in times of trouble, geopolitical or seasonality crisis, OPEC influence through cuts is something to be wheeled out as a supportive argument to bullish claims. It is becoming apparent that it cannot prop the market in isolation. The cuts are priced in, so is the cheating. Every time OPEC trims availability of oil to the market, producers in the US, Brazil and Guyana rub their hands and say thank you for the extra market share.

Is there at least a tenuous thread that strings all this together? Well, no. A hurting stock market populace, a proved right but possibly acquiescent FED, a world reliant on the performance of the US economy, a stumbling oil fraternity still underwhelmed by the third quarter and an OPEC, the so-called guardian of the oil price very much backfooted, means that the negative bias doldrums that besets the oil market will unfortunately continue. We would love to jump up and down, bang the desk and tell all that would listen that this is a screaming buy. But we are just too sensible, and this market is just too difficult.

Overnight Pricing

© 2024 PVM Oil Associates Ltd

06 Aug 2024